I hear it from readers all the time: closed-end fund fees are just too high!

And when you can get a passive fund that simply tracks the S&P 500, like the Vanguard 500 ETF (VOO), for a microscopic 0.05% expense ratio, it can seem silly to pay over 2% for a closed-end fund.

(If you’re unfamiliar with CEFs, click here to learn more about them—and why you need to hold at least a few of these high-yield investments in your retirement portfolio.)

My answer is that you need to look closely at total returns, keeping in mind that CEFs report returns after fees. That’s because the fees are taken out of the CEF’s net asset value (or NAV—the total market value of the fund’s portfolio, including stocks, bonds and cash) before management hands over dividends and capital gains to shareholders.

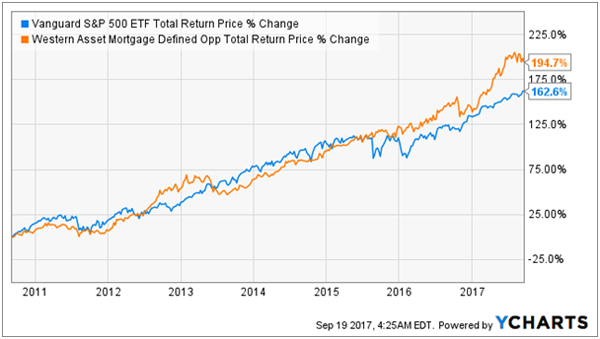

You also need to keep a keen eye on the fund’s total performance. Many funds crush VOO, even with their much higher fees. Take, for instance, the Western Asset Mortgage Defined Opportunity Fund (DMO), which has returned an impressive 15.5% per year in capital gains and dividends, helping it clobber VOO ever since its IPO:

Performance Worth Paying For

Consider also that this outperformance happened during one of the strongest bull markets in stock market history—and at a time when hedge funds famously underperformed the market. It’s a perfect illustration of how choosing the right fund makes a big difference!

Of course, many investors are still concerned that big fees will eat into their gains, so they hunt for a fund that charges low fees while still paying a high dividend yield and setting them up for long-term outperformance. That’s a tall order, as the funds with the biggest dividends often charge higher fees. But it’s not impossible.

Take another Western Asset fund—the High Yield Defined Opportunity Fund (HYI).

This fund has a 0.91% expense ratio, making it one of the lowest-cost actively managed bond funds out there. Currently yielding 7.4%, HYI offers an impressive income stream while also trading at a hefty 8.5% discount to NAV.

That means you’re getting $1.00 of assets for just $0.815. And a discount that wide is one of the most reliable predictors of big upside there is.

HYI is also one of the few CEFs that hasn’t seen its discount get smaller over the last few months.

Cheap Fees and a Bargain, Too

Another bond fund with even lower expenses comes from Invesco, which takes a paltry 0.54% annual fee from the portfolio of their simply named Invesco Bond Fund (VBF).

VBF has a relatively low dividend yield for a CEF, at just 4.3%, but it’s also been a strong performer over a long period of time. In the last 10 years, it’s handed 7.5% annual returns to shareholders, but what’s really impressive is the fund’s longevity. Since the 1970s, VBF has returned over 1,000% in gains and dividends!

A Low-Fee Fund That Won’t Keep You Up at Night

This is a great fund to buy, hold and pass on to the grandkids; its durability through all kinds of markets and its ability to keep delivering positive returns make it the kind of steady fund that’s hard to come by in uncertain times like these.

Oh, and you’re getting VBF’s assets at a 4.9% discount to NAV, so it’s a bargain, too.

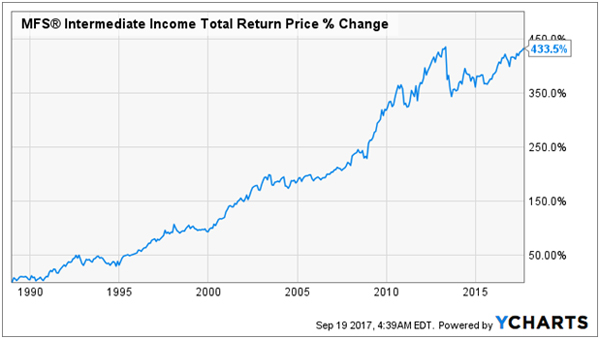

Now let’s offset VBF’s relatively lower dividend with something that’s a much stronger payer. The MFS Intermediate Income Fund (MIN) has a 0.62% expense ratio that’s dirt cheap considering its 9% dividend yield. MIN also trades at a 4.9% discount to NAV, making this a bargain buy right now, as well.

Also, like VBF, this fund has a long history and a well-established track record of delivering strong returns. MIN is up over 400% since it launched in 1988 and has survived recessions throughout the ’80s, ’90s and, of course, the Great Recession of 2007–09.

Reliable Returns for 29 Years and Counting

With a massive 9% dividend payout, you could put $100,000 in this fund and get $750 per month in passive income. Compare that to just $163.33 per month from $100k in VOO and you can see the appeal of MIN, even if its expenses are a bit higher.

These 4 Funds Earn Their Keep AND Pay 7.4% Dividends

I just recommended 4 off-the-radar CEFs whose fees are all over 1%—but you won’t care a wit because they’re ready to explode for 20% gains in the next 12 months!

And yes, that BIG payoff is after fees.

How do I know?

Because each of these 4 funds is trading way below its net asset value—and as I mentioned above, that’s the most reliable indicator of big CEF gains there is.

And when discounts get this big, you only have one job: BUY. Then sit back as the share price takes off into the stratosphere.

You won’t even have to wait 12 months, because all 4 of these funds pay rock-solid 7.4% dividend yields now (and yes, those yields are also net of fees). So even if these 4 hidden gems simply trade sideways, you’re still set up for more than 7% CASH gains here.

I’m ready to give you my complete research on these 4 low-key funds. All you have to do is CLICK HERE to get their names, tickers and all the profitable details now.