Let’s say you’re looking to retire and want to bring in the average American salary in your golden years.

It’s a good goal—and more than enough cash for many retirees, especially if you live outside places like, say, San Francisco, where the average one-bedroom apartment rents for $3,300 a month (!)

So how much are we talking about here?

As of March 2017, the average US worker took home $896.60, according to the Bureau of Labor Statistics. Assuming 50 working weeks a year, that’s $44,830.

Okay, so we need to get $44,830 in pre-tax passive income. Where are we going to get it?

Most people look to three options: bonds, stocks and real estate. And sadly, that’s where many lose their shot at our $45k income stream.

Treasuries, Stocks Need Over $1M Just to Be “Average”

You’ll notice I’ve added one more column to the chart above, called “CEF Portfolio.” It clobbers US Treasuries, index funds (through which many investors buy stocks) and real estate, plus it gets us more than 99% of the way to our goal.

I’ll have more to say about CEFs in a moment—including the names of 9 of these funds boasting yields from 9.9% all the way up to 11.3%!

First, let me explain why the other three choices come up short.

Treasuries: A “Safe” Way to Get Meager Income

US Treasuries will require the biggest nest egg, simply because they have no chance of appreciating in value. With Treasuries, you’re effectively lending to the government and getting cash flow in exchange. The good news is this income is tax-free, so we need to earn less than we need to elsewhere because we won’t have a tax bill to deal with.

The bad news is that if we lock up our cash for 30 years (!) with no risk-free way of withdrawing that cash without potentially losing some of our principal, we need over $1.2 million invested to get $35,864 in post-tax income (which is pretty much what $44,830 would turn into for most Americans after tax). That’s because we’re only getting a 2.96% yield at today’s Treasury rates.

A millionaire can only get an average salary? We need to do better.

Index Funds: Retirement Roulette

Meager bond yields are why many people turn to index funds, which charge low fees and track the broader stock market. There are a couple problems here, the biggest being that market crashes can and do happen.

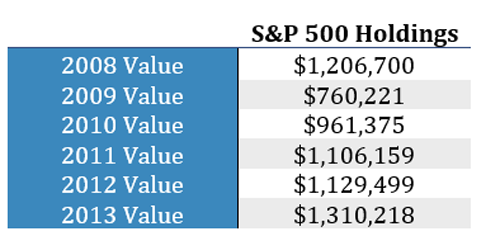

I examined the danger index funds can pose to retirees on April 4. But for now, let’s imagine you were going to retire at the start of 2008, and let’s assume you have our $1.2 million to invest in the Vanguard 500 Index Fund (VOO). Here’s what would have happened in the following years:

Index Funds Take the Brunt of a Downturn

That’s right—you would have been in the red for five whole years! Normally this isn’t that big of a deal … if you’re looking to keep your investment for a decade or more and not touch it. In fact, if you’re planning to invest more while you keep working, these dips are opportunities to buy.

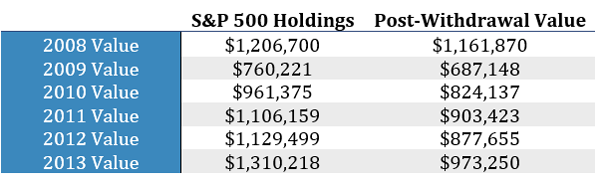

But that means nothing if you’re planning to retire and actually use your investments. For retirees, these market declines were absolutely devastating.

A Crushed Nest Egg

Because the retiree depends on market gains to keep the portfolio from going down AND to provide income in retirement, a downturn is doubly devastating.

To get around this, finance academics have studied historical market returns in the so-called Trinity study. According to that data, to get that $44,830 pre-tax income, we need to invest $1.2 million to guarantee that we won’t run out of money in retirement.

That’s almost identical to what we would need if we choose safer US Treasuries, so what’s the point of an index fund?

If you’re nearing retirement, not much. So let’s move on.

Real Estate—Far From “Set It and Forget It”

I know I don’t need to remind you of real estate’s role in the 2008–09 crisis. But even if we strip those years out, annualized pre-tax yields on real estate average about 5.5% per year, net of closing costs, mortgage costs, repair and maintenance, vacancies, real estate taxes and insurance. Of course, this return varies a lot depending on your local market, and it could be a lot lower.

Already, you can tell from that long list of associated costs that real estate investing isn’t really “passive.” Any landlord can tell you that building maintenance, nagging tenants for late rent checks and advertising and showing properties quickly add up to a lot of hours. Of course, you can outsource that work to a building-maintenance company, but their fees will drag down your returns.

The bottom line? So-called “passive” real estate may beat the S&P 500, but it comes with its own headaches.

Your Best Retirement Play Now

This is where CEFs come in.

CEF stands for closed-end fund, a little-known asset class that beats our other three options by a lot. In fact, I hold most of my personal net worth in CEFs and have been studying them for years.

I recommended 3 CEFs to buy for safe 8.2% yields on May 1. Today I’ll show you 9 that pay even more—with up to 11.3% dividends!

CEFs are like mutual funds or exchange-traded funds—they pool cash from investors and use those funds to buy investments. Many CEFs focus on one asset class, specializing in things like municipal bonds, real estate or blue chip dividend-paying stocks.

That diversity is one reason to love CEFs: you can combine a basket of them to create a well-diversified portfolio. But the main thing that makes them stand out is the income.

Due to their structure and use of managed payouts, where managers sell overpriced stocks and turn those gains into dividends, CEFs tend to yield a LOT more than real estate, stocks or government bonds. In fact, it’s not unusual to find CEFs paying 9% dividends.

With those kinds of payouts, we only need $500,000 to get $44,830 in annual pre-tax income.

Sound impossible? It isn’t. Let me show you 10 funds that have all achieved this feat on their own. And I’m choosing these funds at random; in reality there are a LOT more that yield over 9%, and many have even beaten the S&P 500 for years.

A Portfolio Bursting With Income

These funds are run by different firms and have different investment goals, so you could hold them all and get a lot of diversification.

The list includes the Western Asset Mortgage Defined Opportunity Fund (DMO), the Guggenheim Strategic Opportunities Fund (GOF) and the MFS Intermediate High Income Fund (CIF), which carry all sorts of bonds.

Then there’s the Clough Global Allocation Fund (GLO), which focuses on international investments.

On the energy front, we have the Nuveen Energy MLP Total Return Fund (JMF), and then four stock-focused funds: the Voya Global Equity Dividend and Premium Opportunity Fund (IGD); the Calamos Global Total Return Fund (CGO); the Gabelli Equity Trust (GAB); and the Eaton Vance Risk-Managed Diversified Equity Income Fund (ETJ).

If you had $500,000 and wanted to retire with $44,830 in income, these funds would do it for you. In fact, they’d do more; as you can see from the chart above, these funds all have yields far above 9%, so you can reinvest that excess income and compound your returns.

My Secret Strategy for FAST 32%+ Gains in CEFs

Now what if I told you I’ve found a dead-giveaway signal that a CEF is about to take off and hand you quick double-digit upside?

Sounds crazy, right?

But when this signal showed itself in May 2016, lucky investors jumped on it and rode one CEF to a 32% gain in just 11 months!

And you don’t even have to wait that long for this totally ignored trigger to send your CEF flying: when it showed up AGAIN on December 23, 2016, the folks who spotted this “profit bat signal” bought in and rode another fund to a 19.8% GAIN in a little less than four months!

Now, for a limited time, I’m going to show you EXACTLY what this amazing indicator is (you’ll kick yourself for not noticing it earlier!). Once you learn the secret, you only have to do three things to set yourself up for big profits:

- Wait for this indicator to go off.

- BUY!

- Pocket your 30%+ in gains and dividends!

When you add this stealth alert to the 7.6%, 9.9% and, yes, even 11.3% yields you routinely find in CEFs, you get what I call a perfect profit storm: high yields now and serious upside in the medium and long term!

You owe it to yourself to discover this secret and see how it can work for your portfolio. Simply CLICK HERE to get all the details now.