Return to the office? Heck, we income investors don’t need to return to work—period.

We can turn our nest egg into a cash flow machine, with big dividends to cover our monthly expenses. I’m talking about retiring on dividends alone.

Yes, we’re three buys away from kicking back, collecting payouts and watching our portfolios continue to tick higher. Best of all these dividends have upside, which will power our nest egg to new highs. They serve as the “payout magnets” that pull our investments higher with each dividend raise.

Most importantly, this “three-click” portfolio is well diversified, with 560 different income investments. These secure payouts will provide us with plenty of cushion, even if we do see another pullback later this year.

A “Dividends Only” Retirement Is Entirely Within Reach

Despite what most naysayer advisors will tell you, there are many ways to pull off a “dividends only” retirement—my Contrarian Income Report service is built around the idea, actually.

Here are three types of funds that can get you there. Think of them as a blueprint you can tailor based on your age and income needs (we’ll get into specific tickers for each in a moment).

- Inflation-busting closed-end funds (CEFs) with monster yields—enough to get you a strong income stream on a reasonable upfront investment. (The CEFs we’ll talk about below are perfect foils for inflation—the boogeyman everyone is worried about now.)

- Corporate-bond funds to diversify your portfolio and set you up for gains as volatile markets push more investors to look beyond stocks.

- Overlooked dividend-growth funds, which grow your income stream over time and boost the value of your investment, as prices and dividend hikes are tightly linked, as we’ll see in a bit.

A Growing Trend

Before we go further, you should know that if you’ve chosen to pack it in early, you’re not alone: a recent survey from MetLife (MET) revealed that more than 10% of baby boomers have retired early over the last year and a half or so.

If you follow this route, of course, you’ll need your money to last longer than you may have originally planned. And the key to that is to shift your returns away from fickle share-price gains and toward a steady stream of dividends. Let’s do that with a three-fund “mini-portfolio” built on the assets we mentioned off the top.

As I said above, this trio holds a combined 560 investments. They come from across the economy, and they nicely spread your funds between stocks and bonds, too.

Even so, you’ll want to rotate a portfolio like this over time as conditions, such as today’s soaring inflation, change. I’ll give you my latest recommendations on when and how to do that in Contrarian Income Report (see below to get a risk-free trial to the service).

Retirement Fund #1: ClearBridge MLP and Midstream Fund (CEM)

Let’s start with one of the biggest dividends in the energy business—a monster 7.1% payout—which we can grab through the ClearBridge MLP and Midstream Fund (CEM). This CEF holds master limited partnerships (MLPs)—companies that mainly own oil and gas pipelines and storage tanks.

Giants in the pipeline business, like Enterprise Products Partners (EPD), Williams Cos. (WMB) and Energy Transfer LP (ET) dominate the fund’s portfolio.

These companies pay us high dividends because most MLPs are pass-through entities that don’t pay taxes at the corporate level. (By the way, you’ve probably heard that MLPs issue complex K-1 forms for reporting your dividends at tax time, and it’s true—they do. But buying through CEM gets you around that; the fund sends you a simple Form 1099 instead.)

That’s part of the story behind CEM’s 7.1% payout. The other is rising demand for energy, combined with production that’s still catching up following pandemic restrictions. That’s resulting in higher oil and gas prices—and distributable cash flow (DCF, a critical metric for MLPs) that’s largely recovered from the crisis, helping stabilize their payouts—and set them up for hikes.

In the second quarter, for example, Enterprise Products Partners saw its natural gas pipeline volumes bounce back to 2019 levels; the MLP generated distributable cash flow (a critical metric for MLPs) that was also up from last year and allowed it to easily pay its dividend, with a DCF coverage ratio of 1.6.

And as oil and gas prices and volumes rise, they’ll continue to fuel MLPs’ cash flow and share prices, making them, and CEM, nice hedges against inflation.

The other great thing about CEFs is there’s one number that tells us if they’re expensive or cheap: the discount to NAV (net asset value, or the value of the stocks in the fund’s portfolio). As I write this, CEM boasts a 12% discount, but that discount was much smaller than it is now—around 7%—just before the pandemic hit, so we’ve got plenty of built-in upside here.

Now let’s talk performance:

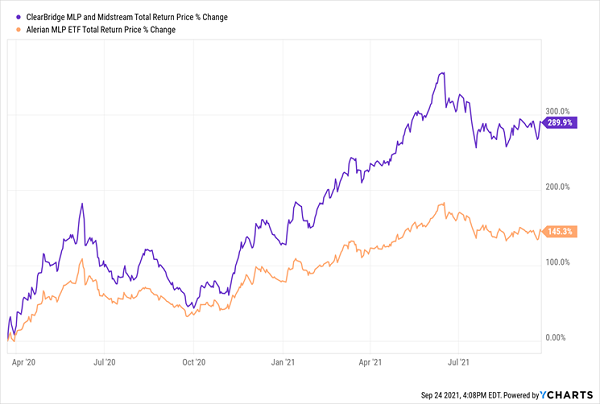

CEM’s Managers Crush Their Benchmark

As you can see above, the expert management team at ClearBridge has helped push CEM well past the MLP benchmark, the Alerian MLP ETF (AMLP), on a total-NAV-return basis (so based on CEM’s portfolio performance alone) over the last year. It’s not even close!

Even so, we can still grab this one for 88 cents on the dollar. That setup—a strong gain and a big discount—sets up a very reassuring entry point for income investors like us.

Retirement Fund #2: BlackRock Floating Rate Income Strategies Fund (FRA)

The Fed made it clear last week that it’s shifting into taper mode, and the 10-year Treasury rate shot from 1.3% to 1.47% in response, as expectations of a hike in the federal funds rate (essentially 0% now) picked up. We want nothing to do with the 10-year, of course, because a million bucks in Treasuries locks you in at a pathetic $14,700 in income!

And Treasury yields move higher, you’ll be stuck with your bond, as no one will want to buy it when they can grab newer ones paying 2%, 2.5% and more.

The BlackRock Floating Rate Income Strategies Fund (FRA) doesn’t have this problem. It buys floating-rate debt, which has variable coupons that are calculated quarterly or even monthly.

The best deals in the corporate-bond market are actually just below the somewhat arbitrary investment grade cutoff. It’s where contrarian fund managers and investors like us capitalize on the fact that any pension funds, banks and insurance companies are not allowed to invest in these “low quality” issues per their bylaws.

The result is a sweet spot of value, thanks to the lack of big money chasing these types of bonds. And because this market is just a little off the beaten track, we want the top pros to work it for us. That’s exactly what we get from BlackRock, the world’s biggest management firm, with $7 trillion of assets.

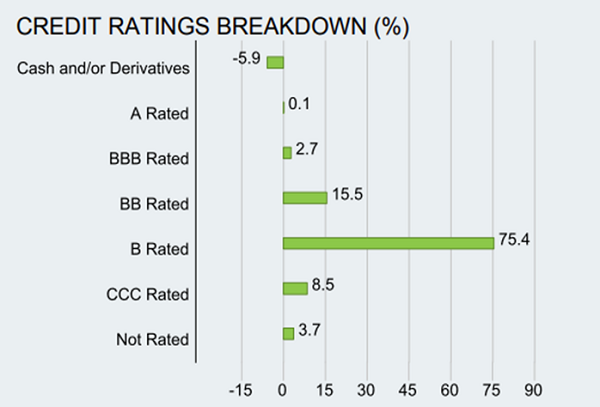

FRA’s managers, David Delbos, Mitchell S. Garfin, Carly Wilson and Abigail Apistolas, take advantage of the absence of big buyers in these debt pools to secure a yield to maturity of 6.4%. They love the Bs—they’ve got 90% of the portfolio in BBB, BB or B rated debt, which is the sweet spot, at or below the investment-grade cutoff of BBB.

Source: BlackRock.com

And now, with pressure to raise the federal funds rate just starting to build, we’ve got a compelling buy window on FRA, before the rest of the mainstream crowd catches on. This is why we’re looking to FRA even though it “only” pays 6% (which is a touch low side for a CEF); it’s bound to make up for that in price gains.

We get a nice assist here from FRA’s 5% discount, too, which will propel its share price higher as it evaporates in the coming months.

Retirement Fund #3: ProShares Russell 2000 Dividend Growers ETF (SMDV)

Finally, let’s supplement our two 6%+ payers with SMDV, an ETF focused on smaller firms with fast-rising dividends. Going with a fund like SMDV is a savvy move because a rising payout is the No. 1 driver of share prices.

I know that may sound odd, as most people see dividends and price gains as different kinds of returns, but you can see this in action in the shares of Lakeland Financial (LKFN), one of SMDV’s top holdings. In the past five years, Lakeland has boosted its payout 79%—and the price has marched up along with it:

Lakeland’s Dividend Powers Its Share Price

Same story with HR and admin services provider Insperity (NSP), another SMDV holding, which has even tossed in a big special dividend for good measure:

Dividend Up, Share Price Up

Sure, SMDV’s current yield doesn’t get our hearts racing, at 2.2%. But its payout growth will inflate the yield on a buy made today. Plus you’ll be lined up for payout-powered gains, as well. There’s simply no better inflation hedge than that!

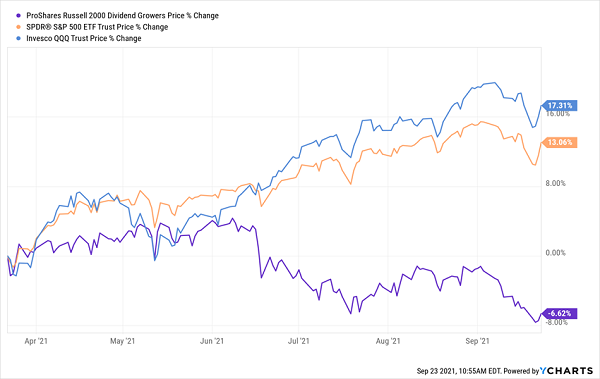

Why small caps, you ask? Because, while the S&P 500 and NASDAQ break out to new highs (seemingly) daily, small caps, as represented by the Russell 2000 Index, have been left behind in the last six months:

Still Plenty of Value in Small Caps

It’s only a matter of time before these smaller, growth-oriented firms close that gap, implying fast 19% price upside for us as we move into SMDV. We’ll tap its portfolio for a nice growing income stream while we wait for that to happen.

The Best Retirement Plan: a $17,000 Yearly Returns on Every $100K Invested

My exclusive “7% No-Withdrawal Retirement Portfolio” gives you fatter payouts and even more diversification than the three funds above. This pack of stout retirement plays includes top-quality preferred shares, real estate investment trusts (REITs) and blue-chip stocks (beyond energy firms), too.

That sets this portfolio up to cut through whatever the market throws at us in the next couple months, while it pays us rich dividends all the way up to 7.7%.

In addition to their huge dividends, the stocks and funds inside this elite portfolio trade at such deep discounts that I’m forecasting 10%+ yearly upside, to go along with the massive (and monthly!) dividends on offer here.

Convert those forecast gains and dividends into dollars and cents and you’re looking at $7,000 in dividends and $10,000 in price upside for every $100K invested!

I’m ready to give you instant access to this life-changing retirement-income portfolio now, plus that 60-day trial to Contrarian Income Report I mentioned earlier. CIR keeps you up to date on my recommendations, so you can be sure your “dividends only” portfolio is always tuned to ever-changing market conditions.

Simply go here and I’ll give you full details on the stocks and funds in this portfolio, and you can start your 60-day trial subscription to Contrarian Income Report, too. In just a couple clicks, you’ll have everything you need for a dividend-powered retirement! Don’t miss this rare opportunity.