A few weeks back, bond giant PIMCO trimmed a bunch of payouts from its closed-end funds (CEFs). Which was no bueno for income investors, who buy CEFs solely for their dividends.

We don’t own any PIMCO funds in our premium portfolios currently. But readers, who rightfully recognize me as a PIMCO fanboy, have written in to ask what’s up.

“Any thoughts on PIMCO recent slashing of dividends? Do you think they will also cut PDI’s dividend?”—John S

John, you know me well. Maybe too well! Here’s a live look at my nightstand which boasts a copy of The Bond King: How One Man Made a Market, Built an Empire, and Lost It All.

(I’m 128 pages in… and would enthusiastically recommend it to fellow fixed-income geeks.)

Bond nerd or not, most of us dividend investors do know the “Bond King” Bill Gross. He was Morningstar’s Fixed Income Manager of the Decade from 2000 to 2009. Gross netted 7.7% yearly returns for his investors—a big return from bonds.

Sure, Bill loaded the deck in his favor. He bought bonds that his benchmark “competitor” iShares Core US Aggregate Bond ETF couldn’t. Like higher-paying paper such as junk bonds, which boosted Gross’s returns and yields.

The New York Times once wrote that Gross was on the US Treasury’s “speed dial.” That’s a gross thought (sorry, had to) for us free market lovers.

But, for us profit-loving contrarians, I have another idea. Let’s hold our noses and invest alongside the guy who is so connected.

PIMCO gets the best bond deals. Could we get mad instead? Sure. Or we can invest alongside Bondland’s royalty.

That said, all kings are eventually deposed. Gross, of course, left his PIMCO throne years ago. A tide of cash followed him out the door.

But the flow of money quickly stopped when successor Dan Ivascyn stepped to the plate and began banging out bond doubles himself. (Hence Dan “Beast” Ivascyn, according to his work colleagues.)

No wonder PIMCO let the King walk out the door – they had a Beast in waiting!

A money manager of Ivascyn’s caliber will usually cost 2% annually (plus 20% of profits). And it’d take a million bucks or two to get his attention. Beasts don’t come cheap!

We contrarians, however, don’t pay up for talent. We are our own silent, calculating beasts. And as such, we simply bide our time and cherry pick the PIMCO funds when they “waive” their management fees.

This is what we did when we pounded the table on PIMCO’s Dynamic Credit and Mortgage Total Return Fund (PCI) back in May 2016. Unlike most PIMCO funds, which were trading at a premium to their net asset values (NAVs), PCI offered a 10% discount.

Which meant we were getting Ivascyn’s PCI fee “comped.” PCI was a CEF, and CEFs pay their management fees out of NAV. They tend to have higher fees than ETFs, which is fine—we simply wait and demand a discount when we buy.

A 10% discount “comps” any management fee. Plus, we still secure a sweet margin of safety!

At the time I called PCI a “financial rehab success story” because it was playing in Gross’s old sandbox. MBSs got a bad rep after the mortgage market imploded in 2007. But nine years later, those bonds were screaming deals thanks to previous fears.

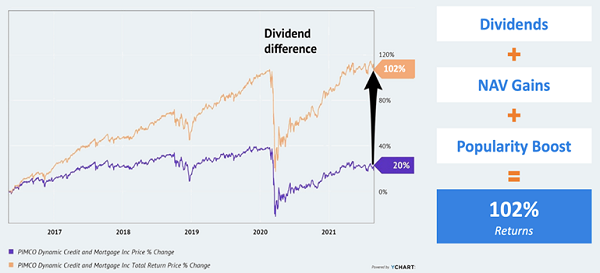

The dividends we collected from PCI made the difference. Our initial 10.8% annual yield added up. PCI’s payout hit our accounts every single month and in fewer than six years we were able to collect 70% of our original purchase price back in dividends:

Plus, the fund gained value while it was paying us! It was like an annuity, but better. Not only did we keep our capital, but it kept growing too. The result? A dividend double—102% total returns in less than six years (including payouts).

PCI’s “Dividend Double”

Alright Brett, you are no doubt thinking. If PCI is so great, why are you talking about the fund like a loving pet who passed away?

Well, in early 2022, PIMCO Dynamic Credit and Mortgage Fund (PCI) merged into sister fund PIMCO Dynamic Income Fund (PDI). On the surface, that was no problem—same great management team (the Beast) and generous dividend (13% as I write)!

But I had three problems with PDI by April 2022, which is why we sold. Pay attention because these problems persist today:

- The fund had swung to a 6% premium to NAV. Which meant our dollar in bonds were selling for $1.06. No longer a deal. (As I write, that premium is up to 12%!)

- Long-term interest rates were still rising, denting the value of the bond’s that PDI owned. Also bearish for its price. (Plus, I’m still not convinced the 10-year Treasury yield has peaked.)

- Short-term interest rates were also soaring, raising the cost of capital for PDI. This would weigh on the NAV and put the dividend at risk.

I’ll elaborate on number three, because this point is my biggest concern with many CEF dividends in the near-term, including PDI and other PIMCO funds.

PDI uses a lot of leverage—48% to be exact! This is great when rates are low. Borrow for 1%, earn (say) 7%, it’s a slam dunk.

But money is more expensive today, with short-term rates approaching 5%. Even now it still makes sense for PDI to use leverage—it’s just not as lucrative.

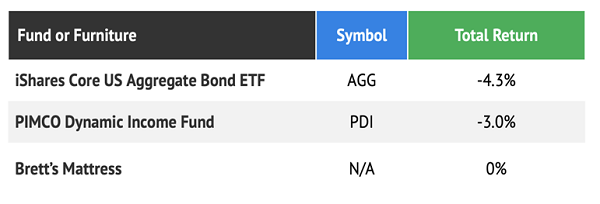

For this reason, PDI’s total return has lagged the cash under my mattress since April 2022 (when we sold it from our Contrarian Income Report portfolio):

I believe this is foreshadowing a potential dividend cut in 2023 for PDI. It’s cost of money has risen so much that something has got to give.

With a current yield of 13%, it probably won’t be a crushing cut. PDI will still pay something healthy. But I personally would prefer for us to wait for that moment—and to let long-term rates top out once and for all—before we consider re-adding PDI to our portfolio.

What would I recommend buying today? That’s easy—I’d look past PIMCO and PDI and would instead consider these 8%+ monthly dividend payers.