Few people know it, but you don’t have to buy a stock for the price you see on Yahoo Finance.

The truth is, you can buy some of the best large cap dividend payers for cheaper: and I don’t mean a little cheaper. I’m talking a 16% discount.

How?

Through a closed-end fund (CEF) that’s trading at a ridiculously high discount to its net asset value (NAV). That’s despite a strong track record, low expenses and an attractive 4.4% dividend yield.

Let’s break each of those things down one at a time, starting with the name of this unheralded investment.

It’s called Tri-Continental Corporation (TY), and it holds some of America’s safest and highest-quality stocks. But you wouldn’t know it by looking at the gap between the value of its assets and its share price: due to irrational investor fears and a lack of knowledge about CEFs generally, Tri-Continental is trading at a 16% discount to the value of its top-notch portfolio today.

Hard to believe, but true.

Demystifying Closed-End Funds

Closed-end funds are similar to mutual funds and ETFs, but with two very important characteristics. Most importantly, CEFs issue a certain amount of shares when they IPO, and that’s it. They can’t ever issue additional shares (that’s why they’re “closed,” as opposed to mutual funds and ETFs, which are “open” and can release new shares at any time.)

Because the supply of shares is fixed, CEFs often go down in price even if the value of their assets doesn’t go down by as much. This results in CEFs being priced below the net asset value of the underlying assets. Likewise, CEFs can sometimes go up in price when the value of their assets doesn’t, resulting in a premium to NAV. This is crucial, because it makes it possible to buy the assets inside a CEF at a discount.

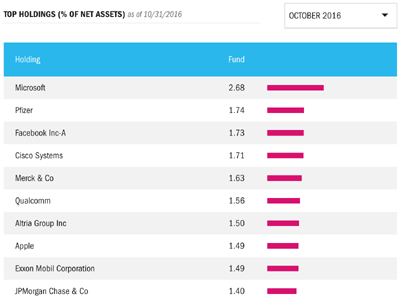

CEFs are ignored but powerful tools savvy investors use to outperform the broader market, and TY is no exception. Its top 10 holdings are all no-nonsense, low-beta (meaning less volatile than the overall market) stocks that have delivered strong returns for shareholders:

Immediately, you see some nice sector diversification in this portfolio, with a tech bias.

Microsoft (MSFT), Facebook (FB), Cisco Systems (CSCO), Qualcomm (QCOM) and Apple (AAPL) represent 9.2% of the fund’s assets, while three other sectors split the next 7.7%: energy, through ExxonMobil (XOM), financials, through JPMorgan Chase & Co. (JPM), consumer products, with Altria (MO), and biopharma, with Pfizer (PFE) and Merck (MRK).

The rest of the fund is similarly diverse, with a bit more tech but an overall balanced exposure to all sectors. But what’s really interesting is how TY has performed relative to these stocks. Let’s look at the techs first.

Underperformance Signals Buying Opportunity

After a massive year for all of TY’s tech holdings, the fund itself is a laggard, outperforming only Apple year-to-date. That’s widened TY’s discount to NAV and insulates you from buying, say, at the peak of a 37% gain, like you would be if you bought Qualcomm on its own right now.

A Discount to Non-Techs, Too

The trend holds true with the fund’s non-tech holdings. As you can see, TY lags every one but Pfizer year-to-date, making the fund’s discount to NAV even more attractive after a year of gains for its constituents—and boosting our upside potential, as well.

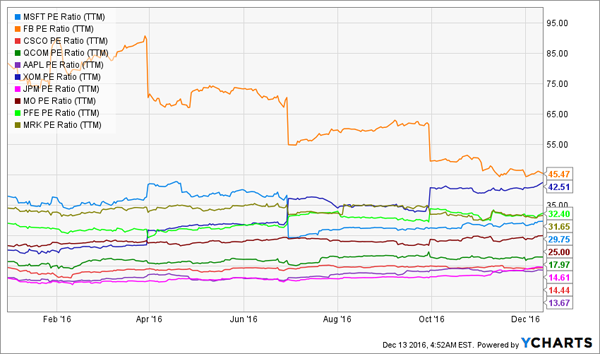

If you wanted to buy these stocks individually, you could overpay if you did so on the open market. Look at the price-to-earnings (P/E) ratios of both the tech and non-tech names mentioned above:

Why “Bundling” Is Better

This is the constant concern with buying a top-performing stock; are you buying too late and getting a P/E ratio that’s a lot higher than what you would have gotten a year ago?

Looking at Facebook’s past performance, that fear was clearly overblown; despite a 12% year-to-date gain, FB’s P/E ratio has fallen from nearly 80 to just over half that, thanks to monstrous revenue and earnings growth at the social-media juggernaut.

But with growth in FB’s top and bottom lines slowing, you’d be right to be concerned about buying now, at a P/E ratio of 45, since that’s still 80% higher than the S&P 500, on average, and above the ratios of most companies with a similar market cap.

However, if you buy TY to get a piece of FB, you’re not buying at a P/E ratio of 45. That’s the power of TY’s discount, which makes your effective P/E ratio 37.5.

It gets better. The average P/E ratio of TY’s top holdings is 27, which is slightly higher than the broader market’s. But because of TY’s discount to NAV, the fund’s P/E ratio is 22.5, which is actually 10% less than the broader market.

In many cases, CEFs hold high discounts to their NAV because many of these funds are poorly managed and have outsized fees. Fortunately, TY suffers from neither problem:

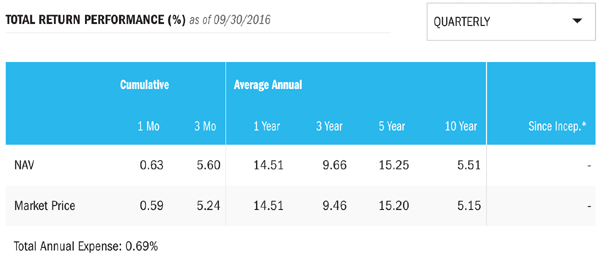

Over the last five years, TY has had a 15% average annual return on its NAV and its market price, topping the S&P 500’s 12% over the same period. That’s right: TY has outperformed the market by 300 basis points a year, on average, over half a decade.

Many people dismiss CEFs because they fear high fees, and sometimes this dismissal is justified. In TY’s case, however, fees aren’t an issue. The fund’s annual management expense of 0.69% of assets is justified by its outperformance, which far exceeds its fees (especially since its 15%+ return is net of fees in any case).

Which brings me back to TY’s dividend yield: 4.4%.

As I said, it’s a great yield in today’s low-rate world, and with the S&P 500’s average payout clocking in at less than half that, you’re doing much better than if you simply park your money in an exchange-traded fund like the SPDR S&P 500 ETF (SPY).

And unlike “passive” ETF investors, you get TY’s top-notch management team working for you, too. Thanks to their deft moves, the fund’s dividend has soared in the past five years.

Reliable Payout Growth

But what if I told you that you could tap into the same level of expertise, also at a big discount, but with a hefty yield of more than 8.0%—nearly double what you’d get from TY today?

It comes in the form of 3 other CEFs we like even better than TY. These 3 income wonders yield 8.2%, 9.9% and even 10.1%.

Like TY, investors threw them out in an irrational selloff earlier this year. That’s great for us, because we can buy these funds cheap now … and then ride them upward as their discount windows close.

These 3 income generators are the cornerstones of our “no-withdrawal” retirement-portfolio strategy, which lets you retire on dividends alone with a nest egg as modest as $500,000. Why rely on stock price appreciation in an inflated market when there are secure, high-paying dividends you can simply live off of and keep your capital intact?

Most investors know this is the right approach to retirement. Problem is, they don’t know how to find 8% yields to fund their lives.

That’s why I specialize in finding safe, under-the-radar high-income options. Click here and I’ll explain more about our no-withdrawal approach—plus I’ll share the names, tickers and buy prices of our 3 favorite closed-end funds for 8.0%+ yields.