“This wine is crap.”

My wife (girlfriend at the time) glared back. I couldn’t let it go.

“Seriously…we paid $50 for this? I’d rather drink a bottle of Niagara.”

My comment—and ode to the New York wine that tastes like Welch’s grape juice—didn’t help the glare.

I was 22 years old, making $50K per year. It wasn’t a bad starting salary back in the day, but I didn’t have many extra $50s to spend on a Napa Valley wine tasting.

Plus, this guy had been drinking cheap Canadian beer since he was 16! The thought that I could procure 100 Labatt Blues for the price of our tasting raised my temperature further.

But our wine hostess saved me a trip to the boyfriend doghouse.

“Now, for the decanted version,” she quipped as she poured our next tastes.

“Wow!” I yelled. “This is much better!” (I’m sure she couldn’t wait to get rid of me and my empty wallet.)

“The decant was the difference?” I asked.

“Oh yes,” she assured. And paused for effect, before slipping into an arrogant tone that my (later) wife and I would repeat for years to come.

“Mr. Peju always decants his wines.”

We left Peju Winery that day with an important life lesson. Give the wine time to breathe (or, if short on time, speed the process with a decanter).

We should apply the same lesson to the dividend stocks we buy. Larry B. reminded me of this when he wrote in, asking why his “stop loss” keeps getting tripped up:

How much of a stop loss do you recommend? I have been stopped out of so many of your recommendations.

You recommended New Residential Investment (NRZ)… It was a couple of days before I could buy, and by then NRZ had dropped to 10. I bought some, then placed a stop at $9.50. But then, very soon, the price fell below $9.50 and I was stopped out.

Larry, my man, take a deep breath. And consider letting your dividend stocks live a little, too.

NRZ has bounced higher and lower after we added it to our Contrarian Income Report portfolio last July. Larry’s stop, unfortunately, was ticked briefly and this “whipsawed” him out of a perfectly good dividend position.

Remember, we’re here for the dividend. We’ve already collected $0.50 in payouts and, fundamentally, NRZ looks great.

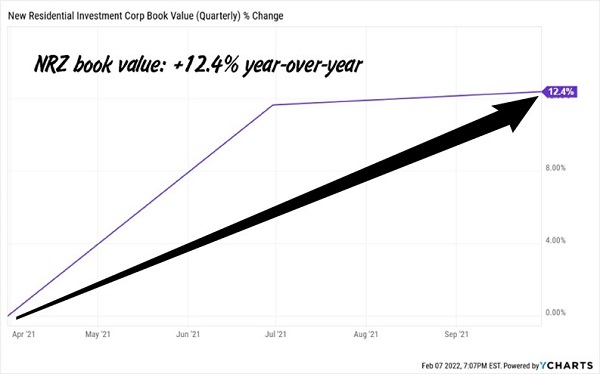

Its book value, which is reported quarterly and less prone to whipsaws, has gained more than 12% year-over-year. This supports the main reason why we bought NRZ in the first place—we knew its underlying portfolio would benefit as mortgage rates rose.

NRZ owns a boatload of mortgage service rights (MSRs). These rise in value when refinancing activity slows, which is exactly what is unfolding as long rates move higher.

As the 10-year Treasury climbs higher, mortgage rates are likewise hitching a ride. They have quietly spiked, and are now at their highest since Summer 2019.

NRZ’s book value—the dollar amount its portfolio would fetch on the open market—has climbed a sweet 12.4% over the past year:

NRZ’s Book Value Increases with Interest Rates

The stock is a bargain, trading for just 90% of book value. We’re happy to collect its 9.7% dividend while we wait for price appreciation.

So, let’s not place the stop loss for NRZ too close. In fact, I’m not sure a leash on the stock price itself is the right move anyway. Why don’t we simply watch mortgage rates? As long as they move flat to higher, we are buyers of NRZ. And if they reverse course, we’ll sell—and beat Wall Street to the trigger.

Larry also noted he is a Hidden Yields subscriber. So I want to pull one more example from our dividend growth publication, to show an example of us using a long-term trend change to book profits.

We added Canadian Pacific (CP) to our HY portfolio in April 2020, a very opportune time to buy a cheap railroad. We quickly enjoyed fast gains.

But how did we know when it was time to book profits?

Well, it’s part art and part science. We saw CP pay up—perhaps too much—to acquire Kansas City Southern. This was a fundamental concern.

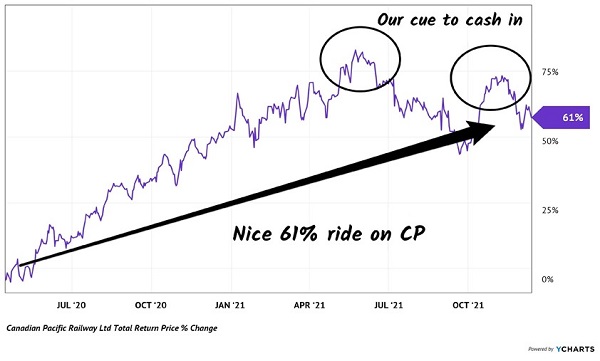

This was reflected in the long-term chart. CP put in a “lower high” and we took that as our cue to cash in profits:

Why We Sold CP in HY for 61% Profits

We didn’t sell at the exact top, but we caught the bulk of the move higher. This winner, who we let run for many months, began to slow down.

Plus, the 2022 edition of the stock market was looking destined to be a big hot mess. So why overstay our ride on CP? With a bearish backdrop and a big-picture breakdown, it made sense to take the money.

(We thought the Federal Reserve was going to be our 2022 problem. Instead, a dictator using a playbook out of the 1930s invaded a neighboring sovereign nation in the name of a land grab. But I digress…back to stop losses.)

Our “big-picture stop” on CP kept us aboard for 20 months. We made some nice profits and hopped off the train before it went off the tracks in 2022.

Markets are volatile right now, to say the least. Let’s make sure we consider the long-term trends of our holdings. That’s a better bet than placing a percentage-based stop, and getting whipsawed out of an otherwise-good dividend payer.

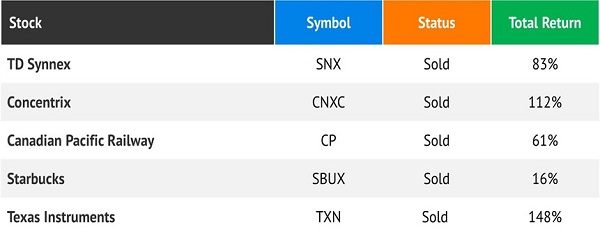

If you’re not a current HY subscriber, why not? CP was only one of five big winners we recently cashed in.

Recent HY Profit Taking

We’re now sitting on the proceeds, waiting out the current pullback and getting ready to go dividend shopping. The Great Reset—and dividend growers that will directly benefit—have my attention right now.

This is an economic trend that is going to power our next set of total returns. I’m talking 61%, 112% and even 148% like we saw above. Please click here to profit from the greatest economic event in American history.