I know I don’t have to tell you it’s tough (and very frustrating) trying to get any kind of income stream from your savings these days.

The average S&P 500 stock yields just 1.9%. That’s not even enough to cover inflation!

Treasuries? The 10-year note yields an almost equally pathetic 2.3%.

But there are still safe 7%+ dividends to be had—even in the “income desert” we’re living in now. I’ll show you three funds yielding up to 8.5% (more than 4 times the typical S&P 500 yield) in a second.

Dividends like those can let you clock out on a nest egg that’s far smaller than advisers say you need. I’m talking $550K—and maybe less. Here are two simple strategies for pulling it off:

- Go contrarian: Buy safe, 7%+-paying funds when they’re out of favor (I’ll give you a simple way to determine this shortly) and hold them through any market.

- “No Withdrawal”: We’ll build a portfolio that can let you retire on dividends alone. Because when you’re pulling in, say, a 7.5% average yield, you can generate a $40,000 income stream on just a $550K nest egg.

For many folks, that’s enough to punch out, collect their dividend checks and ignore the market’s daily swings altogether!

Better yet, I’ve done the work for you.

Here are three overlooked funds yielding up to 8.5%. All three are what I call “pullback proof”: they hold the line during corrections like the “May massacre” we just saw.

High-Yield Pick No. 1: A “Preferred” 7% Dividend Paid Monthly

My first fund holds preferred shares, which are a perfect substitute for the “common” shares you probably own today.

A company’s preferred stock usually pays a much higher dividend than the “common” shares most folks buy. So by simply “trading in” your common shares for preferreds, you can double (or more) your income stream while still investing in the same company.

The tradeoff is usually less upside, but if you buy your preferreds through a well-run closed-end fund (CEF) —which I recommend—the cash return from your dividends can be so high you might not even notice.

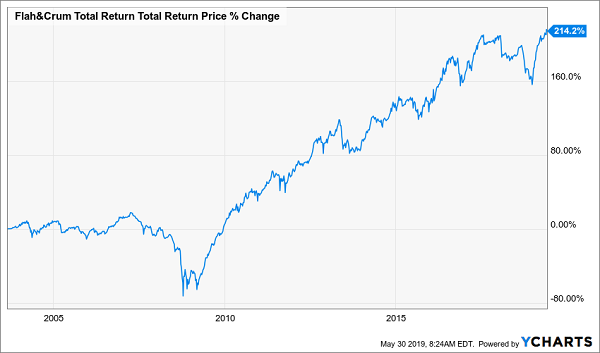

Consider the Flaherty & Crumrine Total Return Fund (FLC) (payer of a monthly 7% dividend): it’s delivered a 214% total return (including dividends) since inception in 2003, driven by its huge cash payouts:

A Huge Gain—Mostly in Cash

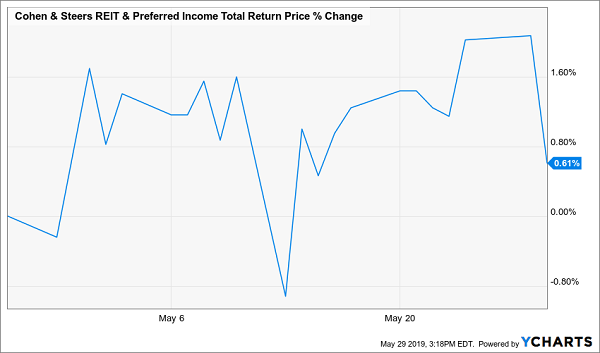

And talk about pullback proof! Look at how it performed over the past month:

The Ultimate “Pullback-Proof” Play

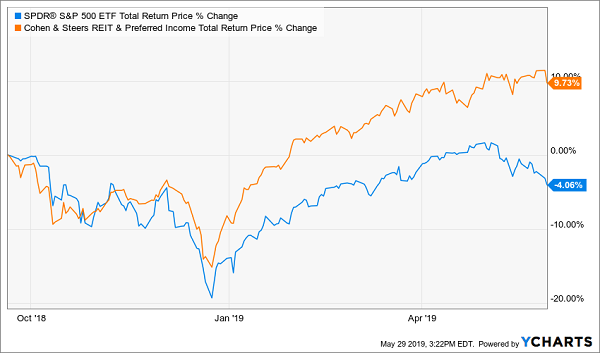

And check out the total return FLC has posted since September 20, 2018, when last year’s collapse started.

FLC Shows Its Mettle

As you can see, the fund’s return didn’t drop nearly as far as the S&P 500 in the meltdown, and shareholders are actually up 10% since that correction started.

Finally, let’s talk upside.

With CEFs, the key number to watch is the gap between the fund’s market price and the value of the assets in its portfolio, known as the net asset value, or NAV.

As I write this, FLC’s discount stands at 4%, and it’s traded at narrower discounts (and even hefty premiums) over the last five years, so we can look forward to price gains as that discount creeps ever closer to par—and beyond.

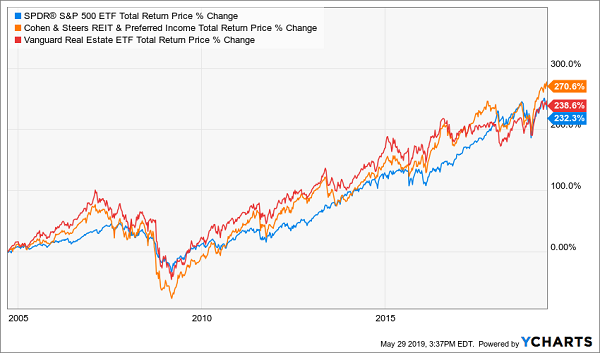

High-Yield Play No. 2: A Top REIT Fund Yielding 7.1%

If your portfolio is low on preferreds and real estate investment trusts, you can grab both in one buy with the Cohen & Steers REIT & Preferred Income Fund (RNP).

RNP has crushed both the S&P 500 and the REIT benchmark Vanguard REIT ETF (VNQ) since inception in 2004—no mean feat for an income play like this.

A High-Yield Market Beater

And thanks to its huge dividend (current yield: 7.1%), a huge slice of that gain was in cash.

This fund taps its REIT holdings (51% of the portfolio) and preferred stocks (49%) to give us that steady 7.1% dividend (also paid monthly). And as with FLC, RNP has held up nicely this past month:

RNP Sails Through the “May Massacre” …

Also like FLC, it fell far less than the market during last fall’s correction, and bounced back faster, handing investors a nice 10% return.

… And the Fall Collapse, Too

Finally, you can grab this one at an 8.5% discount to NAV, a discount that can’t last, considering RNP’s “no-drama” approach and long history of crushing the S&P 500.

High-Yield Play No. 3: An 8.5% Dividend With Upside

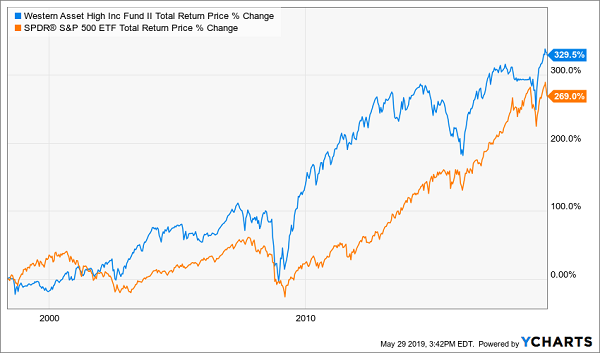

The Western Asset High Income Fund II (HIX) is a high-yield bond fund with a long history of strong performance, having tripled in value (including dividends) since its IPO in the late 1990s, crushing the S&P 500.

This Fund Can’t Stop Climbing

HIX gives investors that strong return while yielding 8.5%. Management firm Legg Mason, which has been in the fixed-income business for 48 years, generates HIX’s 8.5% dividend through a portfolio that includes emerging-market bonds, high-yield corporate bonds, investment-grade corporates, bank loans and a small cash holding.

That high total return and consistent share-price performance make HIX worth your attention at any time, but now that it’s trading at a 9% discount to NAV, it’s particularly compelling.

That’s because the fund has traded near (or even above) par with its NAV for months on end in the past. So if you buy HIX now and wait for its discount to evaporate, you’d be looking at 9.9% gains on top of your 8.5% dividend stream.

5 More “Pullback-Proof” Plays Yielding Up to 9.6%

These three funds are just the start. And to tell you the truth, they’re not even my favorite “pullback-proof” buys now.

Those would be the 5 stocks in my just-released “Pullback-Proof” retirement portfolio, including one stock—a conservative lender with stellar loan performance—paying a “hidden” 9.6% dividend.

I say this stock’s dividend is hidden because its current yield—the one you’d see on Google Finance and Yahoo Finance—clocks in at 8.1%. That’s already massive, but the current yields on most screeners don’t account for one critical thing:

Special dividends.

And this REIT has a long history of special payouts. Check it out:

An 8.1% Dividend—and More

Add in this company’s last special payout, and its “real” yield pops to that incredible 9.6% I just mentioned.

Here’s what that payout means in dollars and cents: if you had $100K in this cash machine, you’d get $9,600 back in dividend cash in the past year alone—and I expect a similar total payout this year (this REIT usually rolls out its special dividend in the fall).

And when I say this stout dividend is “pullback-proof,” I mean it: check out how this stock performed in 2018—a year most investors would rather forget:

My Pick Soars in a Rough Year

That’s right: when the rest of the market tumbled, this pick’s owners actually bagged a near-14% return!

I’m ready to share the name of this pick and my 4 other top “Pullback-Proof” buys with you now.

These 5 reliable CEFs are similar to the 3 funds I showed you above, but with two critical differences: they’re set for stronger price upside (7% to 15% in the next year alone) and faster payout growth, too!

And you’re about to get the full story on each of them.