Dividend stocks reward us with more than just cash flow. They actually benefit our retirement portfolios in four ways:

- A high current yield—for meaningful cash flow today. In a moment we’ll spotlight a timely play with a neat 3.5% yield.

- Dividend growth, which tends to pull a company’s share price higher (as we’ll see below with this stock, whose payout exploded 450% in the last decade).

- Share buybacks, which cut the number of shares outstanding, boosting earnings per share and share prices in the process. And of course …

- Price appreciation, as the stock moves up on strong results for the company, its industry or the economy as a whole.

This gives us a big advantage over the “buy and hopers” who pick up the typical S&P 500 stock and are mostly left to rely solely on #4 above.

Trouble is, looking at each of these in isolation can give you a misleading picture: a high yield, for example, can be caused by a plunge in the share price as much as it can a series of dividend hikes.

Dividend growth is great, but you’re still behind the 8-ball if the current yield is too low, or if your company hikes at a snail’s pace, such as the penny-a-year increases AT&T (T) was famous for before the recently deposed Dividend Aristocrat cut its payout!

And buybacks, of course, can burn shareholder value if they’re done when a stock is expensive.

Luckily for us, there’s one single metric that takes all of these things into account, giving us a true picture of exactly what we’re getting from a dividend stock before we buy. It’s a powerful tool called shareholder yield. Hang with me for a second and we’ll run through how it works.

This Electronics Retailer Boasts a Huge 17% Shareholder Yield

Let’s start by diving into Best Buy (BBY), which dominates “brick and mortar” electronics retailing and has an underrated online presence, which was second only to Amazon.com (AMZN) in 2020, according to Statista. The gizmo peddler even outsold Apple (AAPL)!

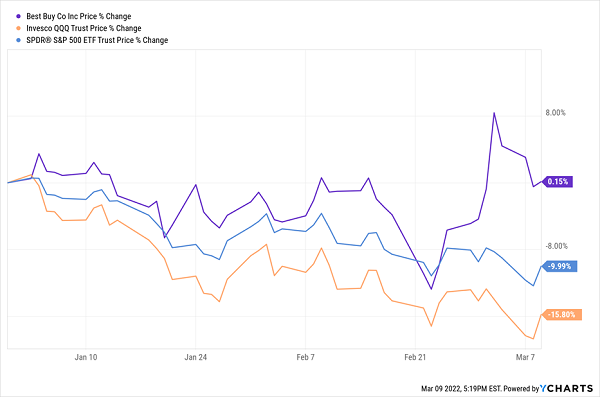

What’s more, Best Buy (in purple below), unlike the plunging S&P 500 (in blue) and the tech-heavy NASDAQ (in orange), has moved sideways this year, finding support around the $90 mark, making it appealing at current levels:

Best Buy Shakes Off the Crash

That’s partly because investors flock to Best Buy in all market weather—helping stabilize the stock in a crash and sending it soaring in bull markets—because its management has a long history of treating shareholders well, as we’ll see now.

Let’s start with the first part of Best Buy’s shareholder-yield story: the dividend, which yields 3.5% currently. That’s not bad on its own: it’s nearly triple the 1.3% the S&P 500 pays! And things get better from there.

… Add a Hit of Payout Growth …

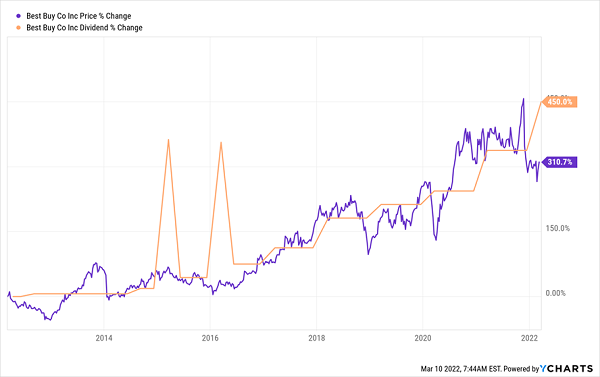

When you add in Best Buy’s payout growth, the real magic begins. The company hiked its dividend an astonishing 450% in the last 10 years, while floating investors a couple of nice special payouts, as well.

As you can see in the chart below, the company’s rising dividend has acted like a magnet on its share price, pulling it higher with every increase. What’s more, its payout growth has accelerated in recent years:

Best Buy’s “Dividend Magnet” Pulls Up Its Price

This means if you’d bought a decade ago, your yield on cost—or the payout you’d be getting on your original buy—would have jumped to an amazing 13.8%!

I expect buyers who pick up the stock today to be looking at something similar in a decade’s time. And we still have one more chapter of our shareholder-yield story to cover: share buybacks.

… and Ignite Your Returns With Share Buybacks

One of the most underrated things about Best Buy’s C-suite is that it knows how to time a buyback: check out how they’ve upped their repurchases (thereby decreasing the number of shares outstanding) as the stock has gotten cheaper (going by its P/E ratio) in the last five years:

Best Buy Smartly Bargain Hunts Its Own Stock

To bring this full circle, when you combine Best Buy’s buybacks in the 12 months ended January 29, 2022, with its dividend payouts in that time (including a 27% hike announced last March), you get its shareholder yield.

That comes out to an amazing 17.9%! And the shareholder yield on a buy made today will only grow as buybacks and dividend growth continue. (Note that Best Buy just announced another big dividend hike on March 2, after its latest quarter ended, to the tune of 26%!)

How to Calculate Shareholder Yield

The formula for figuring out a company’s shareholder yield is simple: take the amount spent on share repurchases in the preceding 12 months, deduct any cash brought in through share issuances, then add in the total spent on dividends.

You then take that sum and divide by the company’s market cap, or the value of all its outstanding shares.

In Best Buy’s case, that comes out to $3.5 billion spent on share repurchases and $688 million spent on dividends, for a total of $4.189 billion in total shareholder returns in the past year. With a $24.5-billion market cap, we can say Best Buy sports a monster 17.1% shareholder yield.

Beware Shareholder-Yield “Traps” Like T. Rowe Price

Of course, a high shareholder yield is great, but we still need to stay on the right side of today’s investment trends. Which brings me to T. Rowe Price Group (TROW), an investment manager with about $1.6 trillion in assets under management.

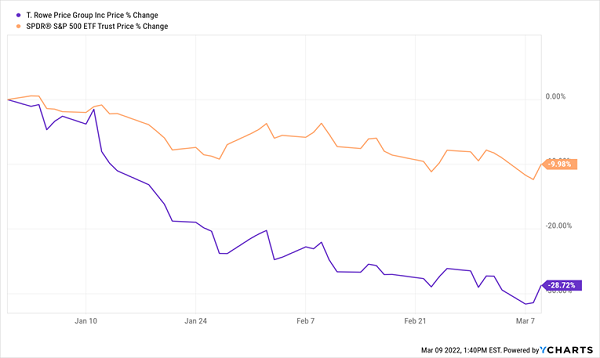

This stock’s taken a drubbing in the markets this year and is down about 30%—almost triple the decline of the S&P 500! That’s more than triple the stock’s shareholder yield of 8.9%, too.

Price’s Plunging Stock Devours Its Shareholder Yield

Price is a great company with a long institutional memory, having been founded back in 1937. It also boosted its assets under management by 19% as of the end of the fourth quarter from a year before.

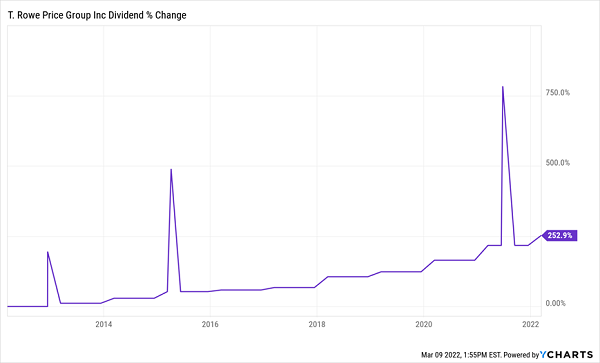

Management has done everything right on the shareholder-return front, too: Price is a Dividend Aristocrat, having hiked its payout for 35 straight years, including 252% in hikes (plus three special dividends) in the last 10 years alone.

Price’s Payout Growth Builds Up Its Yield

But most of this took place in a bull market, and asset managers like these tend to act like leveraged plays on stocks as a whole, which multiplies their losses when things get rough. That’s unlike Best Buy, which can exploit its strong brand and customer loyalty in all market weather (not to mention the fact that electronics have become more embedded in our lives than ever).

All of this makes Price a great company to put on our watch list until calmer markets return. For now, Best Buy, with its high shareholder yield and just-announced 26% payout hike, is the better choice.

7 More “Shareholder Yield” Superstars With Fast Payout Growth Ahead

Stocks like Best Buy are true diamonds in the rough because their high yields, fast payout growth and buybacks attract investors in all markets.

As we just saw with Best Buy, that relentless investor interest helps throw a floor under the stock in rough markets and propels it to new highs when markets soar!

But as rare as stocks like these are, they’re not impossible to find: I’ve uncovered 7 more just like Best Buy, with fast-growing dividends, smart buybacks and high current yields.

The time to buy them is now. Click here and I’ll give you full details: names, tickers, yields, a complete analysis of management—everything you need to know.