Let’s talk about the cheapest dividend payers in the world. With respect to cold hard cash flow.

We contrarians are too savvy for P/E ratios. We know that earnings are accounting creations. “Profits” are all fugayzi.

Free cash flow (FCF), on the other hand, is what it is. The cash a company brings in, minus capital expenditures. This cash can be reinvested in the business or, better yet, paid out to income investors like us.

We like companies that dish dividends because their businesses are running on relative autopilot. They needn’t plow every dollar they raise back in. Which is great—more yield for us.

Here are five cheap dividend payers (with respect to FCF!) yielding an average of 6%.

Coterra Energy (CTRA)

Dividend Yield: 6.0%

Forward P/FCF: 6.1

Coterra Energy (CTRA) is perpetually cheap.

This oil, natural gas and natural gas liquids (NGLs) company has popped up on my radar again and again and again and again in recent months. It sprang to life just a couple years ago, in 2021, when Cabot Oil & Gas and Cimarex Energy merged to form it. It’s a major player in Texas’ and New Mexico’s Delaware Basin, also boasting acreage in the Marcellus and Anadarko basins.

Energy has given us little to celebrate in 2023, woefully underperforming the rest of the market with virtually flat performance. But Coterra has shown signs of life of late, with a beat-and-raise quarter justifying its recent run. Among other things? Oil, nat-gas, and NGL production were all better than expected, leading it to raise its full-year guidance.

I’m not surprised. I’ve previously said that Coterra is a strong operator in the space that’s more talented than most at wringing money out of each drop of oil, and its results continue to reiterate that.

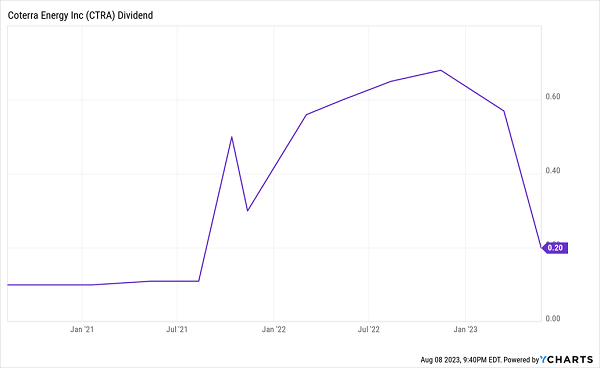

However, I’ve also mentioned previously that Coterra is a difficult holding for long-term income because of its fixed-and-variable dividend—it pays out a base dividend (that increased from 15 cents quarterly to 20 cents this year), then variable dividends as cash flows allow. However, CTRA made a slight adjustment to its policy this year—one that prioritizes share buybacks over variable dividends. Specifically:

“Due to market conditions and the value proposition of our shares, in 2023 we are realigning our strategy to focus on buybacks ahead of variable dividends. Our 2023 capital return priorities include paying our increased base dividend first, share repurchases second, and variable dividends third.”

So unless something changes drastically, that 6% yield—based off of Coterra’s trailing 12-month yield, which I use for fixed-and-variable stocks—is likely to drop to about 3% if CTRA continues only paying its base rate.

Well, It Was Nice While It Lasted

Ford (F)

Dividend Yield: 4.7%

Forward P/FCF: 4.0

Ford (F) is one of the most recognizable automotive names on the planet. Its flagship F-series pickup trucks have been America’s top-selling vehicle for roughly four decades, though in recent years, it has been trying (and in several ways, succeeding) to carve out a place for itself among the top electric-vehicle makers.

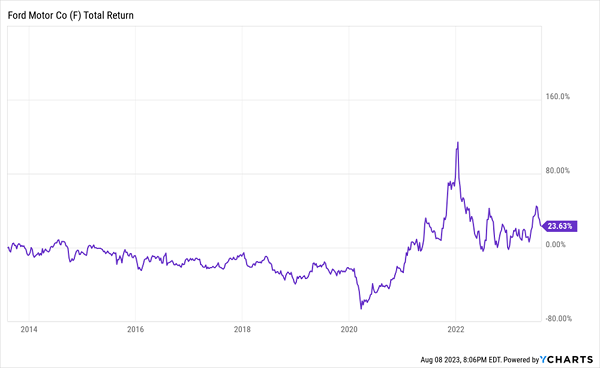

Ford has roughly doubled the industrial sector’s returns in 2023, with some of that driven by optimism over its adoption of Tesla’s (TSLA) charging network. This effectively gives Ford drivers access to some 12,000 superchargers—a move that should improve satisfaction among current Ford EV owners and spur new-EV sales.

Despite a 20%-plus gain in 2023, Ford trades at a very tame 4 times cash-flow estimates and offers a decent yield of nearly 5%.

Zooming out a bit, it’s clear investors aren’t as excited about Ford as its year-to-date returns might suggest. Ford remains stuck in a range it has largely maintained since 2021.

Ford Roared Out of the Pandemic Lows, But Has Settled Down Since

While Ford has assembled a competitive lineup of EVs, including the F-150 Lightning and Mustang Mach-E, it has recently dropped from the country’s No. 2 EV maker by market share to No. 5. It’s also behind the likes of Tesla from a technological standpoint—for now, it’s largely developing EV derivatives of vehicles based on existing internal combustion engine vehicle architectures.

I’ll also note that July—when a 2023 dividend increase likely would have been announced—came and went without any fanfare. Ford kept the payout level, which isn’t necessarily cause for concern, but it won’t excite income investors, either.

VF Corp. (VFC)

Dividend Yield: 6.1%

Forward P/FCF: 4.6

VF Corp. (VFC) is a collection of apparel brands mostly focused on the great outdoors, including Vans, The North Face and Timberland. It also used to include Wrangler and Lee jeans until 2019, when it spun off those brands via Kontoor Brands (KTB). And earlier this year, VFC said it would sell off Eastpak, JanSport and Kipling.

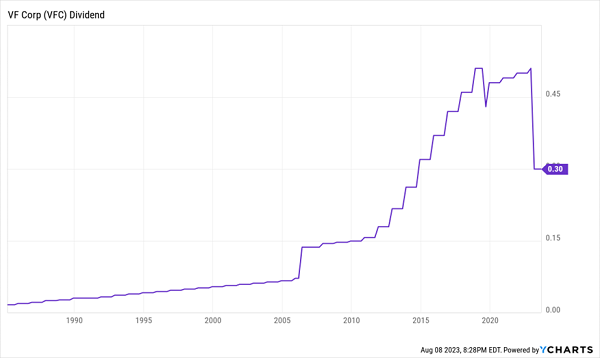

VFC was, for a long time, a stronghold of dividend stability in the notoriously fickle fashion industry. Its payout technically dropped in 2019, but that was only a reflection of the Kontoor divestiture. However, a genuine hammer-drop came this year, when VFC announced a 41% cut to its dividend (to 30 cents per share), all but guaranteeing that, come 2024, it will officially be dropped from the ranks of the Dividend Aristocrats.

Goodbye, Sweet Prince

The dividend cut is part of a multiyear turnaround plan meant to reverse the company’s financial fortunes. That plan also includes bailing on the aforementioned brands, selling off various assets (including its international headquarters), and cost-cutting meant to save $225 million annually by the end of 2024.

I mentioned earlier this year that one of its directors made a significant insider buy in Q1. Unfortunately for Director Juliana L. Chugg, it appears (for now) she bought too early.

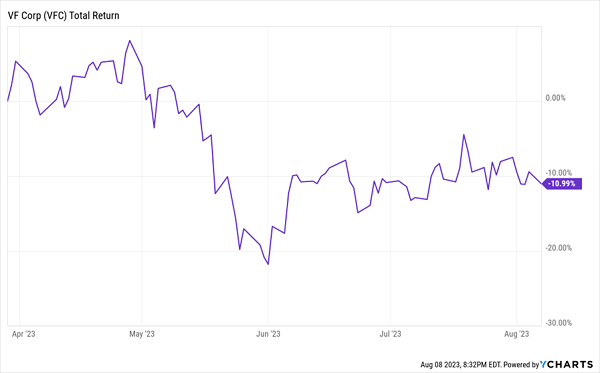

Was VFC a Discount Buy? Maybe. But It’s More Discounted Now.

VFC remains dirt-cheap based on cash flow, at 4.6 times estimates, though I will point out it’s still somewhat overbought based on PEG (1.4). A 6%-plus dividend could tempt some investors to stay and wait for light at the end of the tunnel.

The apparel company could very well be an eventual turnaround play, but for right now, it’s still showing major signs of struggle. It downgraded full-year revenue guidance from flat/slightly up to flat/slightly down. Successes in brands such as North Face (+12% YoY in the most recent quarter) are being offset by big declines in others such as Vans (-22%) and Dickies (-19%).

UGI Corp. (UGI)

Dividend Yield: 6.3%

Forward P/FCF: 4.5

Utility mainstay UGI Corp. (UGI) is not a dividend concern. It has paid dividends without interruption for 139 years, and it has raised them annually for 36, making it a Mid-Cap Aristocrat.

UGI is pretty interesting, as far as utility stocks go. Its core utility operations include UGI, which serves 675,000 gas customers in eastern and central Pennsylvania (and a few hundred gas customers in Maryland) and 62,500 electric customers in northeastern Pennsylvania; and Mountaineer Gas Company, which distributes natural gas to roughly 214,000 customers in West Virginia.

But UGI’s business also includes:

- Retail energy marketing

- Electricity generation

- HVAC

- Liquefied petroleum gas distribution in Europe

- Amerigas—America’s largest retail propane distribution operation, which UGI acquired outright in 2019

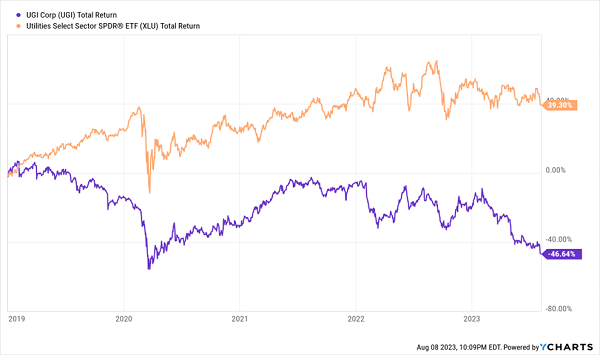

Despite being a utility (normally a recipe for stability) and offering a more diversified business portfolio than most of its sectormates, UGI has been simply dreadful in recent years, losing roughly half its value since 2019.

This Is Simply Not Normal

You can’t pin all of UGI’s troubles on any one factor, but the war in Ukraine was a big one. Astronomic rises in energy prices in Europe shellacked UGI’s cash flows last year, and the continent continues to hamper UGI this year. In May, UGI cut guidance for adjusted diluted EPS from a range of $2.85-$3.15 per share to a range of $2.75-$2.90 per share, blaming lower volumes “resulting from significant energy conservation in Europe,” as well as delivery challenges thanks to a driver shortage at AmeriGas Propane.

UGI is dirt-cheap, trading well below 5 times cash-flow estimates, and at a PEG of 0.8 that also indicates it’s oversold. Meanwhile, its 6%-plus dividend is well covered and boasts one of the most sterling payment track records on the public markets.

When this utility’s fortunes will improve is an open question—there’s nothing that screams a turnaround is right around the bend. But it’s hard to find fixer-uppers with more historical resilience than UGI.

Gap (GPS)

Dividend Yield: 5.7%

Forward P/FCF: 5.0

Speaking of fickle, Gap (GPS) is another cheap stock with a well-above-average yield, doling out nearly 6% right now. Shares trade at just five times cash-flow estimates, and why shouldn’t they? The last time GPS traded at current levels was during the COVID bear market. And before that? 2009.

That’s a Lot of Time to Go Nowhere

Gap’s four main brands are its namesake Gap, Banana Republic, Old Navy, and Athleta—an athleisure brand competing with Lululemon (LULU).

Gap is in the midst of an aggressive cost-cutting push, knocking out 500 corporate positions and renegotiating its marketing terms. Still, a few woes are countering these efforts, including a massive inventory imbalance—heavy on fleece and athletic wear, but light on going-out and back-to-office clothing—that forced it to discount heavily. A shaky economy has also pared back spending by low-income customers.

And remember: Gap was forced to suspend its dividend in 2020; it returned in 2021, but at roughly half the amount.

If there’s any good news, it’s that Gap has finally ended a year-plus CEO search, with Mattel (MAT) President and Chief Operating Officer (and Gap director) Richard Dickson taking over effective Aug. 22. Dickson’s background includes revitalizing the Barbie franchise during the 2000s—a feat he hopes to match at Gap.

It’s a promising turn of events, but it takes an iron stomach to jump into a stock in and around a management change.

How to Retire on Just $500K

Even if you were going to roll the dice on a management change, wouldn’t you want a better backstop? Yes, even at its reduced level, Gap’s nearly 6% dividend is far above the market average—but it’s not compensating you for the risk.

And it’s still well below the yield baseline most mom-and-pop investors need to hit to retire well.

If you want to get sleep at night without worrying whether you’ll retire in rags, you need to build a portfolio that can generate at least 8% in reliable dividends!

That 8% is a crucial number—one that could allow you to retire on dividends alone, even if you have a smaller nest egg of, say, $500,000 to work with.

The math is easy: At 8%, you’re generating $40,000 in cash from your retirement account alone. Combine that with Social Security, you’ll have plenty to work with once you’ve moved on from your career.

And if you have an even bigger pile of cash to plug into our 8% “No Withdrawal” Retirement Portfolio, you’re looking at a downright cozy retirement—one where you’ll never have to touch your original nest egg!

Dividend cutters like VF Corp. and Gap won’t fit the bill. But I have plenty of stealth payout plays that do yield the 8% or more that we need to coast forever on dividends alone. Please click here and I’ll share the details on my strategy for very generous dividends!