Interest rates are the talk of the bond world right now. They are going up for once!

Does this mean we should book profits on our fixed-rate bond positions? They have benefited greatly from sliding interest rates throughout 2019 (and that’s an understatement).

Most income investors are thrilled to see 4% or 5% returns from their bond funds. What they wouldn’t give for the eight-pack of “bond moonshots” we contrarians have enjoyed for 25% average returns!

How We Made 25% in 11 Months with Safe Bonds

Yet I’m sitting here at the Inside Fixed Income conference (the bores I endure for you, dear subscriber) in San Diego, California (well… never mind) hearing about the $74 billion now held in bond ETFs. And there’s a hint of rising rate fear in the air.

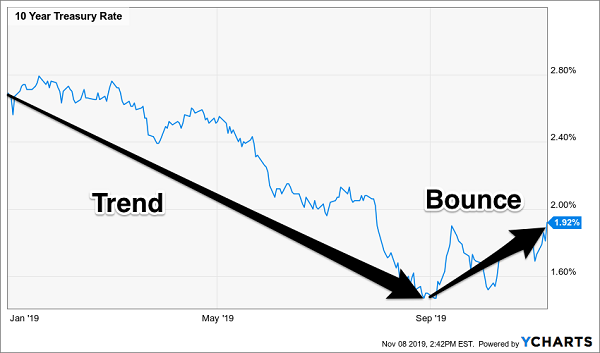

The 10-year Treasury yield dipped below 1.5% in early September, yet it’s bounced back towards 2%. In percentage terms this is a big move. But let’s put it in perspective with respect to the 10-year’s action year-to-date. It’s a bit early to call a trend change!

Putting the 10-Year’s Rally in Perspective

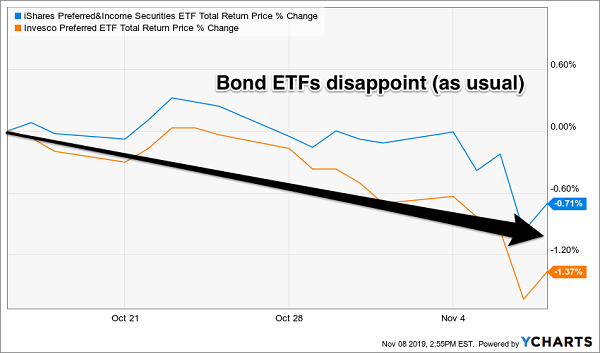

Popular bond ETFs, the vehicles collecting the bulk of the $74 billion, have sold off a bit with the 10-year yield rally in recent weeks. The two big bond preferred ETFs, iShares Preferred and Income Securities (PFF) and Invesco Preferred ETF (PGX), steward over $22 billion of that money. Their job is to collect income with price stability, and in recent weeks they have begun to falter on that stability part:

Preferred ETFs Have Reacted Poorly

Not familiar with preferred shares? You’re not alone. A company will issue preferred shares to raise capital, just as it offers bonds. In return it will pay regular dividends on these shares and, as the name suggests, preferred shareholders receive their payouts before common shares.

A big problem with preferred shares is that they are complicated to purchase without the help of a human broker. So, many investors attempt to streamline their online buys and simply purchase ETFs (exchange-traded funds) that specialize in preferreds, such as PFF and PGX.

But do PFF and PGX investors even know what these ETFs actually hold? Or do they see their promised 5% to 6% yields, turn their brains off, and buy them assuming that they must be reputable because after all they are “well-known” ETFs, issued by big names iShares and Invesco?

The problem with the ETF model is that it doesn’t account for credit risk as accurately as an expert human can. Which means a better idea is—you guessed it!—to find an active manager to handpick your preferred portfolio. Buying a discounted closed-end fund (CEF) is the best way to do this.

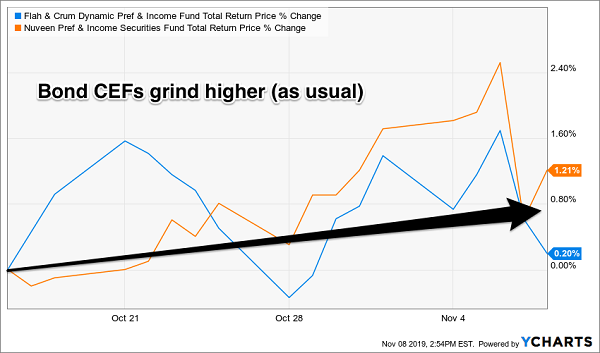

We’ve seen this time and again, most recently over the past few weeks. The two preferred CEFs we hold in our CIR portfolio have held up just fine during the recent bout of interest rate worries:

Preferred CEFs Have Reacted Well

Really, it’s no surprise. CEFs are simply a better way to buy bonds. The $74 billion, if not quite dumb money, isn’t being terribly smart or savvy either.

You’ll rarely get a deal buying an ETF. They don’t trade at discounts because their sponsors simply issue more shares to capitalize on any increased demand. We CEF investors don’t have this popularity problem; we can get a deal. We simply wait and only purchase CEFs when they trade at a discount to their net asset values (NAVs, or the sum of the market prices of the preferred shares they own minus any leverage).

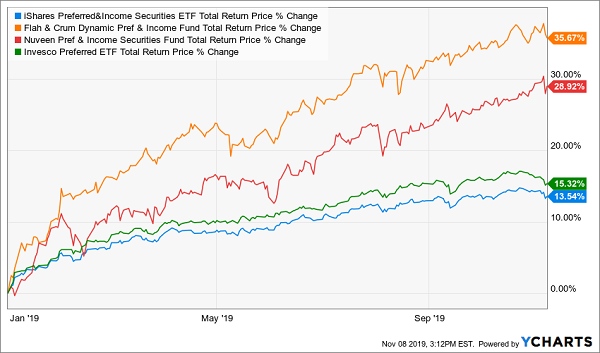

The Invesco Preferred and iShares US Preferred ETFs trade at their “par” value, which means we’re paying $1 for $1 in preferred shares. Meanwhile, many preferred CEFs often trade at discounts to their NAVs. Plus, they have the benefit of an active manager, which is why the funds regularly outperform their ETF counterparts, just as they did over the past year:

Preferred CEFs (Top 2) Crushed Preferred ETFs (Bottom 2)

Another great feature of these “best bond funds” is that they pay their dividends every single month. If you share my affinity for monthly dividends, then check out my best “monthly payer” buys.

5 More “Fed-Proof” Monthly Dividends Up to 9.1%

My Contrarian Income Report portfolio boasts 5 more monthly paying stocks and funds that are screaming buys now, as the market sits on pins and needles, waiting for Fed Chairman Powell’s next change of heart.

Each of these income powerhouses gives us the sky-high yields (7% on average, with one paying an incredible 9.1% in cash!) and steep discounts we need to thrive, no matter what happens with the Fed—or the economy.

They’re just a click away—all you need to do is take CIR for a quick, no-commitment road test to get your hands on these 5 cash machines now, plus all 19 income plays in this dynamic portfolio (average yield: 7.4%; highest yield: 9.1%!).

That’s not all, either, because you also get …

“Monthly Dividend Superstars: 8% Yields With 10% Upside”

This breakthrough Special Report lays out my very best monthly paying buys. You’ll discover:

- An 8.6% payer that’s set to rake in huge profits from an artificially depressed sector.

- The brainchild of one of the top fund managers that’s giving out generous 9.1% yields.

- A “steady Eddie” high-yielder that barely blinks when stocks plummet. (This one is my favorite “Fed insurance” play of all.)

This is, hands-down, the biggest collection of 7% monthly paying buys ever assembled. Click here to get full details on these cheap, high-paying monthly dividends—names, tickers, buy-under prices and everything else you need to know before you buy.