If 2022 taught us anything, it’s that we need to swing our portfolios away from this:

We’re Fading “Cardiac” Share-Price Action Like This …

That’s the chart of “America’s ticker”—the SPDR S&P 500 ETF Trust (SPY)—last year. I call SPY “America’s ticker” because it’s by far the most popular way to track the S&P 500.

But its popularity does not translate into safety. Just holding this simple index fund last year meant taking a 20% haircut—with plenty of heart palpitations along the way! That’s why we want to shift our portfolio returns toward the smooth and steady growth of dividends:

… And Toward the Serene Upward Drift of Dividend Growth

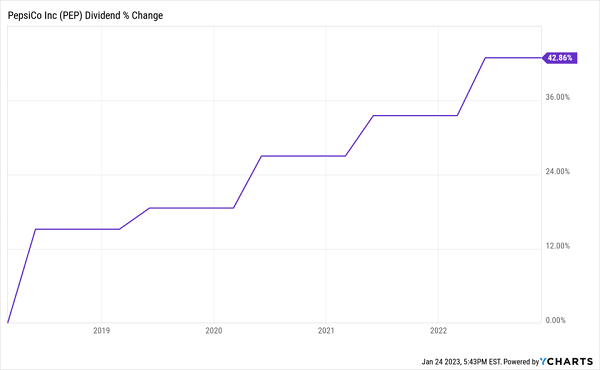

That’s more like it! What you’re looking at is the payout growth at PepsiCo (PEP), a stock many folks look to as a source of steady dividend payouts.

Dividends—and Buybacks—Set to Soar in 2023

The good news here is that it’s easy to shift more of your return to dividends: according to S&P Global Indices, S&P 500 payouts jumped 10% last year—despite the general market dumpster fire. And payouts are likely to keep climbing, even if we hit a recession in 2023.

That’s because, even though S&P 500 earnings are expected to be off this year (down 3.5% from 2022), S&P Global Indices says earnings could dip 5% and there would still be room to raise payouts.

I don’t expect profits to drop that far—but we’re not going after stocks like PepsiCo, for one simple reason: its meager dividend growth isn’t enough for us to bother logging into our brokerage accounts!

Here are three things we are going to look for in dividend growers we’re targeting this year:

- “Medium-sized” dividend yields—in, say, the 3% to 5% range—so we’ve got a decent payout now and a 7%+ yield on our original buy soon, thanks to …

- Accelerating dividend growth—I’m talking growth rates much faster than the S&P 500 average and PepsiCo’s token hikes.

- Finally, we like to see a healthy share buyback program—especially this year, as the 2022 selloff left many stocks trading on the cheap—an ideal time for buybacks to create real value. Clearly, corporate C-suites are getting the message: S&P Global Indices expects S&P 500 buybacks to pop 10% this year.

Bonus points if we can find stocks with high insider buying—because as I wrote in my January 17 article, insiders can sell their shares for any number of reasons, but they only buy for two: they expect the price to rise and they expect the dividend to rise—and bolster their own personal income streams!

Buying a stock with this heady mix can lead to serious gains indeed—especially in the wake of a pullback like the one we’ve just seen.

How Buybacks and Surging Payouts Sent Our “Popular” Buy Soaring

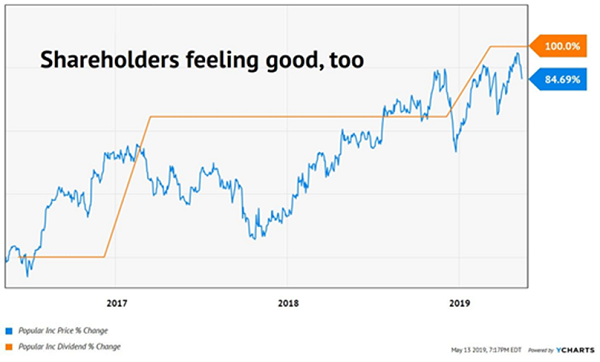

Here’s just one example of how these ingredients can “blend” to give share prices a big boost. Back in the spring of 2019, after the market had ended 2018 with a double-digit plunge (which, you may recall, came as the Fed was aggressively raising rates), I issued a buy call on Puerto Rico’s Popular (BPOP), the largest financial firm on the island, in my Hidden Yields dividend-growth advisory.

At the time, Popular was trading at book value (or the value of its physical assets). This meant we were getting its booming banking business for free!

And booming it was: Popular had been steadily building market share as foreign banks left the island, including Wells Fargo & Co. (WFC), which had just sold about $2 billion in auto loans to Popular. In all, Popular had a dominant 58% share of the island’s banking market.

Sure, the stock only yielded about 2.2% at the time, but its dividend growth was off the charts, with the payout having doubled in just the last three years. That had gotten the mainstream crowd’s attention, and they bid up the share price to match:

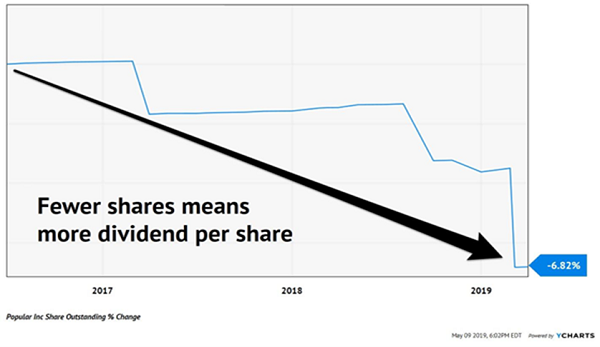

Share buybacks? Check. The bank had just dropped $250 million on its own stock. And over the preceding three years, it had taken 6.8% of its “float” off the market, too! That has a knock on effect on the company’s dividend payout because it’s left with fewer shares on which to pay out.

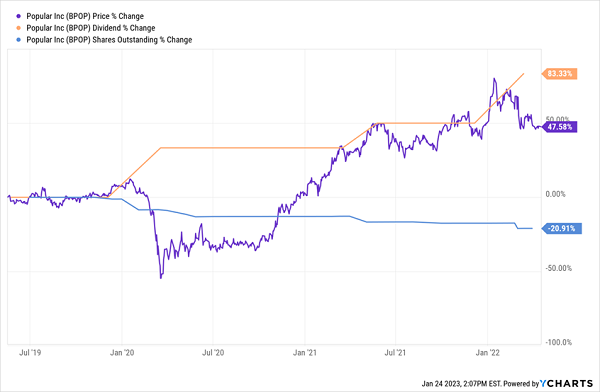

That was enough for us. We bought Popular for Hidden Yields in May 2019 and held it for just shy of three years, checking out in April 2022.

In that time, management juiced the dividend by an astounding 83%, doubling the yield on original buy to 4%. The bank also took 21% of its shares off the market. All together, these moves drove the stock price up 48%, for a total return of just over 61%:

Buybacks and Dividend Growth Powered Popular to a Fast Gain

Of course, none of this was visible by just looking at the 2.2% current yield, as many folks do. That’s why we need to dig deeper. And with dividends and buybacks likely to pick up this year, we’ll get plenty of opportunities to do so.

My Proven “Dividend Magnet” System Just Revealed Its Top 5 Buys for 2023

The “straw that stirs the drink” of this strategy is the “Dividend Magnet”—or the predictable pattern of surging payouts driving share prices higher.

Think about it: this is why the current yield on your favorite dividend stock never changes, even after a payout hike. Because investors spot the hike and bid the shares up—and the yield back down.

So, by carefully watching dividend growers and jumping when their hikes grow at an accelerating rate, you can set yourself up for some very nice profits indeed.

But this is tough to do on your own—you need to pore over corporate earnings reports to make sure that a company’s payout growth is backed by solid business growth.

Believe me, there are plenty of paupers out there, using debt or other financial engineering to raise dividends when they have no business doing so.

These are the companies you don’t want to own when the payout cut (inevitably) comes.

Let me show you how to dodge the dividend traps and zoom in on the next Populars, with healthy payout hikes poised to send their share prices soaring. Click here and I’ll share my full Dividend Magnet strategy. I’ll also reveal how to get my exclusive Special Report on the 5 “must buy” dividend growers right now.