Let’s ride this “tariff tiff” to a cash stream that’s double (and maybe even triple) the 2% and 3% payouts your friends are likely “grinding it out” with today.

I’m talking about a stout 5% yield here. And that’s just the start, because that payout has surged 64% in the last 10 years, and is set to repeat that feat in the next 10.

While we’re at it, we’ll “2008-proof” your portfolio, too, carefully cushioning your nest egg from the next market collapse.

And we’ll do all of this with the three unusual “pullback-proof” stocks I’ll show you shortly. Each is set to hold its own in the next crash, then soar when the dust settles.

How to Win From the Tariff Terror

These three high-yielders are all real estate investment trusts (REITs), often-overlooked “landlords” with properties ranging from apartments to warehouses.

REITs are perfect for times like these because they tend to move independently of the market, giving your portfolio much-needed ballast. Check out how REITs have performed since the “tariff tantrum” began:

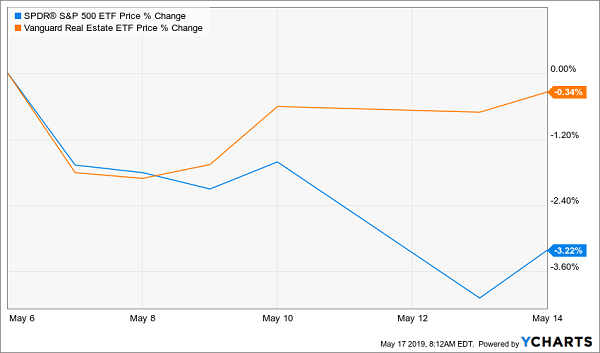

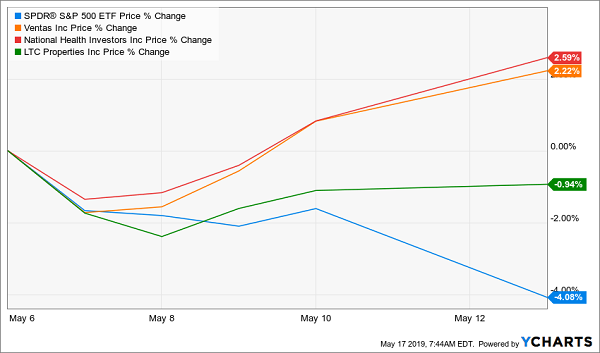

Stocks Tank, REITs Shrug

As you can see, REITs have traded flat since May 6—the first trading day after President Trump said he’d hit China with tariffs—through May 14, the day after the market’s 600-point swoon.

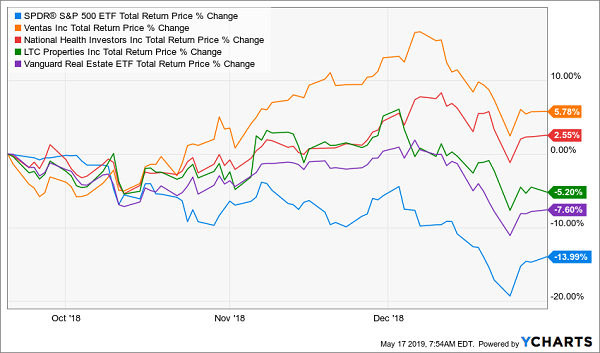

But let’s not stop there: we’ll verify REITs’ crash resistance by going back further—to the late-2018 market smashup:

REITs Fall Less Than the Market …

As you can see, REITs plunged less than half as much as the S&P 500. That’s thanks in part to their dividends (included in the chart above), which act as a cushion, giving us our return in cash, not vulnerable paper gains.

What happened next? REITs went on to crush stocks once 2019 dawned:

… And Roar Back Faster

Here are two other reasons why REITs are still great contrarian buys now:

- They must pay high dividends by law: REITs don’t pay corporate taxes, so long as they pay out at least 90% of their income to investors as dividends. That’s a big reason why the benchmark Vanguard REIT ETF (VNQ) yields 3.9%, more than double the 1.8% S&P 500 average.

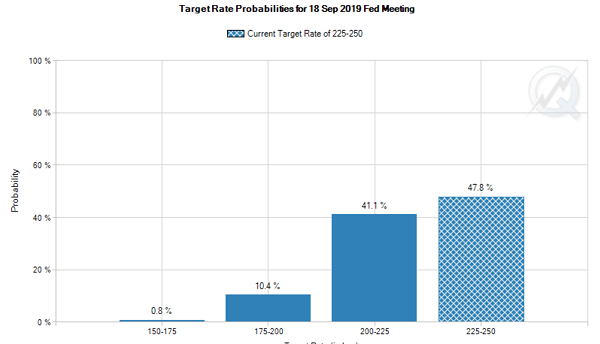

- The Fed will ignite REITs: First-level investors think rising interest rates are bad for REITs because they make so-called “safe” investments, like CDs and Treasuries, more appealing. But the rate-hike script has flipped: the market now sees the Fed cutting rates later this year:

Source: CME Group

But the first-level crowd is clueless! When they (finally) realize a cut is in the cards, they’ll pile in, giving REITs another lift.

So what’s the best way to buy in before REITs make another move up?

We’re going to skip “one-click” index funds like VNQ and look for REITs that have been (unfairly) left behind in the 2019 market run-up. That leads me straight to the one sector (and three REITs) I want to show you today.

3 Bargain “Tariff-Proof” REITs Yielding 5%+

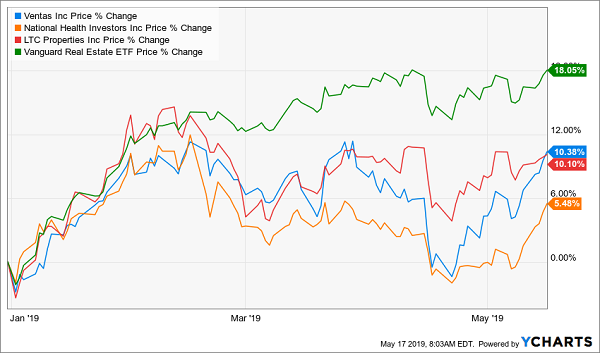

The sector would be healthcare, and our three “pullback-proof” REITs are: Ventas (VTR)—which I spotlighted last week—National Healthcare Investors (NHI) and LTC Properties (LTC).

As you can see, all three have trailed VNQ this year, handing us an opportunity to buy at a relative bargain (more on that shortly):

Healthcare Lag Gives Us Our In

Right off the bat, we’ve also added “China insurance” to our portfolio, because these three REITs, which own or invest in medical offices, senior-care homes, hospitals and labs across the US, have zero exposure to China.

Their gains and dividends are driven by one unstoppable megatrend: surging US healthcare spending—which the Centers for Medicare and Medicaid says will rise an average 5.5% yearly from 2018 to 2027, when it will hit $6 trillion.

No trade war will change that.

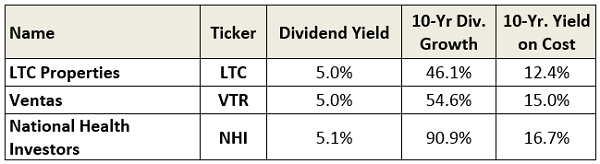

Our three landlords are already translating rising healthcare spending into some of the biggest dividends in the sector, with a yield averaging 5% now, plus 64% average dividend growth in the last decade:

High Yields Now and Later

You’ll notice I threw an unusual column in the table above: the 10-year yield on cost, which is the yield you’d get on a buy made a decade ago, thanks to these stocks’ surging payouts.

That alone makes these REITs pullback proof! Because if you’re counting on your portfolio for income and pocketing a safe 12% to 17% payout (or 14.7% on average), don’t need to pay too much attention to what stocks get up to on a daily basis.

With that kind of yield, you could likely retire on dividends alone.

But we will pay attention to these REITs’ underlying stocks. Because to truly make our “pullback-proof” list, a REIT must show some serious resolve when the rest of the market goes off the deep end.

So let’s check that now, starting with this latest pullback:

“Pullback-Proof” Domestic Plays Shrug Off the Trade War

If there’s one chart that shows the value of owning US-focused healthcare REITs, it’s this one, showing these stocks holding steady (and even rising) from May 6 through the 600-point dive the market took on May 13.

Now let’s take a look at the total return this trio handed us in the late-2018 flameout:

Healthcare Picks Ride Out the Storm

As you can see, our three picks posted a positive return, on average, and none fell nearly as far as VNQ and the broader market, which both tanked!

Let me leave you with one last thing that bolsters these stocks’ “pullback-proof” chops even more: bargain valuations, which cushion our downside while teeing up more gains.

As I write, Ventas trades at a reasonable 16.8-times forecast 2019 funds from operations (FFO, the critical REIT profitability measure), while NHI (15.6-times) and LTC (15.2-times) are even better deals.

How to “2008-Proof” Your Portfolio and Collect 7.5%+ Dividends

Ventas, LTC and NHI are textbook pullback-proof plays, but they’re far from the only stocks that can protect and grow your portfolio the next time the market pulls a 2018- (or heaven forbid a 2008-) style tantrum.

In fact, the late-2018 wipeout was precisely what prompted me to create my new 5-stock 7.5% “Pullback-Proof” portfolio.

The 5 stocks inside this unique portfolio have a lot in common with VTR, LTC and NHI, with two critical differences:

- They pay bigger dividends: as the name implies, these 5 buys pay a safe 7.5%, on average today! And that’s just the average. One of these unsung picks pays a rock-steady 8.5% dividend.

- They’re even cheaper, setting us up for bigger upside, particularly when the crowd finally clues in to the coming interest-rate cut. I’m calling for fast 7% to 15% price gains from these 5 “steady Eddie” picks, in addition to their huge cash dividends!

The bottom line?

If you’re worried about a 2008 repeat, these 5 stocks are for you. They’re each set to let you pocket their outsized 7.5% dividends without fear that the underlying share price will crumble beneath your feet.

To see what I mean, consider pick No. 2 of these 5 stocks. In 2018, a year most folks would rather forget, this battle-tested REIT soared double digits!

Big Gains in a Market Slump

And that 13.5% gain doesn’t even include this stock’s rock-solid 8% dividend, which lucky owners of this sturdy stock collected the entire time!

That’s a classic pullback-proof dividend in action, and you’ll see this story played out again and again across this 5-stock, 7.5%-paying “mini-portfolio.” Click here and I’ll share the names of these “2008-proof” income plays, including their tickers, ideal buy prices and my full analysis and research on each one.