The REIT bears have gone too far this time.

In the past few days, I’ve seen a lot of panicky commentary warning that incoming Federal Reserve chair Jerome Powell will raise rates too fast after he takes over in February—and that would be a disaster for real estate investment trusts (REITs).

Don’t take the bait.

Because it all adds up more fear-fanning headlines from a business press desperate to make something out of nothing.

I’ll show you why in a moment. Then we’ll move on to 3 corners of the REIT space (and 5 stocks in particular) that underperformed in 2017—and are poised to spring back big time in 2018.

The Powell Factor

First, unless you’ve been avoiding the Internet and all newspapers for the last 6 months, you know the Fed plans hike rates further this year.

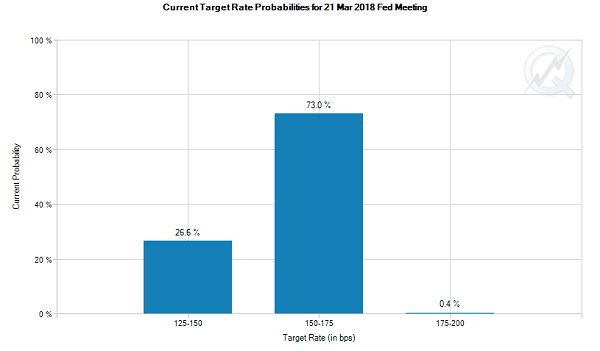

My colleague Michael Foster rattled off the reasons why in a November 21 article, but they boil down to rising wages, falling unemployment and an uptick in inflation, though it’s still below the Fed’s 2% target. That’s got futures traders pegging the next hike for the Fed’s March 21 meeting.

Source: CME Group

But whether we get the 2 rate hikes the market expects this year or 3 or more, as some talking heads predict, we can be sure of one thing: Powell will steer the same course as his predecessor, Janet Yellen.

How do I know?

Because he’s never dissented on any Fed decision since becoming a Fed governor in 2012, according to MarketWatch.

Which brings me to the relationship between rates and REITs, a linkage most people have 100% backwards—handing us a terrific opportunity to profit.

The Truth About Rates and REITs

Most folks think rising rates hurt REITs for 2 reasons.

The first: higher rates increase REITs’ borrowing costs … and it is true that REITs usually carry above-average debt to finance property purchases and renovations.

The second: that rising rates make so-called “safe” investments like CDs and Treasuries more appealing to income seekers compared to REITs.

Let me take the second point first.

As I write, the 10-Year Treasury yield sits at 2.5%, while the benchmark Vanguard REIT ETF (VNQ) pays nearly twice as much—4.3%. And plenty of REITs pay more, like a hotel operator I’ll show you in a moment that yields 7.0% today!

I think you’ll agree that this is still a big gap to close, and it will be a long time—if ever—before CDs, treasuries and the like manage to pull it off.

As for the first point, rising rates do increase REITs’ borrowing costs. But that’s only half the story! Because those hikes also come with a hot economy, which drives up rents and demand for the offices, warehouses, apartments and other properties REITs rent out.

The result? A rise in funds from operations (FFO, the REIT equivalent of earnings per share) that dwarfs higher interest costs and ignites REIT share prices.

If you don’t believe me, check the history. This is exactly what happened from July 2004 through June 2006, when the Fed hiked rates from 1.25% to 5.25%, and 10-year Treasury yields spiked to 5.14%.

How did REITs do? They soared 48%, including dividends, nearly tripling up the S&P 500’s gain.

Biggest REIT Myth Busted

The takeaway? Now is the time to buy REITs … especially if you see any of the ones on your watch list take a dip around the time of a rate-hike announcement (watch for that around March 21).

5 Top REITs From 2017 That Are Primed to Soar in ’18

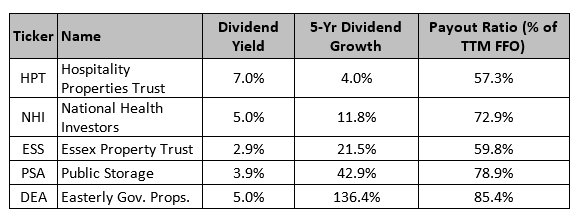

To get you started, I’ve pored over my last 12 months of ContrarianOutlook.com articles to bring you 5 solid REITs, each from a different part of the REIT market.

They are: hotel operator Hospitality Properties Trust (HPT), healthcare property owner National Health Investors (NHI), apartment landlord Essex Property Trust (ESS), self-storage manager Public Storage (PSA) and government building owner Easterly Government Properties (DEA).

All have strengths that safeguard our cash and set us up for gains in 2018. HPT, for example, owns 323 hotels that focus on business travelers and operate under household names like Radisson, Holiday Inn and Marriott. The REIT also cuts its reliance on hotels with its 199 Petro and TA travel centers, all of which are located along the interstate highway system.

These are terrific businesses that will grow as trucking freight volumes zoom ahead 3.4% annually through 2023, according to the American Trucking Association.

Essex, meanwhile, boasts 59,240 apartment units in prime West Coast markets like San Francisco and LA.

As I told you in a December 7 article, Essex is cashing in as millennials skip home ownership in favor of posh downtown pads, while baby boomers swap their suburban addresses for similar abodes. (Self-storage names like PSA, by the way, benefit from these exact same trends.)

Meantime, National Health Investors and Easterly Government Properties add ballast to our portfolio. NHI provides financing for steady medical tenants such as seniors’ housing facilities and specialty hospitals, while Easterly rents its 46 sleek, modern properties to government tenants like the FBI.

Your 5-REIT Portfolio: What the Numbers Say

So with that, let’s put our 5 REITs to the test, starting with 3 crucial numbers for us income hounds: dividend yield, dividend growth and payout ratio (dividends as a percentage of core or normalized FFO; a vital measure of dividend safety).

As you can see, these 5 names give us a nice mix of high yields and dividend growth. (A side bonus: as I recently showed you in an example using Boeing (BA), a rising payout is the No. 1 driver of stock prices.)

And all of those payout ratios (including DEA’s 85.4%) are easily manageable for these REITs, which benefit from rock-solid tenants (who wouldn’t want to rent space to Uncle Sam?) and high occupancy rates—DEA’s currently sits at an unheard-of 100%!

Finally, there are some real bargains in this bin. HPT, for example, trades at a ridiculous 8.3 times adjusted FFO, with NHI and DEA at an attractive 14.5 and 18.2 times, respectively.

It’s no surprise that the two priciest trusts are Essex (20.3 times core FFO) and Public Storage (20.6). But those are fair prices (they’re both below the S&P 500’s 21.8 and down from a year ago) considering these are two of the fastest dividend growers in our basket.

My take? I expect REITs to do a big U-turn in 2018, when the market finally realizes rising rates aren’t a threat—and these 5 are in a great position to benefit.

Revealed: The Best 8% Dividend for 2018

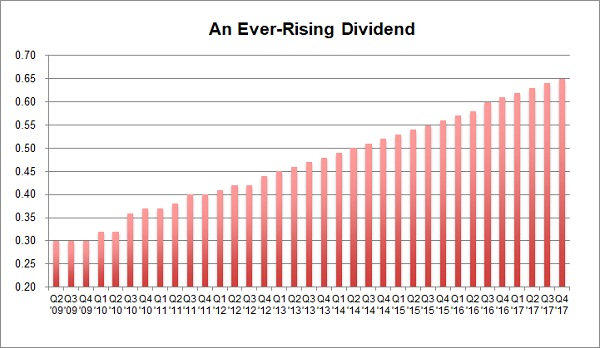

My top REIT pick for 2018 boasts an even higher dividend than any of the 5 trusts above (8% as I write this) and grows its payout every single quarter.

In fact, this powerhouse REIT has increased its payout for 21 straight quarters, so your forward yield is actually 8.4%, given that we’re going to see 4 more dividend hikes this year!

The best part? You can buy in cheap, at just 10 times FFO!

However, I expect this stock’s valuation and price to rise 20% in 2018 as the herd finally gets used to the fact that rising rates are here to stay—and that they’re actually a benefit to REITs.

That’s why I’ve made this unsung REIT pick a cornerstone of my “8% No-Withdrawal” portfolio, a collection of 6 investments from every corner of the market that I’ve assembled to do one thing (two, actually):

- Deliver a safe 8% average dividend yield: That’s enough to pay you $40,000 in income—enough for many folks to retire—on a $500,000 nest egg.

- Safeguard your retirement stash, letting you fund your golden years on dividends alone without drawing down your nest egg by a single penny! This insures your retirement against a market meltdown and lets you leave a lasting legacy for your kids (and grandkids).

I’m ready to share the names of all 6 stocks and funds inside this dynamic portfolio with you now. Click here to get the name, ticker symbol and full details on my top REIT pick and all 6 of these perfect retirement investments now.