From 1994 to 2014, self-storage REITs (real estate investment trusts) rewarded investors handsomely. They delivered 18% annualized returns with lower volatility (less drama) than their REIT peers.

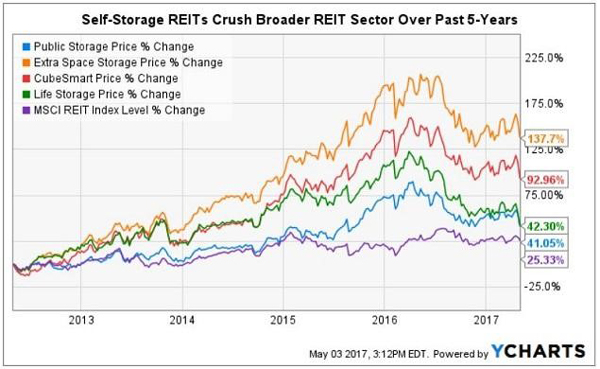

But the past year has been brutal for shareholders of the Big 4 self-storage REITs. The storage sell-off has included sector blue-chip Public Storage (PSA), as well as Extra Space Storage (EXR) a top REIT performer for the past decade. The selling has not spared investors in CubeSmart (CUBE) or Life Storage (LSI), the re-branded Sovran Self-Storage (Uncle Bob’s).

This horrible performance over the past 12-months has come as a shock for most REIT investors who have come to expect handsome dividend increases and higher prices from these names.

Self-Storage Rewarded Investors Handsomely

REITs, by law, must pay out at least 90% of taxable income as dividends to shareholders. This requirement leads savvy investors to REITs for higher yields.

The Vanguard REIT ETF (VNQ) tracks the MSCI REIT Index (RMZ) which includes a majority of property REITs, as shown in the chart above. It is a safe way to gain exposure to high-quality commercial real estate for many retail investors.

However, even after recent price erosion, self-storage REITs have rewarded investors with as much as 5-times the price appreciation as VNQ.

Is this a buying opportunity in self-storage? Let’s look at the sector’s fundamentals today.

What Went Wrong?

First, it’s important to understand what has changed the fortunes of the Big 4 storage REITs.

The main drivers for self-storage success are population density, household income, and the four “Ds” — divorce, death, downsizing and dislocation. Think of dislocation as a college student leaving, or a millennial coming back home to live in the basement.

In the years following the Great Recession, there were relatively few new self-storage units built. Local developers could not get financing from regional banks. The public REITs had pulled back on any new development. This created a Goldilocks environment where occupancy and rental rates just continued to rise, year after year.

But, it gets even better. The big REITs developed a huge technology advantage over the mom and pop operators that own 85% of the storage facilities. Google internet searches replaced the Yellow Pages as the primary way new customers began their search. These big operators make sure they always come up first in search results. Today, smartphones and mobile devices are even more important.

The public REITs also have 24/7 call centers and state of the art revenue management systems which guide pricing at the store level. They can immediately respond to changing market conditions, (since all self-storage markets are hyper-local). Who wants to drive clear across town to access a storage unit?

However, the boom times could not last forever. Beginning in 2016 brand new self-storage facilities began to spring up in many markets. This trend is accelerating in 2017, and forecast to continue into 2018, causing supply/demand imbalances in multiple US markets.

Remember, each new storage development starts out 100% vacant. It can take three years to reach break-even or better. This means that especially in smaller markets, even a little overbuilding creates a dynamic that can impact existing store performance.

The Big 4 self-storage REITs have operations in many markets across the US and some locations have been impacted more than others. Remember, several years of increasing occupancy, higher in-place rental rates and raising of “street rates” have made year-over-year comparisons increasingly difficult. The excess supply is a revenue and same-store NOI headwind – especially if you were already operating at record occupancy.

“The Big 4 self-storage REITs have recently pulled-back, and are once again worth consideration. Public Storage is a blue-chip with an A rated balance sheet, Extra Space Storage has been a top performer in the past. CubeSmart offers investors a low-payout ratio for sustained dividend growth and Life Storage the highest current yield for income-focused investors.

However, there happens to be a better way to profit from the security and earnings growth self-storage can offer to long-term investor.

Best of Both Worlds for 47% Dividend Growth

Before you decide to buy shares in any of the Big 4 storage REITs there is another name we recommend as our top self-storage sector pick.

What if there were a smaller group of seasoned regional operators that decided to band together? Imagine veteran self-storage operators who can sharpshoot local markets, all operating profitably – but with room for improvement that only technology and big data can offer. Now add access to low cost Wall Street to fund the continued growth of this cash cow.

In our dividend-growth focused Hidden Yields service, we recommend a little-known gem that continues to succeed by delivering income and price appreciation for shareholders, despite the struggles of the Big 4 REITs!

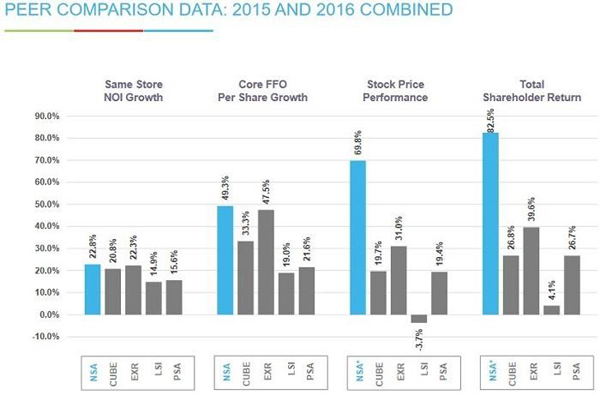

In fact, this top sector pick has outperformed the Big 4 self-storage names on every metric including total shareholder return since its IPO in 2015 — and the shares have continued to increase in value in 2017.

It gets even better when you consider dividend increases, the real engine behind the share price outperformance.

Our Storage Play (Blue) Beats the Big 4 (Gray)

Our favorite self-storage play is one of our 7 favorite dividend growth stock poised for 100%+ gains. No matter what Trump tweets next, these stocks dominate their industry niches – which means their cash flows and dividends will continue to skyrocket in the years ahead. Higher dividends mean higher share prices – which is why this strategy is the most sure-proof (and secure) way to earn 12% annually on your investment money forever.