Plenty of investors buy corporate bonds because they think they’re safe investments.

That makes sense. After all, you do get your principal back at maturity. But corporates still have plenty of risks—particularly now, with interest rates arcing higher.

That’s why I’m recommending another asset class that’s set to deliver even higher yields and fatter capital gains—with much less to fear from interest rates. More on that in a moment.

First, let’s unpack these ideas one by one, starting with why so many investors just can’t kick their corporate-bond habit: corporates tend to offer higher yields than stocks while giving you exposure to the same companies.

For instance, let’s say you want to add to your portfolio’s financial sleeve, and you’re considering JP Morgan Chase & Co. (JPM).

Right now, the stock pays a 2.1% dividend yield, and the payout has grown about 10% annually over the last five years. But you also know that buying now means jumping in after the stock has shot up 56% in a year and at what may be the peak of the Trump rally in financials.

A Little Late to the Party?

But let’s say you still think JP Morgan is a good company, and you still want in. You can sidestep the risk of buying at the peak by purchasing bonds instead.

One issue by the bank (CUSIP 46625HJM3) may be a more attractive alternative. For one, this bond’s price has been pretty much flat over the past year. Secondly, it’s got an investment-grade rating from S&P, Fitch and Moody’s. Finally, it’s yielding 4.65% and will yield that until 2043, when you’ll get your principal back.

Of course, this is where the problems start.

First, to get this yield, you need to tie up your cash for 26 years. Assuming JPM keeps growing its dividend at the current rate, an investment in the company’s stock today will yield a whopping 24% in 2043, and that yield will pass the one on the corporate bond in just nine years.

Which brings me back to rising interest rates, a risk many investors ignore, choosing instead to worry that the bond issuer will default, which statistically has a much smaller chance of affecting your investment in this market.

And right now, interest rates are a huge risk for corporate bonds.

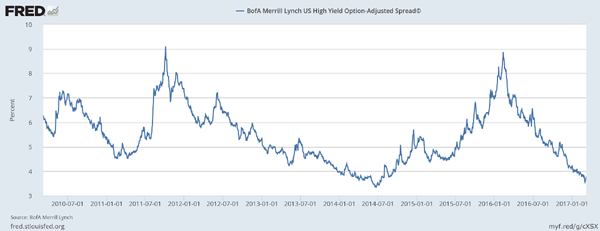

One indication: the BofA Merrill Lynch US high-yield option-adjusted spread—an obscure metric bond analysts obsess over because it measures the difference between the yield on junk bonds (or particularly high yielding, speculative bonds) and the spot-rate curve of US Treasuries (which is really just a benchmark for Treasuries issued over a long period of time).

The narrower the spread, the higher bonds have been valued and the less they yield. When this spread gets tighter, it tends to mean corporate bonds are overbought; when it widens, it means bonds are probably oversold. And right now, the spread is at its narrowest point since the subprime mortgage crisis.

A Risk-Hungry Market

Starting at the peak corporate-bond sell-off in early 2016, junk bonds have seen a beautiful bull run. I have no complaints; it has benefited me personally. But, as you can tell from the chart below, the bullish trend isn’t as steep as it used to be, and the bull run seems to be getting tired.

Junk Bonds’ Bull Run Getting Stale

I’ve already sold off some of my corporate-bond funds as a result of the weakening bull trend, and that now leaves me in a tough position. Where to go now?

The answer is ridiculously simple: municipal bonds.

While junk bonds, the Dow and the S&P 500 have been tearing it up over the past year, the iShares National Municipal Bond Fund (MUB) is down 2.5%:

Muni Bonds Get No Love

This shows that the municipal-bond market is well aware of the interest-rate risk the corporate-bond market is ignoring, which is why munis have sold off.

That means the risk of higher interest rates is already priced in and that muni-bond yields are going higher. This lets us grab a larger income stream while we wait for the eventual market reversal, where cash leaves the riskier junk bond and stock markets and seeks safe havens, including municipal bonds.

How to Beat the Fed and Collect a Safe 10.1% Yield

Municipal bonds aren’t the only income investments getting the cold shoulder right now. Another is closed-end funds, a corner of the market where investors like you are quietly pocketing safe, growing yields all the way up to 10.1%—and beyond.

Why are these high yielders out of fashion? The herd is way too worried that interest rates will send them tumbling.

But they’re completely wrong! Here’s how three of the most popular CEFs—the Gabelli Dividend & Income Trust (GDV), the Calamos Strategic Total Return (CSQ) and the Eaton Vance Limited Duration Income Fund (EVV) performed during the last rising-rate period:

During this two-year span, Fed chair Alan Greenspan boosted the federal funds rate from 1% to 5.25%. An earthquake. And CEFs did just fine.

Fast-forward to today, and this irrational fear has created eye-popping discounts throughout the CEF space, to the tune of 10%, 15% and even higher!

Which brings me to the 3 CEFs we’re recommending now. They give you safe, stable payouts of 8.2%, 9.9% and even 10.1%. Add them to the other 3 low-key picks in our “No-Withdrawal” retirement portfolio and you get a collection of investments throwing off a growing 8.0% payout!

So if you invest, say, $500,000 now, you’ll trigger a $40,000 income stream this year—and you can look forward to that taking a nice step up next year!

But other investors are starting to catch on to what they’ve been missing, and our unusual CEF discount window is starting to close. You need to make your move soon. Click here and I’ll give you these 6 investments’ names, tickers and our complete strategy now.