It may sound crazy, but if you were to invest $1 million in the S&P 500 right now, you’d generate just $1,750 in monthly income.

That’s just barely above the poverty line for a family of three.

When that much capital fetches such a pathetic amount of income, something’s wrong.

You came blame the Federal Reserve and its ultra-low interest rates. Or a retirement system that has thrown Americans to the wolves, replacing defined-payout pensions with 401(k)s that are too often designed to take—rather than grow—your savings with absurdly high management fees and low returns.

In such an environment, our parents’ retirement strategies just don’t work anymore. We need to go deeper to uncover income opportunities most people don’t take the time to learn about.

Which brings me to the wonderful world of closed-end funds, or CEFs.

These funds are often overlooked and sorely under-researched, partly because most 401(k) plans don’t let retirees invest in them. That’s too bad, because many CEFs offer very high yields, top-quality assets at a discount and sturdy income streams retirees can use to give their monthly cash flow a nice boost.

2 of My Favorite CEF Buys Now

In fact, right now I like two CEFs that boast a safe average dividend yield of 9.4%, which is more than four times the payout on your average S&P 500 stock.

What’s more, that 9.4% yield is backed by many of the same names you’ll find in the benchmark index (I’ll explain how this works in a moment), stocks like Apple (AAPL), Kraft (KHC), Home Depot (HD) and Microsoft (MSFT).

And because the market largely ignores these two CEFs, they trade at discounts to their net asset values (NAVs).

I know there’s a lot to unpack here, and the best way to do it is to dive into the first of my two fund picks, the Liberty All-Star Equity Fund (USA).

Right now, this CEF trades at a 16.1% discount to NAV. In other words, you’re only paying 83.9 cents for every $1 of stock you buy.

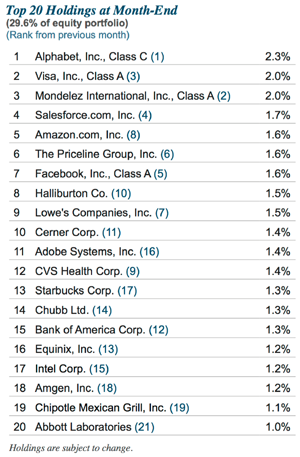

And for that 83.9 cents, you’re getting exposure to the fund’s portfolio of large-cap stocks, with both gain potential and attractive valuations. Here are its top 20 holdings right now:

Outsized Yields From Stocks You Know

Source: All-Star Funds

As you can see, quality holdings like Alphabet (GOOG), Visa (V), Mondelez International (MDLZ) and Salesforce.com (CRM) make up the bulk of the fund’s portfolio. At the same time, its 48-cent quarterly dividend means this CEF is paying out a 9.9% dividend on its current market price.

It’s a good illustration of how a fund trading at a discount to NAV—16.1% in USA’s case, remember—helps boost the yields on the stocks it holds.

That’s part of the explanation for these CEFs’ high yields. My next pick (which I like a little better than USA, to be honest), the AGIC Equity & Convertible Income Fund (NIE), shows another.

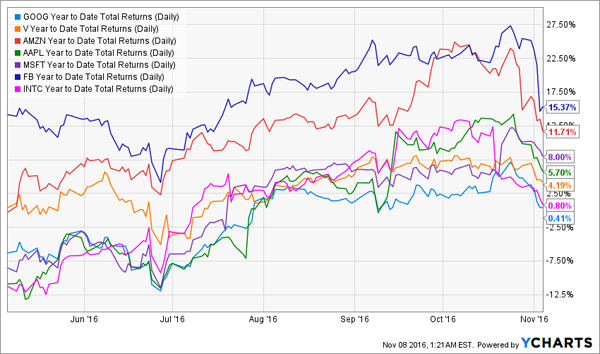

A Who’s Who of Top Mega-Cap Companies

Again, you can see that its top holdings are all instantly recognizable large-cap or mega-cap names, with favorites like Apple, Amazon.com (AMZN), Alphabet, Microsoft, Facebook (FB) and Intel (INTC) all making the list. On average, these stocks have risen 6.6% year-to-date, including dividends:

Quality Picks Beating the S&P 500

That’s almost twice the year-to-date total return of the S&P 500, which clocks in at just 3.9%. It’s also close to the fund’s outsized 8.7% dividend yield, which is possible thanks to NIE’s 14.1% discount to NAV. So for every dollar you invest, you get $1.14 in assets.

There’s more: the fund also uses covered calls and convertible securities to get an even higher yield on its assets. That’s helped NIE’s net asset value rise 7.0% year-to-date, and it’s likely to rise higher.

An Unbeatable 2-Fund Portfolio

Let’s bring it all together and say we buy these two funds. That instantly gives us a diversified large-cap portfolio of stocks across tech, health care, consumer staples, financial and other sectors. We also get a massive income stream, which is the main appeal of CEFs.

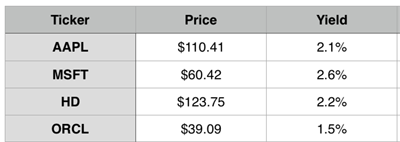

Now let’s compare our two-CEF portfolio with a four-stock combo that includes AAPL, MSFT, HD and ORCL, which both funds hold.

Stable Stocks, Middling Income

Our average yield will be 2.1% in this portfolio because we’re getting safe, reliable stocks with high operating margins and strong cash flows.

But thanks to their discounts to NAV and, in the case of NIE, the use of call options and other strategies the fund’s managers employ, our two funds offer us exposure to those exact same stocks, with the same fundamental strengths, but with a higher dividend yield, in addition to dozens of other companies.

Sharp Managers, Big Discounts Deliver Higher Yields

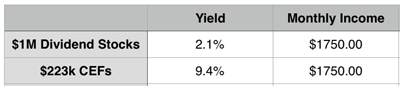

Now we have a portfolio with an average 9.4% dividend yield. This means we can reach the same stream of passive income with much less capital than we’d need if we simply stuck with our four-stock portfolio.

In fact, remember our millionaire living in poverty? I can easily recreate their $1,750 monthly income stream with just $223,000, thanks to the 9.4% yield on these two funds:

The Same Income as the S&P 500 … With 78% Less Capital

As you can see, I’m getting the exact same assets but I’m paying less and getting more cash in hand right now.

There are many things I can do with that cash. I can invest it in these CEFs, for example, or diversify into other high-yielding funds. I can even buy the same low-yielding safe stocks my two CEFs hold and sit tight while their dividends grow and their stock prices rise.

If I choose the first option and reinvest in these and other high-yielding funds, something truly magical happens:

Big Growth With No Extra Investment

I go from $223,000 in capital to over $320,000 in five years without adding any extra money to my portfolio. What if I did this instead with low-yielding dividend-growth stocks? See for yourself:

Low Growth With No Extra Investment

I end up with a bit over $244,000 in five years, assuming dividends grow by a consistent 7.0% every year and I don’t reinvest any more of my capital into the portfolio.

Clearly, the CEF approach works on a short time horizon, thanks to the outsized income stream these funds produce. This makes them ideal investments for retirees who need an income stream now.

In fact, CEFs’ hefty payouts are one reason why we’ve included them in our “No-Withdrawal” retirement portfolio.

As the name suggests, it lets you sail through your golden years without having to tap a penny of your capital. (The three CEFs in the portfolio yield 7.4%, 8.0% and 9.4%, respectively. You can learn more about them here.)

Best of all, you won’t need a portfolio in the mid-seven digits to do it—as you would if you limited yourself to the misers of the S&P 500.

This is the way everyone should be thinking about retirement because it gives you an extra layer of protection in the next downturn.

Back in 2008, for example, many so-called “safe” stocks slashed their dividends, forcing retirees to unload stocks at fire sale prices to make up the difference—slashing their income even further.

That’s a nightmare scenario no one should have to live through, and it’s why we built our “No-Withdrawal” portfolio … so you can skate through the next panic, quietly collecting reliable dividend checks while the market recovers.

Our simple strategy revolves around just 6 often-overlooked high-yield investments, including 3 CEFs trading at 10% to 15% discounts to NAV.

This gives you strong upside potential as that gap closes … and even if the market takes a tumble, these top-notch funds will simply trade flat, and we’ll still collect those fat 7.4% to 9.4% yields. Click here and I’ll show you our complete strategy, the 6 rock-solid investments that back it up, and how to make sure you never need to sell a stock or fund when the market is tanking.