Buying real estate investment trusts isn’t like buying other stocks; despite their high yields and big long-term returns, REITs require a bit more attention and a bit faster action than more popular dividend-payers, like blue chips and dividend-growth stocks.

But it’s more than just speed and care. To win with REITs, you need to follow three rules—and I’m going to show you those today.

These REIT rules have never been more important than they are now. Broadly, REITs are getting more valuable, but the market is getting more scared of them. This disconnect makes no sense and is partly the reason why two extremely healthy and valuable REITs—Sabra Health Care REIT (SBRA) and Care Capital Properties (CCP) recently merged.

In their announcement, both firms said the merger would save $20 million in costs annually, provide greater diversification and give the new company more cash for expansion.

The market’s response? Both REITs have plunged in recent days, giving both negative returns since CCP’s IPO in 2015:

Markets Cautious on REITs

At times, drops like this gave contrarian investors a great opportunity to get both SBRA and CCP on sale when the stocks were ridiculously oversold. Like back in November 2016, when buying SBRA was a no-brainer: it was absurdly undervalued due to a plummet in price without a drop in earnings, capital access or expansion.

Selling SBRA after the merger announcement also made sense, because the market is worried that the combined company isn’t going to deliver on management’s promises. The market is wrong on this, which means waiting for both Sabra and CCP to bottom and then jumping in again might be a good idea.

This brings us to our first rule of successful REIT investing.

- Get the Timing Right

Many things affect REIT pricing, but the biggest is whether there’s a better alternative out there. That’s always changing, of course, which is why the ratio between a REIT’s funds from operations (FFO, the metric used as earnings per share is used for stocks) and its price can change by 30% or more in a matter of months.

And as my colleague Bill Stoller recently pointed out, REIT investors—like all investors—can be fickle; their confidence in a particular REIT or REIT sector can vanish easily, again causing big price swings.

This all means we need to take a closer look when a REIT has fallen extremely quickly in a very short period. Ask yourself: is there a good reason for this fall, like a steep decline in the value of the company’s assets, an explosion of debt without accompanying growth or changes in management that aren’t good for investors? If you can’t find these smoking guns, it’s probably an irrational panic that you can profit from.

- Compare FFO and Pricing

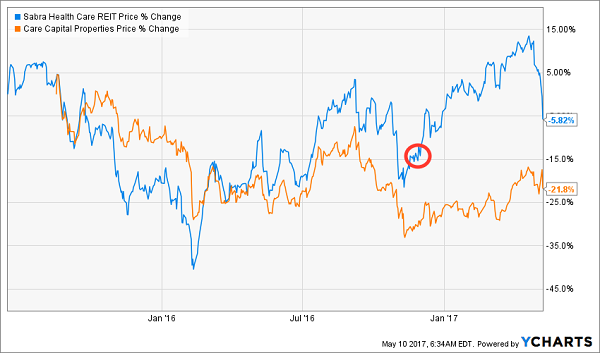

Finding the details in Rule No. 1 isn’t easy. But it is easy to take a quick look at REIT price and FFO and get a sense of whether there’s disaster or opportunity ahead. Are there any radical disconnects between the two? In the case of SBRA, one became apparent in late 2016, as you can see in the red circle below:

Weakening Price, Rising FFO

Notice how prices fell in late 2015, shortly before FFO plummeted, then rose again in early 2016, just before FFO began to rise? That’s the market anticipating changes in the company’s FFO and pricing the stock accordingly.

But then in late 2016, something odd happens—FFO showed no signs of dropping and was about to soar past its 2015 level, yet prices went down suddenly and sharply.

Why? Think back to November 2016. President Trump was just elected, and the market saw this as great for inflation, interest rates and financial stocks. But it was also seen as a bad thing for REITs, so the entire sector took a dive.

This was a rare moment when temporary hot-button issues overshadowed the fundamentals in a REIT—and created a buying opportunity.

When it comes to REITs, we need to wait for those rare moments when the market stops focusing on fundamentals and drops the ball.

Of course, the market quickly realized its mistake and started recovering almost immediately, so Sabra was back to its pre-Trump election level before January. Then it was up nicely just before the merger news. That means there was a nice window of six months in which investors could capitalize on the market’s mistake.

The key takeaway? Ignore the noise from the news, focus on how FFO is trending and take note when the market stops focusing on fundamentals and punishes a REIT unfairly. Then jump in.

- Buy at a Discount

In other words, you need to buy REITs at a discount and constantly look at the stock’s price trend alongside quarterly earnings reports to see if that discount is disappearing or not.

Sound hard?

It is. Instead, some investors just give up and put their money in a REIT index ETF, like the SPDR Dow Jones REIT ETF (RWR). This is a bad idea for two reasons.

Firstly, with an index we’re getting winners and losers because no one is digging through the REITs. Secondly, there’s no churn—the fund isn’t offloading REITs when they’re overvalued and buying when they’re undervalued, so we’re not really taking advantage of the emotional swings of the real estate market.

On top of this, the fund’s yield is weak; we’re going to get a 5.2% dividend when we can get over 7% elsewhere.

Where?

In closed-end funds (CEFs). These more actively managed funds can take advantage of changes in the real estate market to buy and sell REITs when it makes sense to do so. That gives them the opportunity to produce bigger capital gains while accessing the income of high-quality REITs, and that translates into higher dividends.

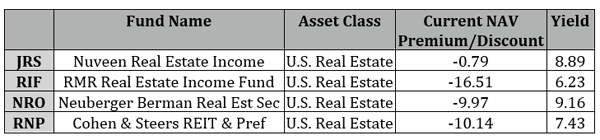

Let me show you four such REIT-focused CEFs: Nuveen Real Estate Income (JRS), RMR Real Estate Income Fund (RIF), Neuberger Berman Real Estate Securities Income Fund (NRO) and the Cohen & Steers REIT & Preferred Income Fund (RNP).

And as I wrote back on May 2, CEFs are a great way to buy REITs at a big discount. And all four of the above funds are trading at discounts to net asset value (NAV, or the value of their underlying assets), although their discounts vary, from less than 1% to over 16%:

That means we’re not only getting access to professional analysis of REITs, we’re also getting that for less than we’d get REITs for with RWR, which doesn’t trade at a discount at all.

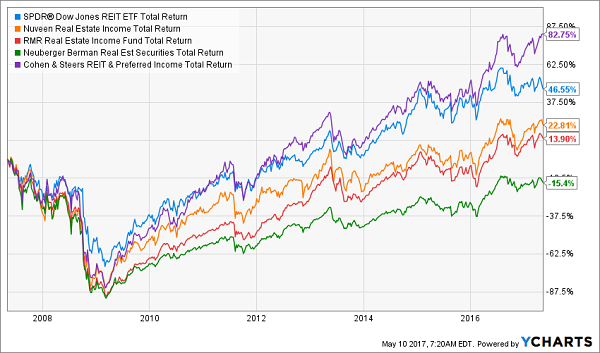

But you have to be picky. Not all CEFs are good—and many are horrible. This is as true with REIT funds as it is with anything else. If we look at the last 10 years, we see that only one of these four REIT funds has beaten RWR on a total-return basis:

CEFs Deliver Mixed Performance

CEFs demand a close look to pick the winners from the losers; when you take that close look, you can pick a fund that almost doubles the index’s performance over a decade, like we see Cohen & Steers delivering with RNP. And that’s not the only fund to offer this superior return.

4 More CEFs With Double-Digit Upside and 7.5% Yields

Here’s the bottom line: if you’ve been searching in vain for bargains in today’s overstretched market (who hasn’t?), you need to take a look at CEFs.

This long-ignored corner of the market (there are only around 600 CEFs in all) is bursting with deals and other weird situations we can jump on and ride to easy double-digit gains.

Take RNP—which has soared 83% in a decade and still trades at a 10% discount! Try to find a “regular” stock like that.

I know. Fat chance, right?

Even better if you can find funds trading at discounts wider than their historical norms. Find this simple disconnect, jump in and get ready for serious upside on top of your 7%+ income stream.

Rinse and repeat.

And if that sounds like work, don’t worry. I’ve done it all for you, poring over the entire CEF universe to sift out 4 funds whose ridiculous discount windows are about to slam shut. When they do, I fully expect their prices to explode for 20%+ upside—at least—in the next 12 months!

And when you throw in their outsized yields—7.5%, on average, as I write—you’re looking at an easy 30% in dividends and gains here.