You know we’re in a pricey market when even obscure high-yield plays like closed-end funds (CEFs) are pricey!

But we can still find deals in this space, which is hands-down my favorite field in which to hunt for big payouts. In focus today: one totally overlooked fund (from an equally overlooked management firm) throwing off a hefty 7.6% dividend.

This deal can’t last—with yields so low on everything from government bonds to large cap stocks, investors will inevitably seek out this hidden high yielder. And we’ll be in with an early position when they do. (We’ll also delve into two other funds from the same management firm that you need to avoid at all costs.)

The Truth About CEF Discounts

If you’ve invested in CEFs before, you know that the discount to net asset value (NAV, or the value of the investments in a CEF’s portfolio) is a critical metric to watch. It measures the difference between a CEF’s portfolio value and the price at which it trades at on the market.

The upshot? You want to buy a CEF trading at a historically wide discount, then ride that closing “discount window” as it snaps shut, propelling the share price higher as it does.

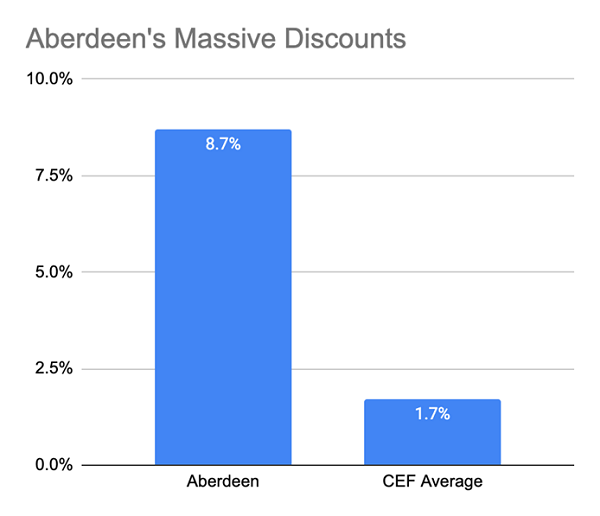

Trouble is, in CEFs, as with everything else, there aren’t a lot of discounts to be found these days. With an average discount to NAV of just 1.7%, CEFs are actually priced much higher than they usually are. To see how expensive this pricing is, consider that over the last decade, CEFs have sported an average discount of 7%.

CEFs are going for higher valuations in part because of what they do: offer big income streams (CEFs currently yield 6.9% on average) in the middle of a “dividend drought.” It’s not easy to pull $690 a year (or $57.50 a month) of income from a $10,000 investment, but CEFs do that—and it’s a heck of a lot better than the S&P 500’s paltry $10.83 per month on that same $10K!

That, by the way, is why now is still a great time to buy CEFs: their outsized payouts are still more than enough to encourage investors to snap up these funds, causing their market prices to rise. Plus, many CEFs are well diversified, holding stocks and bonds in some of the best companies in the world. Finally, the best CEFs have been beating their indexes for years—another big reason to jump in.

But that doesn’t mean all CEFs are worth your attention. One company’s funds—including that cheap 7.6% yielder I mentioned off the top—have slipped below CEF investors’ radar, and that’s where our opportunity lies today.

The Aberdeen Chill

Aberdeen Standard Investments has been around since 2017, when Aberdeen Asset Management (a British financial firm) merged with Standard Life, one of the biggest insurers in Britain. Aberdeen’s CEFs are a small part of the $700 billion in assets it manages, although the total number of CEFs it offers—11 in total—is more than many other CEF issuers do.

Still, seven of those 11 funds are steeply discounted, with an average discount of 8.7% among them. That’s much bigger than the average CEF discount.

Source: CEF Insider

Part of this is a geographical accident: Aberdeen’s base in Britain might be turning off some investors; another part of this is geographical intention: five of the firm’s most discounted funds are focused on countries and regions that have gotten less investor enthusiasm in recent years—Australia, Japan and emerging markets among them.

3 Deep-Discounted Aberdeen Funds—1 Winner, 2 Losers

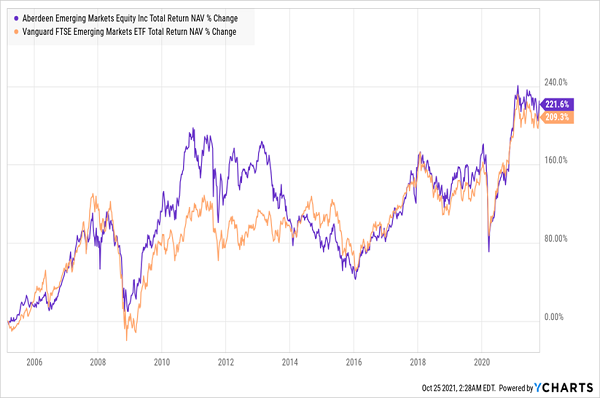

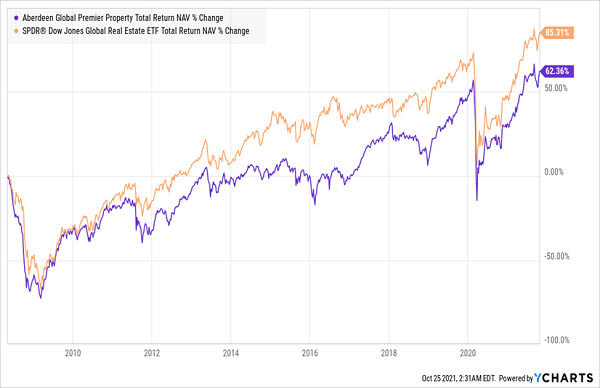

That regional bias explains the big discounts on the Aberdeen Emerging Markets Equity Income Fund (AEF) and Aberdeen Global Premier Properties Fund (AWP), which are trading 11.3% and 5.4% below NAV, respectively.

Just based on that, you’d think AEF, an equity fund whose portfolio includes large cap Asian giants like Samsung Electronics (SSNLF), Taiwan Semiconductor (TSM) and Tencent Holdings (TCTZF), is a dog.

But if we compare AEF’s NAV performance to emerging-market benchmark Vanguard FTSE Emerging Markets ETF (VWO) since VWO’s launch in 2005 (AEF is actually much older, having been launched in 1991), a different picture emerges:

Closely Following the Index—but With More Income

As you can see, AEF’s portfolio has been in lockstep with the broader market for emerging-market investments, which you’d expect from a large cap–focused fund. But here’s the difference: its 7.6% income stream is miles ahead of VWO’s paltry 2% yield, so AEF buyers get a big slice of their return in cash. That, plus AEF’s 11.3% discount, makes it an extremely compelling option.

The same can’t be said for AWP, a 7.4% yielder with a real estate focus as part of its global strategy. But that hasn’t really been helping AWP: it’s far behind the SPDR Dow Jones Global Real Estate ETF (RWO), a good benchmark for international real estate, making AWP an unappealing buy, especially with its relatively smaller discount.

AWP Takes Itself Out of the Game

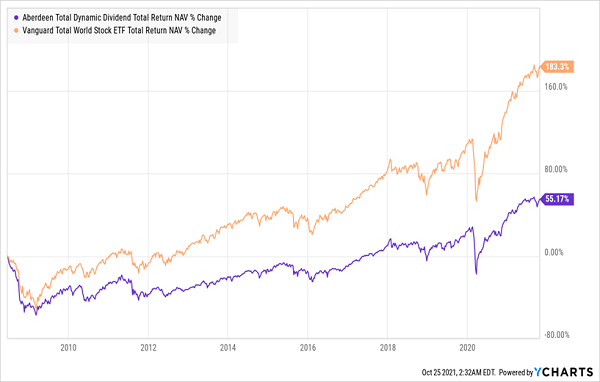

If we pivot to one of Aberdeen’s most popular (and also international) funds, the 6.9%-yielding Aberdeen Total Dynamic Dividend Fund (AOD), we really see how a close look at CEFs separates the winners from losers, even when they’re run by the same firm!

AOD’s 9% discount is massive and surprising for a fund that has $1.1 billion in assets under management (relatively big for a CEF). But when we look at the fund’s recent performance, we see that this fund is discounted for a good reason.

Global Stocks Run Over AOD

AOD’s return is a fraction of that of a global stock index fund, making it an easy-to-resist CEF that deserves its unusually big discount.

The Bottom Line? AEF Is the Aberdeen Fund to Buy Now

The fact that AEF’s discount is even bigger than that of AOD, despite it closely tracking the index and paying out a generous income stream, shows how inefficient the CEF world can be. And that makes for a great opportunity to get into AEF before its 11.3% discount closes.

4 CEFs That Crush AEF (With 7.3% Yields, 20%+ Upside Ahead)

AEF is one of a very few real “deals” in CEFs right now, but we’re far from out of luck here.

My team and I have spent months sifting through the CEF market and have uncovered 4 other CEFs that are even more attractive, offering equally huge 7.3% dividends but with an “upside edge” in the form of absurd discounts that set them up for 20%+ price upside in the next 12 months.

Add that big 7.3% dividend and your forecast gains together and you could easily be looking at a solid 27% in price gains and dividends by this time next year!

What’s more, this 4-fund portfolio offers much more diversification than you’d get by simply buying AEF and calling it a day. In 4 quick buys, you get access to the best real estate investment trusts (REITs), infrastructure stocks, corporate bonds, convertible bonds (which can “transform” into stocks to maximize your upside) and industrial stocks primed to soar in the ongoing reopening.

Don’t miss your chance to buy these 4 stout income plays now, while they’re still cheap. Simply click right here and I’ll give you the full story on all of my top 4 picks in a special investor report.