Natural gas prices have been completely washed out—and that’s set up some sweet dividend opportunities for us contrarians to tap into.

(These opportunities aren’t just in gas, by the way: China’s reopening and the Biden administration’s need to refill the Strategic Petroleum Reserve—which it’s been using to keep a lid on oil prices—will also lift the goo. We discussed 3 stocks to play crude’s likely rebound on February 4.)

To get a sense of the opportunity setting up for us here, let’s look ahead to next winter, shall we? It’s tough to see how gas can stay low with a setup like this:

- Russian gas will still be a no-go—leading to another dash to boost European supplies over the summer, especially with the current winter looking like it’ll end on a cold snap, draining off the surplus gas the continent is sitting on now.

- China will be fully reopened. There’s no way COVID controls are coming back after Xi’s epic climbdown.

- Supplies are tight in Asia, as Europe hoarded LNG shipments in its scramble to make up for lost Russian supply. With the IEA projecting the Asia-Pacific will account for half of the expected growth in gas demand up to 2025, something’s got to give here, especially as …

- Global supplies can’t keep up, as producers race to tap new sources in places like the Permian Basin in the US.

This is why gas still has a multi-year rally ahead. The fuel, along with oil, is still in the “rally” period of our “crash ’n’ rally” pattern, which is one of my favorite indicators for energy investing.

Here’s how it played out in the wake of both the 2008 and 2020 crashes:

- Demand for energy evaporated and prices crashed quickly (2008 and 2020).

- Energy producers scrambled to cut costs, so they cut production aggressively.

- The economy slowly recovered (2009 and late 2020), energy demand picked up, but supply lagged.

- And lagged. And lagged. And energy prices rallied until supply eventually met demand (2009-2014 and 2020-present).

This predictable multi-year cycle is why I consider this pullback in oil and gas a short-term “second chance” for investors who missed the first big energy dip. For those who joined the binge in energy stocks we went on in my Contrarian Income Report service in 2020, it’s a great time to dollar-cost average in.

The best way to play a dip? Through “tollbooth” stocks like Williams Companies (WMB), which yields 5.6% today and has 30,000 miles of pipeline and handles 30% of the natural gas in the US.

Williams is nicely positioned to benefit as gas supply and demand rise. And with gas being the least offensive of the fossil fuels, it’ll remain a big part of our energy mix for some time. But even so, the world is turning toward renewables and Williams is smartly keeping that in its plans, laying an impressive emissions gauntlet for itself:

- A 56% reduction from 2005 of company-wide greenhouse gas emissions.

- Net-zero carbon emissions by 2050.

Management believes it can make early progress simply by upgrading equipment and scaling its renewable energy (impressive!). It is also expanding solar initiatives in nine states.

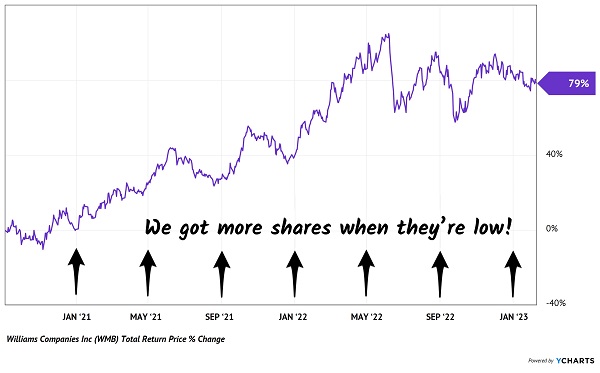

My Contrarian Income Report subscribers and I are sitting on a nice 79% return (and locked in a 7.7% yield on our initial buy) on Williams since September 2020. But the stock can be volatile, which brings me back to dollar-cost averaging.

If you’re not sold on the coming nat-gas rally, or you’re worried about a deep recession, we can give ourselves a nice “hedge” by following a DCA approach with energy stocks like WMB.

That’s because, even though WMB has already built up its infrastructure and most of its cash flows go to dividends, the stock price moves more than you might think:

WMB’s Twitchy Drive Higher

That’s actually an opportunity for our savvy DCA’ers. By buying a fixed amount every few months, we naturally acquire more shares when prices are low. Effective and easy market timing!

What’s more, we avoid the mistake of going “all in” at the top. For WMB, that moment came in June 2022, when the stock topped out near $38, as gas prices spiked near $10.

No matter how we choose to buy in, the bottom line is that I expect a rally in natural gas and oil to play out for years to come (with the occasional pullback like the one we’re seeing now). Williams is smartly set up to profit—as are the other three “Crash ’n’ Rally” energy dividends (yielding up to 7.4%) in our CIR portfolio.

Get All 4 “Crash ’n’ Rally” Picks—Plus 3 Monthly Dividends Up to 12%—Now

If you want to take full advantage of the coming surge in oil and gas, I urge you to own all four of our “Crash ’n’ Rally” picks. You can get their names, tickers and my research on all of them when you take a no-risk 60-day trial to Contrarian Income Report.

What’s more, I’ll throw in a complementary report—“Monthly Dividend Superstars: Yields Up to 11%.” This exclusive briefing names three monthly payers I see as must buys now.