Most folks dread checking their retirement accounts these days, but not us contrarian income-seekers. We’re coolly playing our “no-withdrawal” retirement strategy, paying our bills with 7% to 9% dividends—while leaving our pile of saved cash alone.

I know that sounds pretty sanguine—boastful, even—when the S&P 500 is down nearly 20%. But deep down, most people know that a “dividends-only” retirement really is the best way to go.

Trouble is, most folks don’t know how to get there. I’ll lay out a roadmap that could let you hang ’em up on dividends alone with as little as $500K saved a little further on.

Fed Goes From Friend to Foe

First, I need to tell you that going full “no-withdrawal” is critical now, because we’re probably looking at steeper market declines from here, for one reason: the Fed will not be riding to the rescue this time.

That’s because the so-called “Fed put”—the central bank’s habit of diving in to save a sinking stock market—is dead.

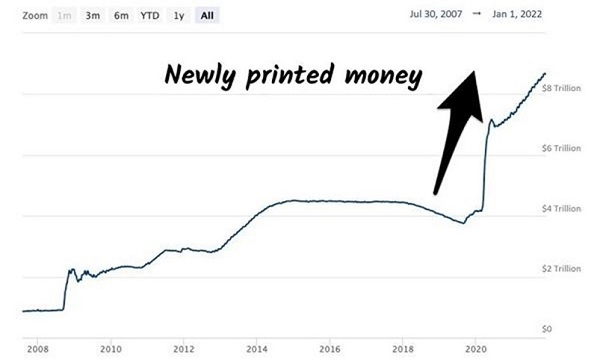

The origin of the Fed’s “put” was the 2008 financial crisis. The financial system was on the ropes and the stock market itself became “too big to fail” as far as the Fed was concerned. Then-Chairman Ben Bernanke printed a bunch of money, boosted the market and was heralded a financial hero.

But Bernanke didn’t have 8% (self-inflicted) inflation to deal with, as Fed Chair Jay Powell does. I say “self-inflicted” because Powell’s last “put”—the $4 trillion he printed to float the economy through the pandemic—spiked the stock market in 2020 and 2021:

Now, unfortunately, Powell must take the punchbowl away. To save his job, he has to crush the 8%+ inflation he’s caused, even if it means sacrificing the stock market.

The “4% Rule” Goes From a Bad Strategy to a Disastrous One

All of this has turned retirement into an ongoing vigil over the latest market moves for folks who rely on the so-called “4% rule.” A sacred cow for most advisors, it states that a retiree can withdraw 4% from their portfolio every year and, no matter the market’s swoops and swoons, the money would likely last at least 33 years.

So a 60-year-old with a million-dollar portfolio can pull out $40,000 every year and be good until at least 93. Not bad.

At least this was according to the 50-year period the rule’s creator, William Bengen, analyzed. Trouble is, 2022 is a dumpster fire, and many folks who follow this rule have been forced to withdraw their cash at exactly the wrong time!

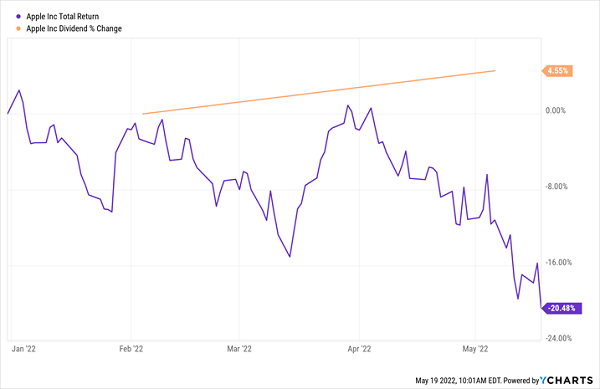

The biggest tech stock of them all, Apple (AAPL) proves how dangerous the 4% rule can be at times like these:

As you can see, the dividend is fine—growing, even—but you’re selling at a 20% loss. In other words, you’re forced to sell more shares to supplement your income when they’re depressed. This is the opposite of the dollar-cost averaging you probably used to build your portfolio!

It’s also a recipe for running out of money. Just ask Bengen himself: he’s nine years into retirement and concedes he’s “not comfortable.” The MIT grad admitted this to the Wall Street Journal, adding that he’s cutting back on restaurants.

Billy B.! Ditch your own rule and follow our “no-withdrawal retirement plan.” We contrarians don’t limit ourselves to a bland mix of conventional stocks and bonds. Instead, we retire on dividends alone, which leaves our cash intact and lets us spend our days pretty well anywhere else but in front of a computer screen.

Money manager Tom Jacobs and I literally wrote the book on this. In How to Retire on Dividends: Earn a Safe 8%, Leave Your Principal Intact, we outline our “no-withdrawal” approach to retirement:

- Save a bunch of money. (“Check.”)

- Buy dividend stocks with big yields.

- Enjoy the income while keeping the original principal intact.

Step 2 is tricky one for many investors. Even if you manage to save up a million bucks, the S&P 500 is of little help, yielding just 1.5% today. A seven-figure nest egg in popular “low cost” SPDR S&P 500 ETF Trust (SPY) will land you in the low-income bracket with just $15,000 a year.

That will keep your taxes low. And your quality of life!

To make our savings last, and our working life worthwhile, we really need yields in the 7% to 8% range that profit as inflation and interest rates rise. We typically don’t see these stocks touted on Bloomberg or CNBC, but they are around.

And you don’t have to be a millionaire to take advantage of this strategy. A $500K nest egg yielding 7.5%, for example, will create $37,500 in annual income. Or $200K will generate $15,000 in yearly dividend income (better than a million bucks in SPY!) You get the idea.

The important thing is that these dividends are reliable, which creates stability for the stock (and fund) prices attached to them. We want our income and the ability to maintain our principal. It’s really the only way to retire comfortably, without having to stare at stock tickers all day, every day.

3 “Inflation-Friendly” Dividends Yielding 9.2% (With Upside Potential)

In the portfolio of my Contrarian Income Report service, we hold three stocks that profit from inflation in our aptly named “Inflation-Friendly Dividends” bucket.

These 3 picks yield a gaudy 9.2%, on average, today, and they’re just the start. We’ll also be looking to add more inflation-friendly picks in the coming months, adding diversification and dividends as we do.

These 3 stocks are among my best recommendations for putting my “no-withdrawal” retirement plan into action. I’ll share them with you now when you take a no-risk trial to Contrarian Income Report.