If we can say one thing about the rest of 2024, it’s this: We’re looking at a stock-picker’s year here—and folks who try to play it with vanilla ETFs will have a tough time.

Just look at the state of play in front of us.

The Fed is trying to thread a needle, and if economic numbers come in too hot or too cold for Goldilocks, well, good luck holding something like the SPDR S&P 500 ETF Trust (SPY)!

In an environment like this, a good plan is to zig when the market zags.

To do so, we’re targeting stocks in the bargain bin with “recession-resistant” strengths such as steady revenue from clients who must buy their services no matter what.

At the top of our list? Utilities—specifically growth utilities that are riding the wave toward the electrification of, well, pretty well everything.

How will we find the best ones?

Easy, we’ll look at their dividend growth, and specifically zero in on companies whose payout growth is accelerating.

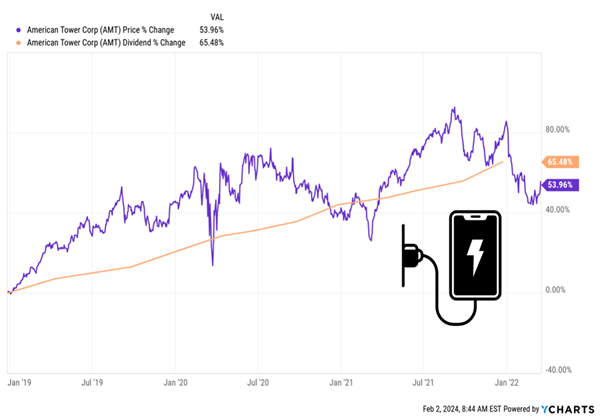

Because the truth is, dividend growth and share-price growth are joined at the hip: Where the dividend leads, the share price follows. Just like it did with our purchase of cell-tower REIT (a utility in everything but name) American Tower (AMT) in my Hidden Yields advisory in November 2018.

By the time we sold in March 2022, we’d booked a 57% return (in gains and dividends), as the dividend marched the price higher, point for point.

AMT’s “Dividend Magnet” Charges Up

(This, by the way, is why the yield on your favorite dividend stocks never seems to change: management hikes the payout, boosting the yield; then investors see that higher yield and bid the stock up—and the yield back down.)

Let’s move on to two other “growth utilities” whose dividends are on a tear. Both are also showing a unique signal that proves they’re bargains—and now is a good time to pick them up.

In addition to receiving steady, recurring revenue, both are expanding their operations, which will drive their profits (and dividends!) higher in the coming years.

“Growth Utility” Pick No. 1: Entergy (ETR)

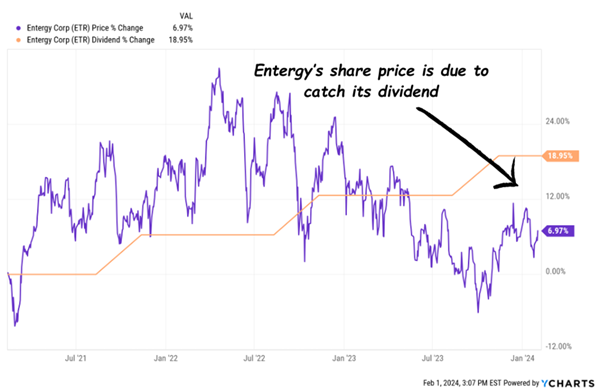

Let’s start with ETR, which serves three million customers in the South, namely Arkansas, Mississippi, Louisiana and Texas. The stock stands out because ETR’s dividend growth has kicked up a gear since early 2021.

Prior to that, management had been dropping middling two-cent-a-year hikes on investors. But starting with the 2021 hike, the size of its increases tripled.

That boosted the stock for a bit. But it’s since fallen behind, with the price now trailing the payout’s growth spurt. That marks a good buy window, before the price catches back up:

Entergy’s “Dividend Gap” Is a Good Buy Indicator

We can expect that payout growth to continue, by the way. For one, the dividend accounts for 63% of the company’s last 12 months of earnings, easily manageable for a utility with steady revenue like Entergy. Better still, the company “starts us off” with a high current yield of 4.4%.

Factor in ongoing payout growth and we can expect to be grabbing north of 5% in cash on a buy made today before long. That’s on the strength of Entergy’s forecast EPS growth of 6% to 7% in the coming years, as the South attracts more factories, thanks in part to favorable tax rates and the ongoing “onshoring” trend.

Source: Entergy 58th Edison Electrical Institute Financial Conference

Moreover, Entergy’s industrial clients continue to electrify their operations, which is a particularly potent demand driver when you consider that about half of the firm’s customers are industrial users.

To top it off, Entergy trades at just 14.6-times its last 12 months of earnings, well below its five-year average of 18. Cheap!

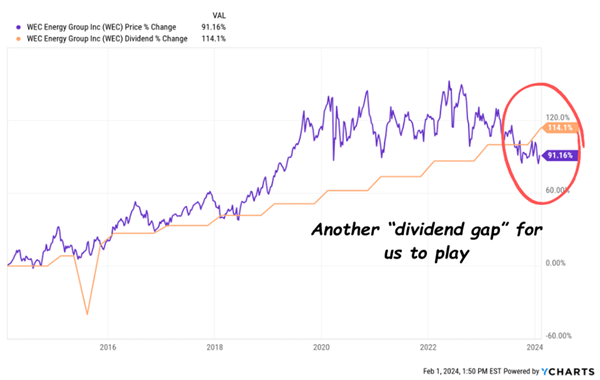

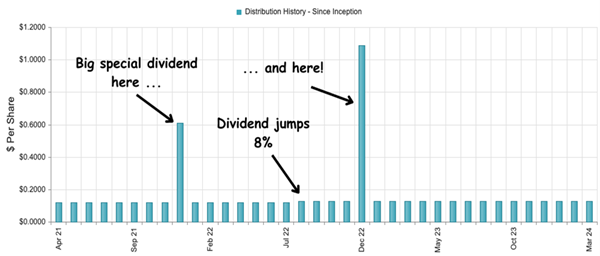

“Growth Utility” Pick No. 2: WEC Energy (WEC)

Meanwhile, far to the north is WEC, which serves 4.6 million power and gas customers in Wisconsin, Illinois, Michigan and Minnesota. Like Entergy, it gives us a high yield to start: 4.1% as I write this.

Dividend growth? Check!

On January 18, management declared a 7% hike to the payout, marking WEC’s 21st straight year of hikes. Meantime, the company’s earnings report, released last week, showed earnings per share up 37.5% from a year ago on an adjusted basis, to $1.10, meeting analysts’ estimates.

That’s despite the fact that 2023 got off to a warm start, hurting natural gas use. This actually bodes well for the current quarter, however, as it’ll provide a lower-than-normal figure for which to compare this year’s mild winter.

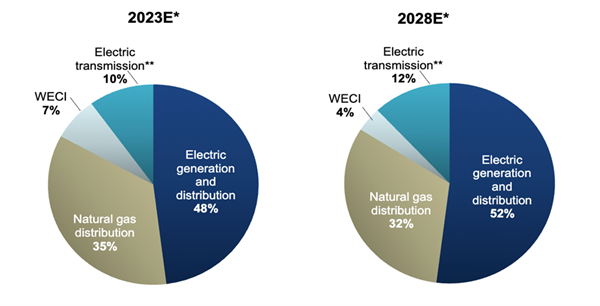

Meantime, the company is cutting its reliance on natural gas and fossil-fuel generation. WEC plans to build 3,800 megawatts of zero-emission facilities, including solar, wind and new battery-storage operations, between 2024 and 2028. That’s a smart move as the cost of renewable-power generation falls: according to the International Energy Agency (IEA), 96% of newly installed solar and onshore wind facilities generated power more cheaply than new coal and gas plants would have in 2023.

WEC’s Changing Energy Mix

Source: WEC Energy January 2024 investor presentation

Meantime, the latest dividend hike will add to a payout that has more than doubled in the past decade:

WEC’s Price Springs Higher With Its Payout

(Don’t worry about that dip in 2015—the payout was pro-rated due to WEC’s acquisition of Integrys Energy; it wasn’t cut!)

You can see that WEC’s share price (in purple) hardly ever falls behind its payout growth (in orange). And when it does, it doesn’t stay there for long. That makes today’s gap unusual—and worth looking at for some “bonus” upside before the purple line jumps over the orange one again.

Meantime, the annualized payout amounts to 64% of the $4.90, on average, analysts see the firm making in 2024. That’s more than sustainable for a growing utility like WEC—and it’s below the low end of management’s 65% to 75% target.

Finally, like Entergy, WEC is a bargain valuation-wise, too, with a P/E of 18.9, well below the five-year average of 23.2.

Buy This Top 2024 Pick Now—and “Lock In” a 14% Gain—in Cash!

WEC and Entergy are terrific stocks to own, especially with the uncertain economy we’re facing today. But we can get a lot more of our dividend income upfront, with a current yield that dwarfs the roughly 4% these stocks pay.

Enter another stock (closed-end fund, to be precise), that I’m pounding the table on as we move further into 2024. This underappreciated bond fund gives us the best of all worlds, with a 14% current yield, a monthly dividend, dividend growth and a history of special dividends!

A “Once-in-a-Generation” 14% Dividend Opportunity

Source: CEF Connect

What’s more, that immense payout is delivered by a manager whom Morningstar previously named Fixed Income Manager of the Year. He’s also been inducted into the Fixed Income Analysts Society Hall of Fame.

To say he knows the bond world is an understatement—and now we can get him working for us, just in time to help us navigate the shifting winds we’ll no doubt encounter in the year ahead.

Don’t miss this opportunity, which I’m urging ALL investors to take advantage of now. Click here to learn more about this 14%-yielding income play and get a free Special Report revealing my latest research on it.