Long-term interest rates have awoken. The trend toward higher Treasury yields is likely just getting started, which makes 2021 an “inflection year” for us income investors.

And what better way to celebrate the paradigm shift than to buy dividend payers that are likely to double (or better!) in the months and years ahead?

Sure, some fixed-income plays are going to be punished. That’s a topic for another time. Today, we should focus on shareholder-yield darlings that see their profits increase in an outsized manner when interest rates climb.

I’m talking about stocks that will shower us with:

- Current yields today,

- Dividend raises tomorrow,

- Generous stock buybacks, and (most importantly)

- Share prices that will climb dramatically.

I’m talking about “boring” old insurance stocks. These income-investor favorites are going to absolutely roll as interest rates rise.

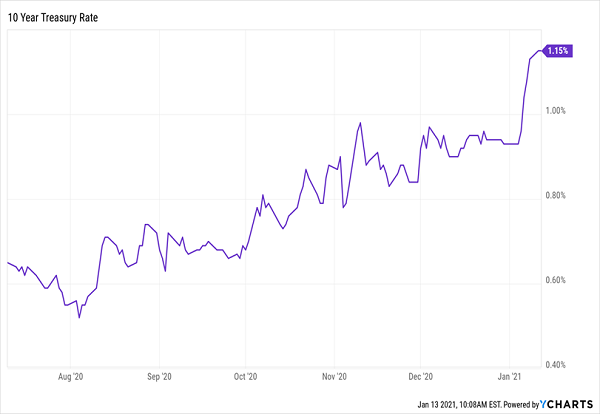

And make no mistake, rates are already rising, with the yield on 10-year Treasuries recently eclipsing 1%. That may not sound like a big move up, but remember that the T-note yielded just 0.5% in August, so 1% is an important psychological barrier.

Now that it’s breached that level, it could be off to the races. In fact, it already is:

Treasury Yields Soar …

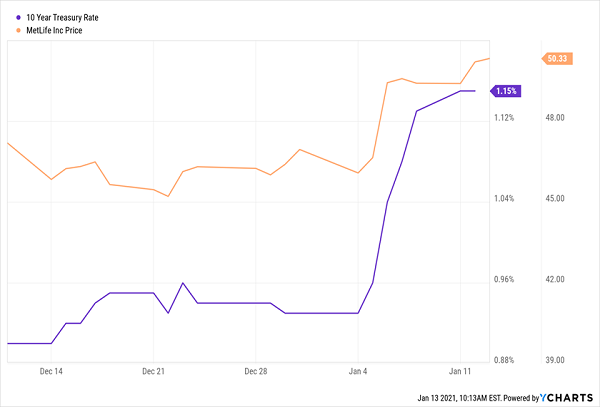

This is where insurers come in, because there’s a direct line between rising Treasury rates and their profits. You can see that connection in the shares of MetLife (MET), the biggest life insurer in the US by market share, which lurched higher with Treasury rates—and have tacked on a 7% gain since January 1 alone:

… Taking MetLife Shares With Them

That’s no surprise: investors are simply front-running the higher profits MET and other insurers are certain to see from higher rates.

I say “certain” because insurers are constantly investing the premiums they collect in, among other things, government and corporate bonds, and yields on those bonds rise with Treasury yields. Those higher yields fatten insurers’ net interest margins, or the difference between investment returns and claims paid out to policyholders.

2 Insurance Stocks to Buy for Rate-Driven Dividend Growth in 2021

Let’s stick with MetLife, because the company, which boasts $600 billion in assets under management, already puts us dividend investors in the starting blocks with a nice 3.6% yield.

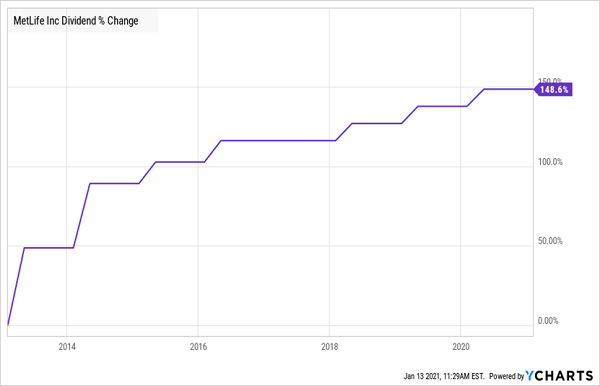

Speaking of dividends, back in 2013, the Federal Reserve let MetLife off the hook—MET had been classed as a bank-holding company and was therefore tied to payout-limiting stress tests. Since then, management has been footloose and fancy free with its dividend—and guess what? They were proven right.

MetLife’s Payout Lurches Back to Life, Grows Steadily

That’s a pretty big clue that the stress tests were unnecessary: MetLife pays just 14.4% of its last 12 months of free cash flow (FCF) as dividends today, so it could more than triple its payout tomorrow and still be well below the 50% of FCF I consider the dividend safety line.

Its balance sheet is also spotless, with long-term debt down 14% in the past five years and, at $18 billion, just 23% of its $780 billion in assets. And we can expect that percentage to shrink as rising rates inflate its assets.

And yet, despite all this, we can buy MET for a ridiculously low 8-times its last 12 months of earnings! The stock also trades at 61% of book value, or less than the value of its assets if it were broken up and sold today. (In other words, we’re basically getting its business, including its household-name brand, for free!)

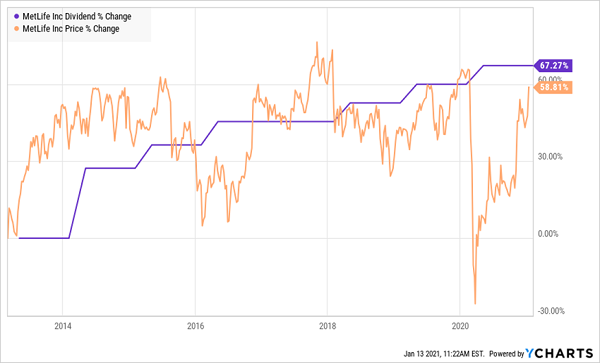

Throw in the rising 10-year Treasury yield and more dividend-driven upside (MET’s payout has pulled its share price higher since the Fed took off the shackles), and you get a recipe for even further gains:

MetLife’s Payout Pulls Up Its Price—Point for Point

Finally, MET recently resumed its buyback program, showing that management agrees that this stock is too cheap (a nice cue for us). The firm’s repurchases lead to fewer shares outstanding, helping boost the value of those still in circulation.

Another Insurer With Rate-Driven Upside

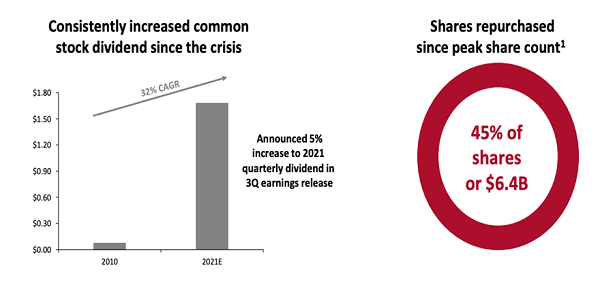

Lincoln Financial Group (LNC), the sixth-biggest life insurer by market share, trades at less than half of book value today—just 46%. That’s higher than the 30% of book at which it traded in late 2020, but it’s still near historic lows (and another case where we’re basically getting a landmark business for free).

It’s also ridiculous when you consider LNC’s sterling dividend-growth rate and the fact that it’s bought back nearly half of its outstanding shares in the last decade.

Source: Lincoln Financial November 2020 Investor Presentation

Those buybacks include 5.5 million shares repurchased between September 2019 and September 2020. The company did put its repurchases on hold in the third quarter of 2020, but I expect them to resume as rates rise, naturally increasing its assets under management and lifting its underwriting profits.

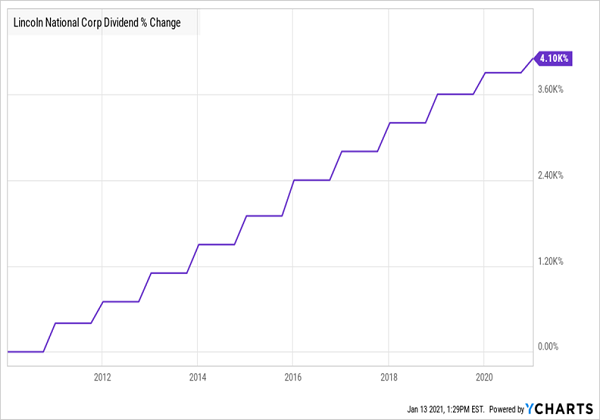

Buying now also gets you in on a devoted dividend grower: the payout yields 3.1% today and has exploded from just a penny a share (after LNC cut during the 2008/’09 crisis) to $0.42 today—a 4,100% increase in a little over a decade! Put another way, if you’d bought back then, you’d be yielding upwards of 6% on your LNC stake today.

Lincoln’s Payout Stair-Steps to the Sky

There’s more to come: even though LNC’s payout ratio is a slightly elevated 60% of its last 12 months of FCF, that still looks safe when you consider the impact of rising rates and the firm’s strong balance sheet, with just $6.7 billion in long-term debt, a small fraction of both its total assets (of just under $348 billion) and its cash and short-term investments (of $121 billion).

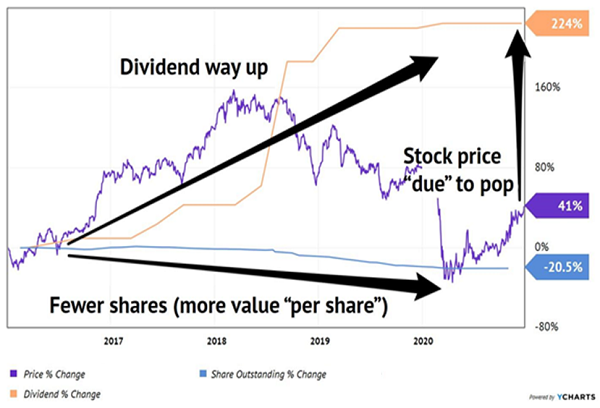

This Incredible Rising-Rate Buy Grows Dividends 224% (yours in 2 clicks!)

Let’s not stop with insurers. I’ve got another play for you that is, hands down, the easiest way to double our dividend money in 2021.

It’s a small, nimble firm with great relationships with its customers; it’s dirt cheap—like our two insurers, it trades for less than book value—AND it yields a gaudy 4.2%. Its dividend is en fuego, too, having popped 224% in just five years!

Throw in a raft of share buybacks and a share price that’s come “undone” from payout growth and you get a recipe for an EASY double here—in short order.

This Rising-Rate Play Gives Us 3 Ways to Win

Absolutely everything you need to know is on the front page of the January issue of my Contrarian Income Report service, which you’ll get immediate access to when you take a no-risk, no obligation 60-day trial today.

Big Yields, Big Gains—and CASH Dividends Paid to You Every Month

I can’t wait to share this pick with you—its dividend is poised to gap higher, yanking that share price right up with it. And you’ll get full access to it when you start your trial now.

That’s not all, either. You’ll also get an exclusive Special Report handing you my very best MONTHLY dividend stocks to buy now. These cash-rich dividend payers yield 8%, on average, and that payout stream is smooth, predictably rolling into your account every single month.

Don’t miss your chance to get in now and set yourself up for a full calendar year of monthly dividends. AND you’ll grab my brand-new rising-rate play for 224% payout growth, too. Your full report containing all the details on these 8% monthly payers, and the January issue with this new rising-rate pick, are waiting for you right here.