No safe bond pays 10% itself, of course. But it is possible to generate double-digit yields from a portfolio of secure bonds.

The secret is similar to successful dividend investing. Why buy a stock and be content pocketing “only its dividend” when you can have the payout with price upside to boot?

Most income investors are even less thoughtful when they purchase bonds. They fixate on the coupon rate (which these days they are inevitably disappointed with.) They watch their bonds weigh down their entire portfolio, muttering to themselves “at least they are safe.”

Well, sure. But they can be both safe and profitable. Just ask any Contrarian Income Report subscriber who held one of my favorite bond funds throughout 2017. They didn’t have to “settle” for 7%+ yields. They enjoyed double-digit price gains too, bringing their total returns for the year (including dividends) to 20%+!

20%+ Returns From These Safe Bonds in 2017

Is this repeatable in 2018? Yes – especially for those willing to “flip horses” and buy laggards that are due for a run next.

So how do we select the best bonds for 2018, and earn these 10%, 15% and even 20% returns (with 8%+ of those returns coming as cash dividends?) It’s a simple three-step process.

First, Bet the Smart Money for “Rising NAV”

To make big returns, we must choose funds whose assets are going up in value. I know this sounds obvious, but again, many income investors conveniently forget about this as they fixate on bond yields solely.

You wouldn’t buy a stock with stagnant earnings. So why buy a fund with stagnant NAV over time?

NAV stands for net asset value. It is the market value of the fund’s entire portfolio. In other words, if the ticker liquidated itself today, here’s what it would fetch on the open market.

Let’s look at one of the funds from the previous chart, the Flaherty & Crumrine Dynamic Preferred and Income Fund (DFP). They purchase “preferred shares,” which are bond-like instruments issued by corporations to raise capital. They often yield more than the stock’s “common” shares, hence their appeal.

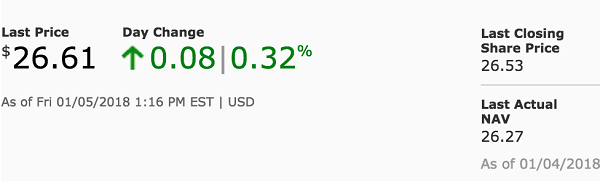

We can find DFP’s current NAV by visiting a site such as Morningstar.com. It’s right there next to the ticker:

NAV is Updated Daily on Morningstar

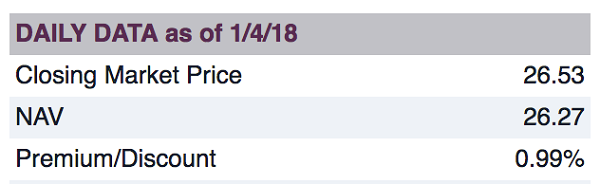

Or, as I prefer to do, you can go straight to the source – the fund’s website:

NAV Straight From the Source

We’ll talk about the discrepancy between market price and NAV (and the premium or discount that results) in a moment. First, let’s talk NAV trend.

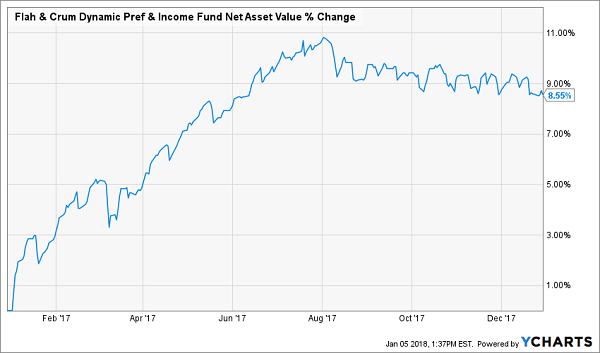

DFP’s current NAV of $26.27 doesn’t tell us much – until we plot its course throughout 2017. Here we see why DFP was such a star – its holdings increased in value by 8.6% during the year!

NAV +8.6% in a Year

(Remember that bonds, like stocks, can go up and down in price. For example, investors who bought bonds in the early 1980s profited from price gains. Their “higher paying paper” became increasingly valuable as interest rates dropped over the next two decades. Not only were they able to lock in higher yields, but they also enjoyed price upside from their holdings.

While 2018 is not 1981, savvy bond managers like the folks at Flaherty & Crumrine can locate niche opportunities that you and I simply don’t have access to. Their brilliance is reflected in their portfolio’s rising NAV.)

Back to DFP. Add its 8.6% rising NAV gain to the stock’s initial yield at the start of 2017 (7.3% or so) and we have 16% of the fund’s 2017 total returns accounted for.

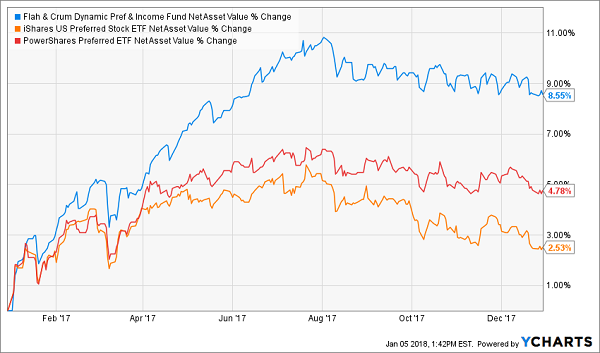

But was 2017 simply a good year for preferred shares? It was – but, as usual, the smart managers at DFP outperformed their “dumb money” ETF counterparts.

Most investors who read about preferred shares pile into the popular iShares US Preferred Stock ETF (PFF) or the PowerShares Preferred ETF (PGX). Their computer-generated NAVs didn’t keep pace with the human selected variety (yet again):

Popular (and Overrated) ETFs Underperform (Again)

Taking a bigger picture view, we see that DFP has comfortably doubled up its robot counterparts over the past five years:

Smart Money Doubles Up Robot Money

As I’ve pointed out before, past performance in bond-land tends to be quite indicative of future results. So it’s important for us to select the best managers.

And as we bet with the best, we’ll next use a simple market timing technique to determine when to buy them for maximum upside.

Then, Buy the Bargains

DFP pays 7% today. That’s not bad in a 2% world.

But can we count on 8%+ NAV growth again in 2018?

I don’t like to make these assumptions. I prefer to be more conservative and buy funds that are only trading at discounts (the steeper the better) to their NAV.

Big discounts are clear contrarian indicators. The more investors dislike a strategy at the moment, the greater the discount they demand. The irony is that most people love chasing recent performance, which means they’re most inclined to sell a loser at the moment it’s most likely to turn around.

As a result, the bargain bin often contains high payers selling for 10% discounts or better. This means you’re getting the fund’s assets for $0.90 on the dollar – an easy way to lock in likely 10% upside along with your big yield as the discount window closes.

Back to DFP, we see that these big bond profits weren’t rocket science. Anyone who bought when the price (orange line below) lagged the NAV (blue line) did quite well:

Always Demand a Discount!

As you can see on the right-side of the chart, DFP’s discount window finally slammed shut last year. The fund actually now trades at a premium to its NAV (which shows you how manic investors can be with regards to excellent but little-known funds!)

When we add the 4% premium gain to our initial 7.3% yield and our 8.6% NAV rise, we get the 20% total return that DFP generated last year.

Finally, Enjoy the Monthly Dividends

DFP’s easy money window may have closed, but there are a few others which remain wide open (for now) heading into 2018. This is where we should look for our potential 20%+ returns in the year ahead.

Plus, my five favorite bond funds for 2018 all pay their dividends monthly. And right now, this five-pack yields an average of 8.42%. Let me show you what this translates to in terms of monthly checks (or deposits straight into your account).

Most investors with $500,000 in their portfolios think they don’t have enough money to retire on. They do – and they can do it with safe bonds alone. If you deployed this capital into my top five bond funds for 2018, you’d be looking at this income stream to kickoff the new year:

Got a million parked in underperforming fixed income? Great – you can redeploy that and double the “every 30 day payments” you see above (for $7,016.66).

These monthly checks should help keep your mind occupied while you sit back and wait for the other pieces of the 20% return puzzle to fall into place!

The 5 Best Bond Funds to Fund Your Retirement

Monthly paying bond funds – with price upside potential – are a cornerstone of my 8% “no withdrawal” retirement strategy, which lets retirees rely entirely on dividend income and leave their principal 100% intact.

Well that’s not exactly right. Their principal is more than 100% intact thanks to price gains like these! Which means principal is actually 110% intact after year 1, and so on.

To do this, I seek out funds that:

- Pay 8% or better…

- Have well funded distributions…

- Trade at meaningful discounts to their NAV…

- And know how to make their shareholders money by increasing NAV consistently.

And I talk to management, because online research isn’t enough. I also track insider buying to make sure these guys have real skin in the game.

Today I like five “blue chip” bond funds as best income buys. And wait ‘til you see their yields! These “slam dunk” income plays pay dividends up to 10.2%!

And as I mentioned, they pay every single month.

Plus, they trade at 10-15% discounts to their net asset value (NAV) today. Which means they’re perfect for your retirement portfolio because your downside risk is minimal. Even if the market takes a tumble, these top-notch funds will simply trade flat… and we’ll still collect those fat dividends!

If you’re an investor who strives to live off dividends alone, while slowly but safely increasing the value of your nest egg, these are the ideal holdings for you. Click here and I’ll explain more about my no withdrawal approach – plus I’ll share the names, tickers and buy prices of my five favorite bond funds for up to 10.2% yields.