The market isn’t doing fixed-income investors any favors right now. But one of my favorite funds—in one of the best cash flow niches in the market—is delivering a gaudy 6.6% yield at today’s prices.

And it does that by holding some of Wall Street’s most boring, stable and dependable securities.

How can we bank this 6.6% “free lunch” when 10-year Treasuries still pay less than 2%? By tapping into an income stream that most individual investors rarely think about: Preferreds.

The Power of Preferreds

If we wanted to own a piece of a company, say JPMorgan Chase (JPM), we’d go out and buy a few shares of JPM. Those particular shares are what’s known as the “common stock” of this mega-bank.

But look just past the common stock, and that’s where you’ll find preferreds.

Corporations will sometimes issue preferred stock as an alternative to issuing bonds to raise cash. These preferreds generally pay dividends that receive priority over those paid on common shares (a nice benefit during brittle economic times like these).

Another nice benefit? Sometimes, preferred dividends are “cumulative”—if any dividends are missed, those dividends still have to be paid out before dividends can be paid to any other shareholders.

But better still, these dividends are almost always juicier than the modest dividends paid out on common stock. A company whose commons yield 2%, even 1%, might still be doling out 5% to 7% to their preferred shareholders.

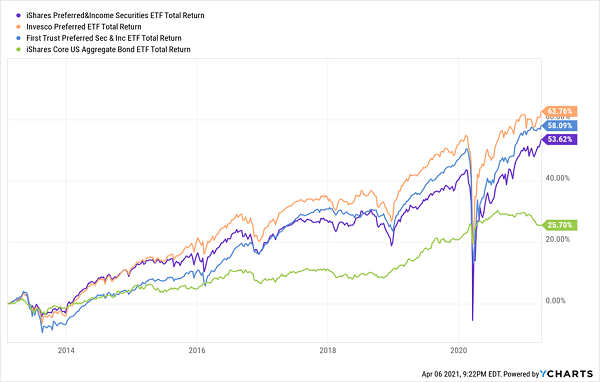

The downside to preferreds is that they behave a lot more like bonds, trading around a par value over time. But the chart above is missing one key component—the dividends. Once you factor in preferreds’ juicy income, you get extremely attractive total returns with a fraction of the risk of commons.

Just remember: Preferred stock can collapse the same way common stock can, and in fact, some preferreds went the way of the dodo during the 2007-09 financial crisis. That’s why second-level investors like us do the smart thing and buy preferred funds—locking up those 5% to 7% yields while defraying our risk across dozens, even hundreds of issues.

Let me show you what I mean.

The Best, and Worst, Ways to Invest in Preferreds

Again, the 10-year T-note is yielding 1.7%, but like most people, we buy our bonds via funds. So let’s say we buy a medium-term bond fund like the iShares 7-10 Year Treasury Bond ETF (IEF)… we’re actually getting less than that, at a meager 1.4%.

That means if you sunk a million dollars into IEF, you’d be generating a meager $14,000 in annual income.

Sad.

If we go out even further, say 20-plus years, with the iShares 20+ Year Treasury Bond ETF (TLT), we’re taking on quite a bit more risk just to get bumped up to a 2.2% yield right now.

Now, let’s see what happens when you upgrade yourself to preferreds:

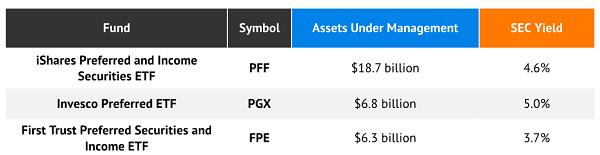

The iShares Preferred and Income Securities ETF (PFF), Invesco Preferred ETF (PGX) and First Trust Preferred Securities and Income ETF (FPE) are the three largest preferred exchange-traded funds on the market. And as you can see in the table above, you’re looking at an immediate upgrade in yield over Treasuries and corporates, and in the case of PFF and PGX, you’re easily outyielding junk bonds, too.

All of these funds offer similar exposure, so we’ll use PFF as an example. The ETF holds more than 500 preferred securities, the majority of which (60%-plus) come from financial institutions such as Wells Fargo (WFC) and Bank of America (BAC). This is par for the course, as is large weightings in industrial and utility preferreds.

We’re getting built-in diversification and a decent yield for all of 0.46% (the best of the trio, by the way). And across all three, we’re enjoying superior performance to a standard bond index.

Preferreds Have Doubled Up Basic Bonds

And we can do even better by thinking smaller.

Let’s Earn 6.6% With Preferreds

If you’ve heard of a high-yield ETF, chances are there’s a better CEF version just waiting to be discovered.

Closed-end funds command a mere fraction of the market of exchange-traded funds. They’re typically actively managed, they can be more complex, and they can charge higher fees, which scares off many beginner investors.

But if we choose our managers wisely, they’ll more than make up for their costs.

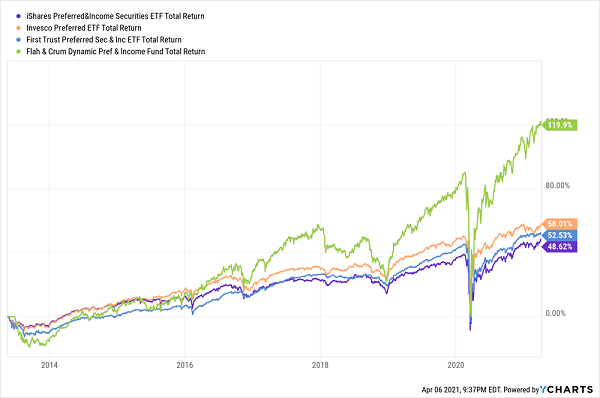

Our “mystery” 6.6% yielder is none other than the Flaherty & Crumrine Dynamic Preferred and Income Fund (DFP). At about $570 million in assets, DFP is a mere fraction of the ETFs we just discussed. And because it’s in the unsexy world of CEFs, it’s not on your typical CNBC guest’s radar.

Too bad for them.

“Basic” Preferred Funds Eat DFP’s Dust

DFP’s managers have put together a portfolio of roughly 170 holdings that, like most preferred funds, is heavy in financials, at 86% across banks, insurers and other sector names. Most of the preferreds are clustered around the “investment-grade” line, with 44% in Baa-rated (the lowest investment-grade rating), and 39% in Ba-rated (the highest junk rating).

You also get some international diversification, which doesn’t hurt; the U.S. makes up 70% of holdings, but you also get exposure to the U.K., France, Australia, even Mexico.

Flaherty & Crumrine’s managers are what set DFP apart from preferred ETFs, which are almost all index-based. Here, management has an advantage in that they can exploit deep values in the preferred space that the rules-based indexes just simply can’t do anything about.

But also powering DFP’s high yield and strong performance is management’s ability to use leverage to amplify its bets. At the moment, DFP uses a high 33% leverage—which results in more volatile returns than its ETF peers, but it’s hard to complain about the results.

If a 6.6% Yield Sounds Great, How About 8%—Paid MONTHLY?

Alas, would-be buyers of DFP have been cursed by the fund’s success. It has become so relatively popular of late that it’s actually trading at a whopping 12% premium to its net asset value.

This is a great fund, with great people at the helm. But paying $1.12 for a buck’s worth of assets is a quick way to handicap your own returns on new money.

Fortunately, DFP can wait. Because many of the other picks in my “8% Monthly Payer Portfolio” are trading at the right price, and the right yield, right now.

In fact, today, you can secure a portfolio yield of more than 8% … and have those dividends paid out to you each and every month.

Just like DFP, many of the picks in my “8% Monthly Payer Portfolio” leverage the power of steady-Eddie holdings like preferreds to generate massive yields and shockingly aggressive performance. That allows us to double our money much more quickly than most investors do through popular ETFs.

The dividends you’ll find here are truly life-changing: drop $500K into this powerful portfolio now and you’ll kick-start a $40,000 income stream. That’s about $3,300 a month in regular income checks!

Now is the time to get in, while you can still do so at a bargain. Click here to get everything you need—names, tickers, complete dividend histories and more—instantly.