Real estate investment trusts (REITs) are dirt-cheap—but hurry if you like dividends. These generous payers may not be in the bargain bin for much longer.

REITs tend to trade opposite long-term interest rates. The ever-rising 10-year Treasury yield has been a big headwind for these stocks.

But all rising rate periods eventually end in recession. Which brings falling rates. Which hurts stock prices—unless you like REITs.

REITs trade more like bonds than stocks, so they tend to hold up well in recessions. Their dividends, ignored during AI bubbles, come back in vogue as easy money dries up.

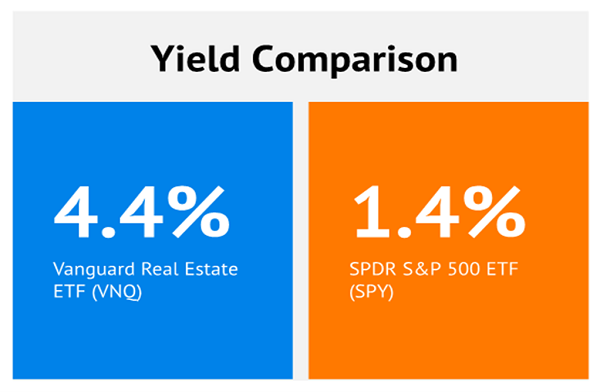

So here we go—bargain city! Vanguard’s vanilla REIT index dishes three times the yield of the broader market right now!

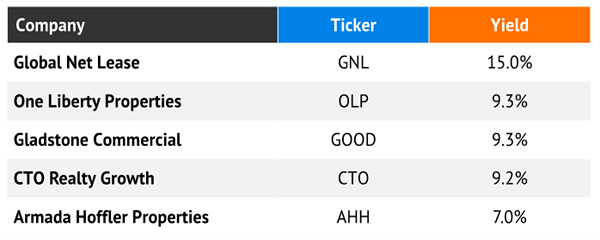

And that’s just an average. If you’re looking where I’m looking, you can snap up yields of between 7% and 15% that have remained dirt-cheap for some time.

But this is only a game for the patient. This period of rising rates has already outlasted many so-called experts’ expectations, and many would-be traders looking for a quick score have been sitting on these positions for months longer than they’d like.

Buy-and-hold investors, though, know that interest rates will rise and fall over time. The key is striking now while prices are low to give you the best chance at outsized gains over the long haul—and collecting big, fat yields all the while.

So, let’s look at a few REITs that remain in the bargain bin—five stocks currently averaging a nosebleed 10%.

Three of the stocks on my radar are awfully familiar—because they were offering up similarly super-sized dividends just a few months ago.

CTO Realty Growth (CTO, 9% yield) is a diversified REIT that owns 16 retail properties, three office properties, and five mixed-use properties totaling more than 3.7 million square feet. It also owns a nearly 15% stake in Alpine Income Property Trust (PINE), a net-lease REIT.

CTO Realty’s shares are off 25% over the past year, sagging worse than the broader REIT sector in large part because it was forced to lower the rents on two large leases. Still, at least until recently, when rate woes clipped REITs again, CTO was showing some life amid brighter prospects for office real estate in general.

You don’t get a 9% yield for nothing, of course—notable tenants include Regal Cinemas (just recently exited bankruptcy protection) and WeWork (a very real bankruptcy risk), so that’s still countering some of CTO’s progress. Still, this REIT is showing operational strength, and its tight (nearly 90%) FFO payout ratio is projecting lower through this year and next.

One Liberty Properties (OLP, 9.3% yield) is a net-lease REIT that also counts Regal among its tenants—and it’s having a more difficult time with that.

OLP is a net-lease REIT that’s in the middle of a portfolio transformation. While its 121 properties include restaurants, fitness centers, grocery-anchored real estate and office space, that mix is increasingly leaning toward the industrial space. Indeed, industrial properties now make up a plurality of One Liberty’s sites (49), as well as a majority (56%) of contractual rental income.

However, I previously mentioned that Bed Bath’s bankruptcy was hanging over OLP’s head, as well as a possible restructuring of leases it has with Regal Cinemas. The latter is no longer possible—it’s certain—with significant rent reductions starting as of Regal’s emergence from Chapter 11 bankruptcy protection. On top of that, it’s negotiating a short-term lease extension with LA Fitness that could lead to a rent reduction at a Hamilton, Ohio fitness center.

OLP’s poor fortunes have driven its valuation lower and its yield higher, but there has to be light at the end of the tunnel before it makes sense to chase.

No Reason to Think One Liberty’s Downturn Is Over Yet

Gladstone Commercial (GOOD, 9.3% yield) is part of the Gladstone family of REITs and business development companies (BDCs), which also includes Gladstone Land (LAND) and Gladstone Investment (GAIN) and Gladstone Capital (GLAD).

Gladstone Commercial owns 136 single-tenant and anchored multi-tenant net-leased industrial and office properties across 27 states. A roughly 40% allocation to office properties has crippled the share price and, earlier this year, forced GOOD to clip its monthly dividend by 20% to 10 cents per share. That’s misery for current shareholders, but it does make the dividend look safer to new money—the FFO payout ratio has dipped from 96% to 77%.

Conversely, though, optimism over a push by corporations to get employees back into the office at least part-time has put some wind in Gladstone’s sails. Long-term, offices might never be what they once were, but it’s a much-needed sign of stabilization. GOOD’s most recent quarterly core FFO topped estimates. And to help offset issues with interest-rate caps expiring this year (raising interest expenses), management has waived its incentive fees for the rest of this year.

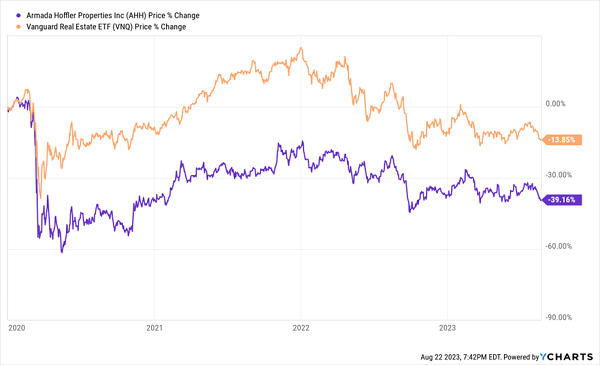

Armada Hoffler Properties (AHH, 7.0% yield) is another diversified REIT that owns 38 retail properties, 10 multifamily properties and nine office properties throughout the Mid-Atlantic and Southeast. But that spread is a little misleading—while office real estate might make up just 16% of overall properties, it accounts for 35% of property NOI, which helps explain some of its difficulties basically since COVID began.

Armada’s Fleet of Investors Are Still Trying to Recover From COVID

Despite its problems, there’s plenty to like about AHH. The REIT has a high-quality portfolio with occupancy in the high 90s across all segments. It’s shrinking its mezzanine portfolio, which should lead to more reliable results. And it recently closed on a $215 million acquisition of Atlanta’s Interlock—a mixed-use public-private partnership with Georgia Tech.

And while, like many REITs, Armada had to slash its dividend (by half!) in 2020, the payout has quickly recovered and is now just 11% below its pre-COVID rate.

Global Net Lease (GNL, 15.0% yield) offers up a wild yield of 15%—and it’s also something of a wild card right now.

This commercial REIT operates not just here in the U.S., but in 10 other countries, including the U.K., Netherlands, Finland and France. It owns 317 properties leased out to 139 tenants in 51 industries, but it’s about to get a whole lot bigger. Subject to a Sept. 8 shareholder vote, it’s set to merge with The Necessity Retail REIT (RTL), which would make it the fifth largest publicly traded net lease REIT, with a combined 1,300-plus properties.

Global Net Lease says the deal should be 9% accretive to annualized adjusted FFO per share in the first quarter after closing compared to the first quarter of 2023. It should also reduce net debt to adjusted annualized EBITDA to 7.6x by Q4 2023 (from 8.3x for GNL and 9.9x for RTL).

On top of that, an already wide portfolio should become even more diversified. Global Net Lease will shift from a 5/55/40 retail/industrial/office split to 48/31/20—halving the weight of office properties on the portfolio. And no single industry will account for more than 6% of annualized straight-line rent.

Earn 8% in Retirement + Get Paid EVERY MONTH

But remember: Global Net Lease is also a company that hasn’t lifted a finger to lift its dividend since cutting it in 2020. And Wall Street hasn’t exactly jumped for joy at this Wall Street wedding, with shares still grossly underperforming even the weak REIT sector.

It’s a gamble, just like any merger, and it will take a while for the dust to settle.

Long-term investors looking for high yields now should be looking for more certainty and stability. In fact, they should be looking for downright boring companies that don’t generate headlines—just fat, consistent dividend checks.

And those are the kind of high-yielding blue chips I hold in my “8% Monthly Payer Portfolio.”

Don’t let the name deceive you. The “8% Monthly Payer Portfolio” isn’t just about earning high yields—it’s about earning high levels of yields by leveraging steady-Eddie holdings that won’t have you reaching for the Pepto every time the S&P gets the jitters.

You also won’t need to stress about the size of your nest egg. Unlike many retirement plans that require you to bleed out your savings as you age, the income this portfolio can generate is so rich, it can sustain a retirement on dividends alone.

Here’s the math: A mere $500,000 nest egg—less than half of what most financial gurus insist you need to retire—put to work in this powerful portfolio could generate a $40,000 annual income stream.

That’s more than $3,300 every month in regular income checks!

Even better? The current bear market has provided us with a rare gift, pulling many of these monthly dividend stocks back into our “buy zone,” where we can grab them at bargain prices. Click here to learn everything you need about these generous monthly dividend payers right now!