The disaster that was 2020 is finally out of our hair, though there could be one silver lining if you followed a contrarian investing approach in 2020: serious gains in your stock portfolio.

But, of course, those gains come with a big consequence: Uncle Sam will be coming for his share on Tax Day in April. And to be honest, we don’t have much leeway to cut our 2020 tax bill at this point. But there is one canny move we can make to (legally, of course!) reduce our tax burden in April of next year: buy municipal bonds.

What Everyone Gets Wrong About Municipal Bonds

Sure, municipal bonds (issued by cities and states to fund local infrastructure) seem like a pretty boring option when there are corners of the stock market (I’m looking at you, tech) that jumped 40%+ last year. But that, in a strange way, is why we love munis: their low volatility gives a portfolio a strong base from which to build, and they pay us a nice dividend, too. Right now, in fact, you can grab attractive muni-bond funds trading at discounts to their true value and throwing off dividends yielding up to 5%.

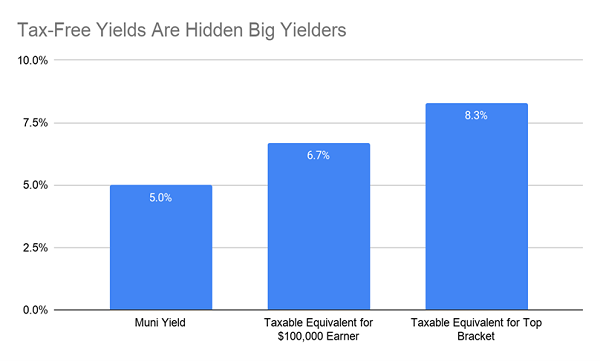

Here’s where their tax advantage comes in, because that 5% payout is tax-free for most Americans. That’s a critical advantage: if you’re in the top tax bracket, a 5% dividend equals 8.3% on a taxable basis, and that is roughly how much tech stocks rise on an annual basis in the long run, even though they are much riskier (and currently priced very high)!

So with munis, you’re grabbing the same long-term return you would with high-flying tech stocks but with a fraction of the volatility. Yet far fewer people invest in munis.

Source: CEF Insider

Here we can see how much muni bonds’ “true” yields rise along with your income. It’s a clear snapshot of why every investor needs to know what muni bonds can do for them.

Why ETFs Are Your Worst Option in Muni Bonds

There’s one thing we should address before we go further into munis, however: the muni market is a bit complex and tough for individual investors like you and me to access. That might tempt you to buy through an exchange-traded fund like the iShares National Muni Bond ETF (MUB).

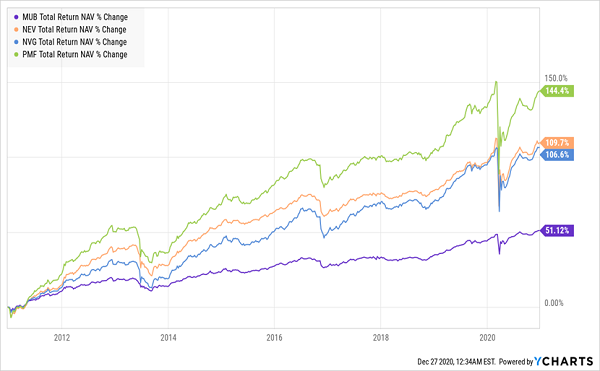

But the muni-bond market isn’t like the stock market. With munis, we need a knowledgeable pro with deep connections and research assets at the head of the funds we own. An algorithm-run ETF simply can’t compete, as we can see when we stack up MUB, in purple below, against the three actively managed closed-end funds (CEFs) we’ll look at next.

Muni-Bond ETF Comes Up Short

This type of underperformance isn’t just an issue for MUB, but for all of the muni-bond index funds. And these funds don’t even make up for their inferior performance with higher dividends: all of the muni-bond CEFs I’m about to show you yield around twice as much as MUB!

Even so, we can’t buy just any actively managed muni-bond CEF. We need to be particularly choosy now, as the COVID-19 crisis prompted the Federal Reserve to step in and buy muni bonds throughout 2020. That brought the market back to its usual, stable self and actually made munis safer than they were before the collapse. And with a further recovery in the cards in 2021, the muni market is poised to keep gaining as the Fed steps back.

But this gradual removal of support will also expose the weaker municipalities that have been leaning too heavily on Fed stimulus, so we’ll need our savvy managers more than ever to ensure our steady muni-bond upside (and dividends).

3 Muni-Bond CEFs With (Hidden) Yields Up to 8.3%—and Upside

Now let’s move on to our three winners in the space, all of which are run by the top-flight management firms with the wherewithal to make the most of the year ahead—and reward us with strong gains and dividends.

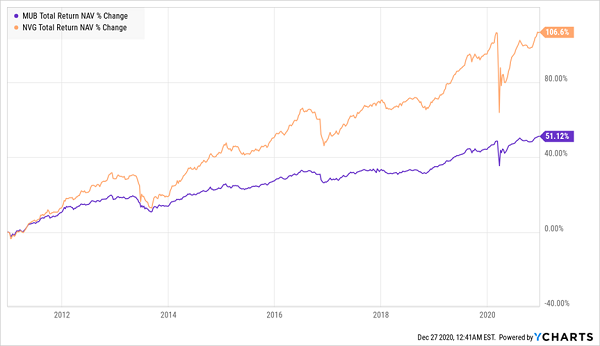

The first is the Nuveen AMT-Free Municipal Credit Income Fund (NVG), the largest muni-bond CEF, with over $3.5 billion in assets. As a result of its market dominance, municipalities will turn to NVG first when they want to sell new bonds, giving this fund some potent first-mover access. No wonder it’s up twice as much as MUB in the last decade.

NVG Rides Its Connections to Strong Gains

NVG also comes with a nice yield—4.9% currently. And the best part is, we can pick up this dominant fund at a nice discount: NVG currently trades for 5% less than its net asset value (NAV, or the value of the bonds in its portfolio).

Next up is the Nuveen Enhanced Municipal Value Fund (NEV), which is run by the same firm that manages NVG but takes a more aggressive approach, investing 80% of its assets in lower-rated muni bonds. Although that does add slightly to NEV’s volatility, the fund has also crushed the benchmark ETF, MUB, in the last decade, with a 110% return.

One thing that makes NEV a standout, however, is its propensity to pay out special dividends when its muni-bond investments outperform. It just did this last month, with a one-time payout that bumped 2020’s effective yield from 4.6% up to 5.2%. This is why NEV now trades at a small 2% premium to NAV and usually trades near its par value. Even so, this is a price worth paying, given its strong performance and the fact that it regularly drops special dividends on us.

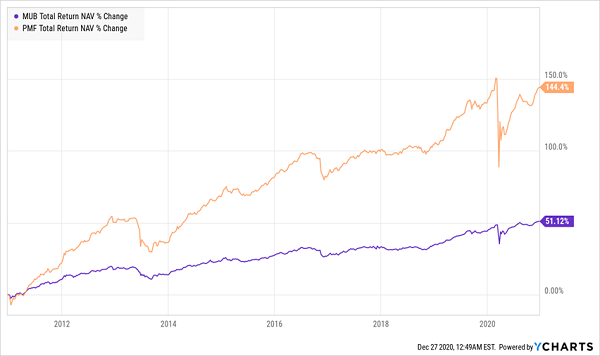

Finally, there’s the PIMCO Municipal Fund (PMF), payer of a 4.7% dividend. It’s run by PIMCO, the world’s second-largest bond buyer, and has nearly tripled the index’s return in the last decade:

PIMCO’s Muni-Bond Fund Delivers Stock-Like Returns

This outperformance comes at a price; PMF tends to trade at a premium to its NAV (currently 3.6%). That premium could hold back its upside in the near term, but it’s worth paying if you plan to hold the fund for a long time, due to PMF’s history of massive outperformance.

Do This Now to Add Growth (and 8.7% Dividends) to Your Tax-Free Payouts

Now let’s build on our tax-free dividends with 4 other CEFs I see handing you serious gains and big dividends as 2021 unfolds.

These 4 unsung funds yield 8.7%, on average, as I write this, and they trade at massive discounts that nicely position us for the two things we dividend investors crave most right now:

- 20%+ price upside if the market moves up from here in 2021, and …

- A nice downside hedge if there’s another collapse—because these funds are so cheap now, it’s tough for them to get a lot cheaper!

Either way, we’ll collect their huge 8.7% CASH dividends!

I’ve named these funds in an exclusive Special Report I’m making available to the public, and I want to make sure you get your hands on it. Go right here and I’ll give you a copy, which will reveal all the critical data on these 4 income plays: names, tickers, best-buy prices, complete dividend histories—the works.