Is the bottom in?

Or is the market merely “sniffing glue” (as one of my friendly financial advisors aptly put it to me)?

No matter where you are currently handicapping the market, we have a proven playbook for buying big payers after a crash like the one we’ve just seen. We’ll consider the winners coming out of the 2008 crash, as well as the types of stocks that have performed well in post-pandemic China. Let’s get right into it.

Post-Crash Tip #1: Think Big

I love small companies. I lasted exactly 13 months in corporate America before fleeing to the world of small business and startups. As you know, I’m not a guy who can tolerate much red tape.

Well, I have to admit, these are the times to invest in the big bureaucracies. Size and scale help when the world closes itself for business.

On the other side of this, we are (sadly) going to lose many small businesses. Large companies are going to gain more market share. We, as consumers, will be worse off for a while.

But this doesn’t mean our portfolios should be worse off for a while. When it comes to post-pandemic investing, it is going to pay for us to pay more attention to the big firms.

Of course, within the big firms, we are likewise going to have winners and losers. To sort them out, we are going to modify our order to go “lite on the assets.”

Post-Crash Tip #2: Think “Asset-Lite”

As I was planning my corporate escape, 22-year-old me looked around and saw friends and peers in the San Francisco Bay Area making more money and having more fun. Most of them worked in “tech,” specifically software, a wonderful type of business that enjoys big profit margins when done right.

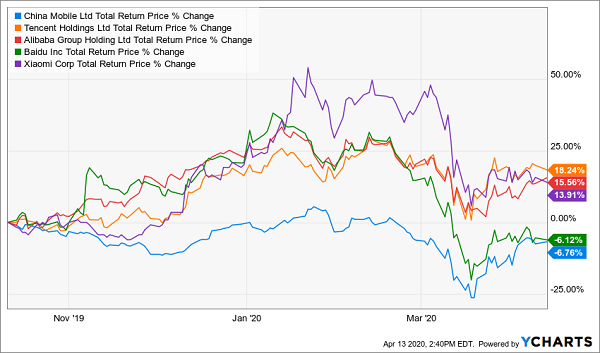

Here’s a 6-month look at China’s five largest software companies. They’ve averaged 7% returns over this pandemic-included time period, performing much better than many of their “asset-heavy” peers:

China’s Asset Lite Menu: +7% Through Pandemic

Let’s apply the same thinking and look at US-based insurance companies. Their people and their processes are their product, similar to software firms. But they tend to return more cash to shareholders and do not subject us to “buying” shares and “hoping” they’ll appreciate post-crash.

For example, Allstate (ALL), the huge insurer that’s a household name, hasn’t been this much of a bargain since 2014. It trades for just over 7-times free cash flow (FCF).

If you bought shares six years ago, the last time they were this cheap, you doubled your money (+103%, including dividends). And this even includes its 2020 pullback!

This is the beauty of investing after a waterfall selloff, in which every stock on the exchange was crushed. Allstate’s shares are quite cheap with respect to their dividend:

Shareholders Are in Good Hands

This is exactly the type of “blue-light special” that we should be adding to our portfolios right now.

For you folks focused on current yields, Allstate probably still doesn’t pay enough. It’s dishing 2.2% at the moment, about as much as it ever does. To boost our income, we need to consider shares with cash flow projections that have been unfairly dinged by investors. Give us low-priced stocks with secure dividends!

Post-Crash Tip #3: Think Contrarian

It’s a fine line we contrarians walk as we sort through the market’s immense trash heap. Buying a stock simply because it’s “way down” is not enough of a filter for quality. We should focus on dividend-paying shares that have been:

- Crushed with the market’s cascade selloff yet have

- Income streams that are safe (or, at least, should be able to “muddle through”).

Healthcare landlord and old favorite of ours Medical Properties Trust (MPW) comes to mind. It may not be asset lite, but it sure owns the asset-of-the-moment: hospitals.

Unfortunately for most REITs, April 2020 is probably going in the books as the worst month for rent collection in the history of this asset vehicle. Founder Edward Aldag notes that even usually-steady hospital cash flows are a bit uncertain at the moment. Hospitals are prioritizing COVID-19 patients and deferring non-critical procedures, which is the right thing to do from a human standpoint but creates potential gaps in cash flow.

My sense is that Ed and his excellent MPW team will eventually find a way to the other side. If and when they do, today’s 6.2% yield on shares will look like a good buy. However, given the volatility in these markets and the fact that we have an interesting earnings season on tap (to say the least!), we should bide some time to wait for a great opportunity on MPW.

Urgent: 7 “Hidden Yield” Stocks Kicking Off Mega-Rallies

As intriguing as ALL and MPW look, I’ve got 7 overlooked dividend growth stocks that are already starting to kick off mega-rallies.

Thanks to the March waterfall crash, these share prices have temporarily “disconnected” from their safe, rising payouts. Simply put, these stocks are way too cheap!

And while these seven “recession-proof” names have already begun to move, ain’t seen nothing yet. These stocks are ready to pack on consistent gains for years to come (whether the broader market continues its rally, or regresses).

Recession-proof dividend investing is the name of the game right now, and these 7 stocks are set up for fast gains regardless of what the S&P 500 does.