“Coach Brett, how many points do I have?”

My star player, Captain K, was dominating the basketball game. He’d steal the ball, storm down the court, and drain the shot. Then retreat into a defensive position and do it all over again.

Two points after two points after two points. I’d have lost count if I had to count. Fortunately though, we weren’t keeping score.

Most leagues these days don’t keep score when the players are only five years old. The run is more important than the result.

But my man K knew he was “killing it,” as his dad told him from the sidelines! So, your investment strategist—and Saturday morning coach—wondered if he could inspire K to involve his overwhelmed teammates.

After all, our opponents were doing their best to swarm our star player, but he was scoring anyway. But maybe, just maybe, he could drop a pass off to a teammate for a wide-open shot? A potential glory moment?

“You know K, for really good players, it isn’t always about how many points they score.”

I paused for effect.

“Sometimes their greatness is defined by how many points they can get for their teammates.”

Our most valuable player stared at me, unimpressed.

“Isn’t that cheating?”

He walked away. I cracked up. In the literal sense, he was 100% correct—players cannot in fact score points specifically for their teammates.

I had jumped ahead to the advanced concepts of drawing defenders and passing to wide-open teammates. Generating easy shots. Points for them, if you will—which, yes, they score for themselves!

This is perhaps a legal way to “cheat.” Or gain an advantage. It’s within the rules. I’ll have to explain that in a future practice.

(To his credit, my man K did drop two beautiful passes to teammates after our talk. Perhaps my words got through. Or perhaps I analyze five-year-old hoops too much.)

What’s the equivalent of “legal cheating” in the dividend world? That’s easy: Buying closed-end funds (CEFs) at discounts. It’s literally a free lunch. (Like what we treated our players to after the Big Game.)

Four months ago, we highlighted DoubleLine Yield Opportunities (DLY) as the maraschino cherry of bond funds:

It’s run by the “Bond God” Jeffrey Gundlach and his crew, yields 10% and trades at an 8% discount to its net asset value (NAV). A cherry indeed!

Here’s how that works. The bonds that DoubleLine owns in DLY add up to an NAV of $15.28. But as I write, the fund trades around $14 per share.

This means we have an 8% discount window (eight-point-three percent, to be exact). If and when this window shuts, as it has for DLY’s two sister funds, it will equal price upside for us.

That window is already half shut. DLY now trades for ninety-six cents on the dollar, 4% narrower in four months.

DLY’s total return since then has been—wait for it—4.3%, which annualizes to 13%+! Which, of course, is splendid for a safe bond fund.

The fund is still a decent deal here, yielding 9.6%. Nothing to sneeze at! Sister fund DoubleLine Income Solutions (DSL) has already seen its markdown disappear. Opportunistic investors may want to grab some discounted DLY (pronounced “dilly” by the DoubleLine team) before it’s fully priced.

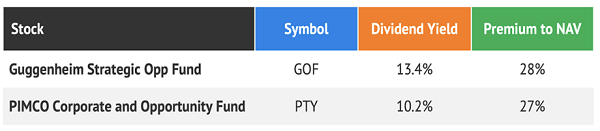

Guggenheim Strategic Opportunities Fund (GOF), meanwhile, is the “bad shot” of bond funds. GOF trades at a 28% premium to its NAV. Which is a 32% surcharge over the DLY.

Guggenheim is a fine shop. But c’mon, they don’t have a fixed-income deity like Gundlach at the helm. (Who does?)

As a value-focused investor, I’m hesitant to pay $1 for $1 in assets. We contrarians demand discounts. Paying $1.28 for a mere $1 in bonds is pure insanity.

Can it work? Sure, if you have years… But we’re not chucking up half-court shots here at Contrarian Outlook. We’re playing the dividend percentages.

Investors are being lured by GOF’s 13.7% headline yield. That’s great, but the fund has 28% downside if it merely trends towards fair value. No thanks!

GOF is the biggest bad idea on the bond board. Its runner up is PIMCO Corporate and Opportunity Fund (PTY), trading at a nearly-as-offensive 27% premium to its NAV.

Yes, PIMCO is a primo bond shop. It’s been so since the days of the “Bond King” Bill Gross.

Like all kings, Gross was deposed years back. For good reason—PIMCO had his successor already identified in the form of Dan “Beast” Ivascyn (yes, that’s actually his nickname on the Street).

Who doesn’t want to invest alongside a bond Beast? (we’ve got the God, so why not the Beast?) I get the love for PIMCO, but I pity the fool who buys PTY!

If you’re going to insist on investing with PIMCO, why not cut that 27-cent premium down to three? PIMCO Dynamic Income Opportunities Fund (PDO) trades at 103% of NAV. Not exactly a steal, but a heck of a better deal than PTY at 127% of NAV. Plus, PDO yields more!

Ideally, we do demand a discount. Why choose between a big yield and steady upside when we can have both?

Payouts plus price appreciation equal retirement perfection. And right now, thanks to the manic markets, we have some ideal dividend payers flashing buy signals. Please read on and I’ll explain what these “dividend machines” are and where they fit in The Perfect Income Portfolio.