“Buy and hope” investing has never been more hopeless.

With bond yields doing a “moonshot” to 1.8%, they are now looking down at the S&P 500’s sad 1.3% yield. Still, let’s admit—these aren’t enough for us to be able to retire on dividends alone.

Plus, we’re seeing serious volatility as the Federal Reserve hits the Pause button on its money printer. Basic income investors are losing these annual yields in one trading session!

Fortunately, there are serious dividends beneath the surface of the market. Today we’ll highlight five stocks that pay more than 7%. This is a big upgrade.

Back to the “spike” in bond yields. I jest because 1.8% still isn’t very much income. On a million dollars, this is just $18,000 per year.

The S&P 500—America’s retirement fund—is just as dicey. It pays just 1.3%, which nets only $13,000 on that million. Plus, it’s possible to give that entire payday back in one bad trading session.

I don’t know about you, but I prefer cash flow. Give me payouts that are 7% or better. This way, we can generate $70,000 on that million I mentioned. Or $35,000 on $500K.

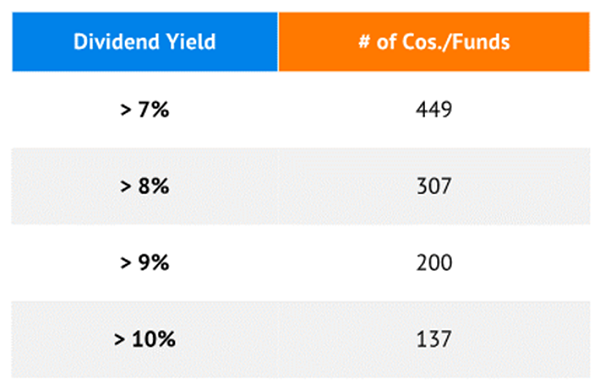

And believe it or not, there are 449 stocks and funds that yield more than 7% today. There are even 137 that pay more than 10%!

Number of Stocks and Funds with 7%+ Yields

Note: U.S.-listed companies and funds with market capitalizations or AUM greater than $300 million. Source: S&P Global Market Intelligence

Now many of these are what I call “dividend traps.” These are paper payout tigers that are in trouble. They are cheap for a reason.

It’s our job as contrarians to figure out which of these are unfairly cheap. Let’s look at five with big dividends between 7.4% and 16.1%. This is the type of homework that will indeed let us retire on dividends, and leave those 1%+ yields behind.

Global Net Lease (GNL)

Dividend Yield: 10.6%

Global Net Lease (GNL) is a commercial real estate investment trust (REIT) that operates not just in the U.S., but also developed Europe, providing a diversified portfolio of properties that helps it both grow and insulate it from inflation.

How diversified are we talking?

The company currently operates in 12 countries–including in the U.S., U.K., Germany, the Netherlands and Finland–where it boasts 312 properties split among 134 tenants in 48 industries. GNL does everything from financial services to auto manufacturing to tech to healthcare.

Tenants include the likes of McLaren—yes, that McLaren—FedEx (FDX), Whirlpool (WHR) and ING Groep (ING). And even amid a recovering economy, GNL’s properties are sitting at a high 99.1% occupancy rate.

The “net lease” part of its name is a real draw. GNL specializes in net leases, which means they’re “net” of insurance, maintenance and taxes—this REIT just collects rent and leaves the rest to the tenants. This eliminates three big variables. The result is Global Net Lease’s profits are more predictable and reliable than they would be sans-net.

The nearly 11% dividend is secure, requiring roughly 90% of adjusted funds from operations (AFFO). (REITs can pay up to 90% of their AFFO or FFO in dividends.)

GNL: Cheap Compared with VNQ?

Saba Capital Income and Opportunities Fund (BRW)

Dividend Yield: 12.6%

Saba Capital Income and Opportunities Fund (BRW) is a relatively new closed-end fund (CEF) that we discussed in August.

The skinny on BRW:

Saba Capital Income & Opportunities Fund has only been known by that name for a bit more than a month. Prior to June 22, it was the Voya Prime Rate Trust (PPR). So what happened?

A proxy battle.

Saba Capital Management LP is a hedge fund manager and activist investor that got Saba-nominated board members elected at Voya Prime Rate Trust last year. Those board members then picked Saba to replace Voya Investment Management Co. as the fund’s investment advisor effective June of this year.

The new BRW will primarily invest in high-yield credit, but it also says it “will also opportunistically target other investments, such as registered closed-end funds and special purpose acquisition companies.”

SPACs make up almost half of the portfolio, followed by senior loans, and a collection of corporate bonds, short-term investments and other CEFs.

Recently, in late December, the company announced it was targeting a 12% annual yield. So the fund upped its monthly dividend to 4.8 cents—nice.

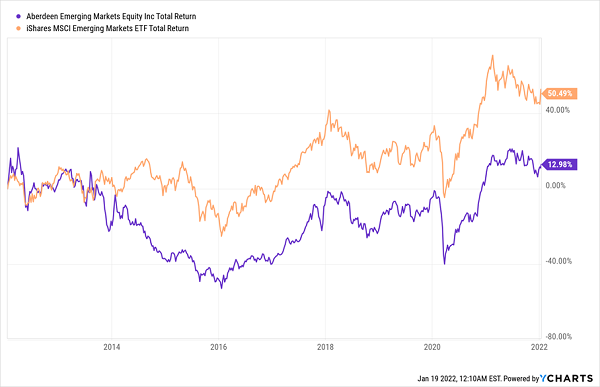

Aberdeen Emerging Markets Equity (AEF)

Dividend Yield: 7.4%

Aberdeen Emerging Markets Equity (AEF) is run like a basic index fund. It owns an emerging-markets portfolio of just 80 stocks, and it covers some of the biggest names in the game: Taiwan Semiconductor (TSM), Alibaba (BABA), Tencent (TCEHY) and more.

China is tops at nearly 30% of assets, followed by India and Taiwan at 13% each—all within a couple percentage points of the category average.

Where AEF really sticks out, however, is its yield. EMs are traditionally a font of growth, but Aberdeen’s closed-end fund manages to squeeze more than 7% in yield—typically all dividend income, not capital gains or return of capital—out of the emerging world.

The total returns are a bit disappointing, however. When AEF is on, the leverage helps amplify management’s good decisions—but the fund has been through a few long lulls that have really hampered longer-term performance.

Aberdeen Has Been Better of Late, But It Struggles Through the Dips

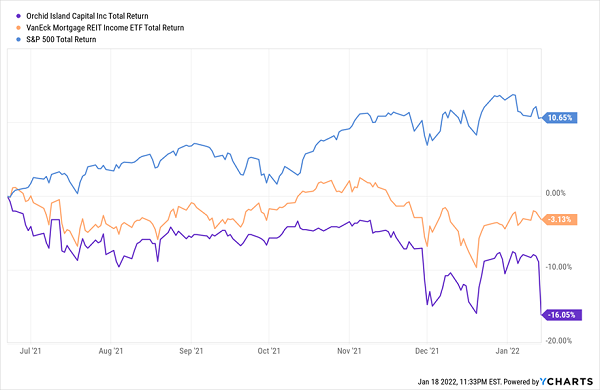

Orchid Capital

Dividend Yield: 16.1%

Orchid Capital (ORC) belongs to one of the highest-yield corners of the market: mortgage real estate investment trusts (mREITs). These so-called paper mills are different from traditional REITs in that they don’t invest in physical properties, such as malls or hospitals, but in securitized mortgages.

Orchid Capital, for instance, invests in residential mortgage-backed securities (MBS)—issued by the likes of Fannie Mae and Freddie Mac—on a leveraged basis. It makes profits on the difference between the yield on its mortgage assets, and what it costs to borrow. And in general, the threat of rising yields (and the actual rise in Treasury rates) have not been kind to the space.

mREITs Are Trailing as Fed Gets Hawkish

Unfortunately, ORC has been struggling on that front long before COVID. As I mentioned back in April:

“Quarterly earnings with gains/losses removed were as high as 70 cents per share in 2017 but have since dropped between the high teens and low 30s over the past year-plus. That has resulted in a steeply declining monthly dividend; ORC has chipped away at its payout four times since 2017, from 14 cents per share then to 5.5 cents through mid-2020, before hiking it back up to 6.5 cents currently. That’s simply too much dividend variability, regardless of how large the headline yield might be, for anyone planning out more than a couple years out into the future.”

Not only has the stock declined by double digits since then, but just last week, the company announced a 15% haircut to the payout, to 5.5 cents per share. The stock still yields an impressive 16% but I’m worried about how long until the next dividend cut.

Western Asset High Income Fund II (HIX)

Dividend Yield: 8.7%

Western Asset High Income Fund II (HIX) invests in high-yield corporates and emerging-market debt, then juices its picks by utilizing leverage (28% currently). It holds about 270 different debt issues with an effective duration of 6.25 years. Top holdings right now include Dish Network (DISH) bonds with a 7.75% coupon, and Range Resources (RRC) debt with a 9.25% coupon.

Over the past five years, HIX has beaten its popular ETF cousin, the SPDR Bloomberg High Yield Bond ETF (JNK), by a healthy 44% to 27% margin.

Live Off Dividends Forever With This “Ultimate” Retirement Portfolio

These five payers make for an interesting starting point, but if you’re looking to retire on dividends today, and you want a timely play, I recommend the “triple play” stocks in my 7%-yielding “No Withdrawal” retirement portfolio–have so much more to offer.

We all know you need enough income to cover all of your regular expenses. And we probably all inherently know that we should be holding high-quality stocks. But investors often overlook the importance of growing their nest egg in retirement – that way, if the unexpected happens, you won’t cripple your dividend-producing potential to dig out of trouble.

Get on Google and search for a set of “best stocks” by some of the mainstream financial outlets. I have—and after a few quick analyses of these “pro” sets of picks, I calculated likely total returns of between just 3% and 5% annually, based on so-so dividends and potential share appreciation from paltry estimated earnings growth now that the “recovery bump” is starting to be priced in.

Those kinds of returns will force you to bleed your nest egg dry just a few years after you retire. And you have worked too hard, for too many years, just to struggle financially in retirement.

My “No Withdrawal” portfolio features the best of several high-income assets. Of course, only a handful of stocks and funds meet my rigorous standards for this multipurpose strategy. But the result is an “ultimate” dividend portfolio that provides you with …

- An average 7% portfolio yield

- The potential for 10%-plus in annual capital gains

- Robust dividend growth that will keep up with (and beat) inflation

This portfolio will let you live off dividend income alone without ever touching your nest egg. You won’t have to worry about paying the mortgage or other monthly bills, nor will you have to wonder how you’ll survive if a financial disaster strikes.

Let me show you how to secure the comfortable retirement you’ve worked your tail off to enjoy. Click here and I’ll provide you with THREE special reports that show you how to build this “No Withdrawal” portfolio. You’ll get the names, tickers, buy prices and full analysis of their wealth-building potential – and it’s absolutely FREE!