Andrew, Arthur and Paul knew their REIT stock was too cheap. So, last August 21, the trio slapped down three independent bets on their firm’s stock using their own money. Their reward? Quick 26% returns:

REIT Moguls Know Best, for Quick 26% Gains

Did they time the entire sector bottoming? No – Vanguard’s Real Estate ETF (VNQ) dropped 5% over the same time period. But that was just noise, because these boys knew their own business. They cherry picked the bargain.

It shouldn’t be a surprise that a chief financial officer (CFO) and his cronies would nail this trade. After all, finding deals with real estate investment trusts (REIT) is a straightforward 2-step process:

- Find a high relative yield, and

- Buy it if “first-level worries” will soon prove fleeting.

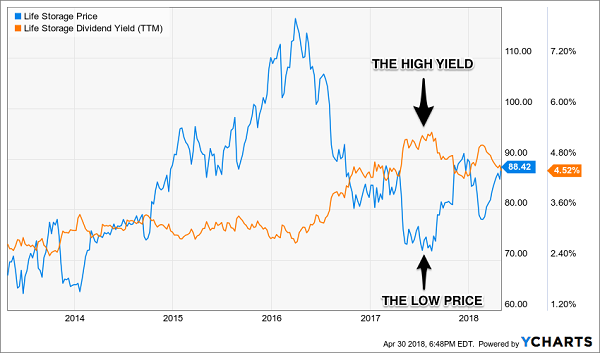

The executive trio at Life Storage (LSI) realized that Wall Street was concerned about oversaturation in self-storage. But they also knew their own company’s properties even better. So they took advantage of LSI’s highest yield in six years and locked in a 5%+ yield with instant upside:

Buy the Bargain (When Yield is High)

Have REITs Bottomed? If So, Consider These Smart Money Favorites

REITs at-large may be quietly carving out a bottom. They didn’t seem to mind the 10-year Treasury bond passing its feared (but arbitrary) 3% threshold. This might be a sign that all of the “bad rate news” is already priced into shares.

The best REITs will be just fine anyway as rates rise, because they’ll be able to keep raising their rents. Higher cash flows will translate to higher dividends and higher stock prices.

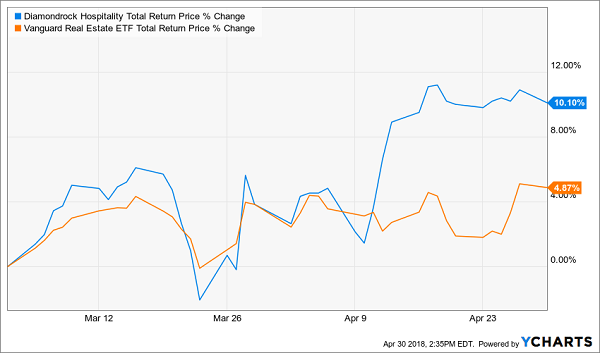

And that’s where you and I should focus, regardless of what the widely followed REIT indexes do. VNQ is up 5% in the last two months, but it’s been doubled up by the favorite of another REIT mogul, Mark Brugger:

Diamondrock Doubles Up the Index<

Mark called it. The Co-Founder, President and Chief Executive Officer at DiamondRock Hospitality Company (DRH) didn’t worry much about the 10-year. He bought his own 5% yield, and banked 10%+ total returns (including dividends) in just two months.

And these tidy gains add up when you’re a baller like Mark. His $99,800 purchase has already appreciated to $110,500!

Stephen’s 6% Gravy Train

Meanwhile Director Stephen Sadove’s timing couldn’t have been worse. Good thing he knew exactly what to buy, too.

Investors who followed his lead last August and purchased the “dumb” index VNQ (rather than Stephen’s stock) have seen their capital grind 6% lower. But this guru wasn’t worried about the “REIT rout.” His 6% buy did just fine, returning him a neat 15% in less than nine months. Rather than buying the sector at large, he put his money into the company he knew best – Park Hotels & Resorts (PK):

The REIT Director Outsmarts the Index

Park is a relatively new real estate investment trust that was spun off by Hilton Worldwide (HLT) at the beginning of 2017. Recently it was trading for less than 10 times its funds from operations (FFO) – a bargain that was bought by this smart money insider.

Which REIT Will Rally Next?

Many subscribers write in to ask me what I think of REITs right now. As you can see, this question is too broad to be profitable.

It doesn’t matter what happens with prices in the broader sector. From real estate in general to REITs themselves, no matter what the headline narrative is, there is a bull market in some REIT, somewhere.

Which means our job is to find it – and bank these big yields with price upside while we get paid.

Next up, I’ve got my eye on Nashville. The city is booming, and its Predators are looking for a return to the Stanley Cup. Our beat here is payouts, and Music City’s popular export Opry City Stage is poised to power some big rent demands.

The attraction’s creator and landlord is Nashville-based Ryman Hospitality Properties (RHP). The firm recently opened Opry City Stage in popular Times Square, with an eye towards more venues in more tourist-centric locations (both at home and abroad).

Will it work? CEO Colin Reed seems to think so. He’s so confident that he purchased another cool $500,000 in his own firm’s stock two weeks ago, bringing his total position above $50 million!

I love it when the big boss owns more than 10% of his own firm. Plus, his stock’s even a bit cheaper today than it was when he added to his position a couple of weeks back. As the global bull market in country music continues to unfold, Colin’s dividends might be a boot scootin’ way to fund your retirement.

In fact, there’s only one thing I don’t like about Colin’s purchase – his stock only pays 4.3%! Which means that his fat half-million dollar purchase pays a miserly $21,500 in yearly dividends. That isn’t nearly enough passive income.

Fortunately there are other bargains paying nearly twice as much as Ryman that are great buys today. Plus, they’re recession and rate proof!

My 2 Favorite Recession & Rate Proof REITs: 7.5%+ Yields and 25% Upside

My two favorite REITs today are comfortably positioned in recession-proof industries. They’ll have no problem continuing to raise their rents – and reward their shareholders – no matter what the Fed decides at its next meeting, what Trump tweets or when the stock market finally takes a breather.

My favorite commercial real estate lender lets us play Monopoly from the convenience of our brokerage accounts. They do all the legwork, building a secure, diversified loan portfolio featuring offices, retail space, hotels and multifamily units.

Management then collects the monthly payments, deposits the checks–and then it sends most of the profits our way as dividends (a requirement of its REIT status).

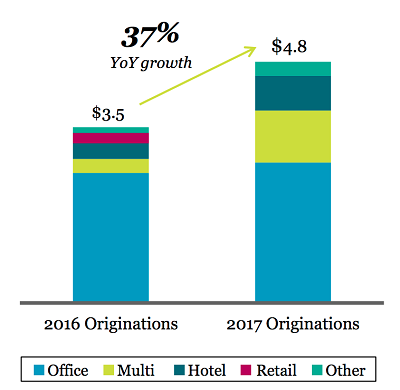

The stock’s current dividend (a 7.7% yield today) is covered by earnings-per-share (EPS) today. And don’t be fooled by the stagnant dividend (not that stability is bad). The firm continues to originate an increasing number of loans:

37% Loan Growth Today Tees Up Dividend Growth Tomorrow

This firm is a conservative lender with perfect loan performance (100%). Its growing portfolio will drive higher profits, which in turn will inspire the next dividend hike. The best time to buy the stock is right now, as it makes the investments which will drive its payout and share price higher from here.

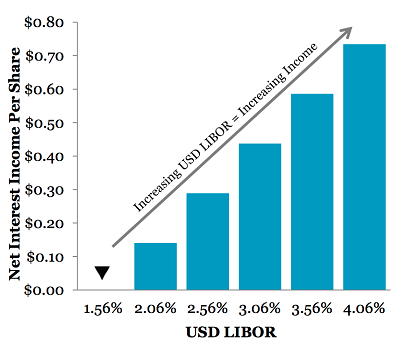

Plus this firm has also smartly eliminated interest rate risk because it uses floating rates. In fact, it’s actually set up to make more money as interest rates move higher:

More Income as Interest Rates Rise

Same for another REIT favorite of mine, a 7.5% payer backed by an unstoppable demographic trend that will deliver growing dividends for the next 30 years. Interest rates are no problem for this landlord because it will simply continue raising the rents on its “must have” facilities.

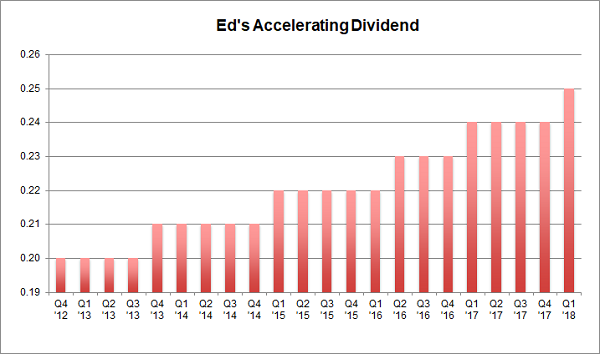

Its founder Ed admitted that, fourteen years ago, he had “zero assets, a dream, and a business plan.”

Well his dream and plan were plenty – the visionary entrepreneur parlayed them into $6.7+ billion in assets!

And right now is the best time yet to “bet on Ed” because his growing base of assets is generating higher and higher cash flows, powering an accelerating dividend:

I love dividend increases because they are proof that management is actually making more money, so can afford to pay us shareholders more. And an accelerating payout is a flat out cry for help!

Any management team that raises its dividend faster and faster is clearly making more money than it knows what to do with. This usually happens when it achieves a tipping point where its machine no longer requires as much reinvestment to continue growing. So leadership says: “Please, take a bigger raise, shareholders.”

Meanwhile investors and money managers who spot dividend accelerators lose their minds because, in theory, there is no valuation too high for a company that is increasing its dividend at an accelerating rate. Their spreadsheets literally break, and they buy the stock in a frenzy.

Ed’s stock should be owned by any serious dividend investor for three simple reasons:

- It’s recession-proof.

- It yields a fat (and secure) 7.5%.

- Its dividend increases are actually accelerating.

These two REITs are both “best buys” in my 8% No Withdrawal Portfolio – an 8% dividend paying portfolio that lets retirees live on secure payouts alone. And they can even enjoy price upside to boot, thanks to the bargain prices they’re buying at. Now, as active recommendations for my premium subscribers, it wouldn’t be fair to reveal their names here.

But I would like to send you a free copy of my latest special report, Recession Proof REITs: 2 Plays With 7.5%+ Yields and 25% Upside, with all the details.

It includes the names, tickers and exact buy advice on how to start profiting right now.

In short, it’s everything you need to know before you invest a single penny, and it’s yours at no cost whatsoever. Click here and I’ll share how you can get a complimentary copy of my premium REIT research.