Is there a bond bubble? There’s certainly more froth than not, with investors recklessly reaching for the riskiest of yields.

But there’s one last 10% dividend on the board worthy of our consideration. It’s available thanks to investors’ misunderstanding (and laziness) – we’ll discuss details in a minute.

But first, let’s review three key rules that will help us navigate this budding bond bubble.

Rule #1: Maximize Your Upside

Our favorite second-level thinker Howard Marks noted in an op-ed for Barron’s that Netflix (NFLX) bond buyers – who recently scooped up €1.3 billion of Eurobonds paying just 3.625% – might have exposed themselves to significant downside without much upside.

After all, they bought the bonds rather than the stock. For 3.625% annually.

I’m with Marks – this is a low upside, high downside wager. Investors are forgetting that Netflix had to heroically reinvent itself just five years ago!

Bonds in This Rollercoaster? No Thanks

Apple’s Steve Jobs was fond of “betting the company” regularly on a new product, idea or technology. He believed that’s what it took to stay ahead of competitors.

And Jobs, of course, had a perfect track record on his own double-downs. But it was his shareholders who were richly rewarded – his lenders merely got paid back.

Meanwhile AT&T (T), which is three decades past its own technology pinnacle, just issued one of the largest bond offerings in recent memory. It’s expected to bank $15 billion from desperate yield seekers who will receive between 3% and 5%.

But AT&T’s stock pays a 5% dividend. And while its payout growth is limping along at a penny per share per year, at least there’s some yearly upside.

Still, though, that’s not enough for our income needs.

By now, you probably know my requirement for current income – 6% or better. (I only waive this for total returns of 12% or more annually.)

And 6% current yields are still available today. But most investors lament the S&P’s 1.9% payout and the 10-Year’s 2.4% coupon, because they don’t know where to look. We do, however – and we’ll talk 10% dividends shortly.

Rule #2: Limit Your Downside

Our 6% current yield minimum will assure us of 6% annual returns, provided we don’t lose any capital. This may sound obvious, but we can’t forget it.

A secure no withdrawal portfolio means we never sell shares for income. We may sell a stock or fund and then purchase another one, but we’re not eating our capital to create an income stream.

Contrast this with an annuity, which misleadingly includes return of capital in its “yield.” Or the “4% fallacy” – a notion crafted by hack financial advisors who pulled a safe withdrawal number out of thin air. The theory conveniently overlooks the fact that retirees who follow this advice will sell more shares when prices are low. A recipe for disaster.

Many income hounds share our affinity for 6%, 7% and 8%+ yields. But they reach for them, and forget to limit their downside.

That’s happening today in the closed-end fund (CEF) space. These vehicles were forgotten stepchildren just 18 months ago. But investors are so desperate for yield they’re piling into them – so much so that mainstream rags such as Business Insider are talking about them these days.

And there are plenty of ways to burn capital in CEF-land if you don’t know what you’re doing. Buy a bad fund (there are plenty of them). Or buy a good one at a premium (and overpay).

Here’s a real-life example that you may have already profited from yourself. In April 2016, I compared two bond funds. Both paid big 10%+ yields. Both benefited from a brilliant bond manager at the helm.

In fact, they shared the same manager – Jeffrey Gundlach, the Bond God himself. The man who dethroned Bill Gross as the supreme deity in fixed income!

And both funds shared a “wide mandate” that basically gave Gundlach and his team the go-ahead to buy anything they want. The only difference between the two last April was price per asset owned. The DoubleLine Opportunistic Credit Fund (DBL) traded for a 17% premium to its net asset value (NAV), while the DoubleLine Income Solutions Fund (DSL) traded for a 7% discount.

In other words, investors were paying $1.17 for just $1 in assets for Gundlach’s first fund – while paying just $0.93 on the dollar for the assets in his second fund. And there didn’t seem to be any good reason for the discrepancy, other than unlucky timing. Here’s what I wrote last April:

Buying DSL today gives us 5-7% upside as investors warm to Gundlach’s second fund. It’s not as popular simply due to unlucky launch timing – from late 2013 through the start of this year, investors fretted about the possibility of higher interest rates. Thanks to these worries, we’re presented with the best opportunity to buy DSL since inception – at a 7% discount, for an 11% yield.

How’d the last 13 months turn out? We enjoyed 33% total returns (including dividends) from our purchase of DSL. Meanwhile, investors who overpaid for DBL saw their money go nowhere:

Contrarians Win: DSL Soars Over its More-Popular Sister Fund

Sister fund DBL continued to pay its same monthly dividend, just as you’d expect. Its investors suffered a “lost year” simply because they overpaid for the fund.

Today, investors in these funds are making the same mistake. They’re paying up to $1.56 for just $1 in assets:

Don’t overpay for these funds. Make sure you demand a discount alongside your 6%+ yield.

Rule #3: Don’t Be Cheap About Fees

Most investors are conditioned by their experience with mutual funds and ETFs to search out the lowest fees, almost to a fault. This makes sense for investment vehicles that are roughly going to perform in-line with the broader market. Lowering your costs minimizes drag.

Fixed income is different, though. It’s an absolute necessity to find a great manager with a solid track record. Great minds tend to be expensive, of course – but they’re well worth it.

For example, take “preferred” shares. Companies issue them to raise capital, and they generally yield more than common shares.

Many investors who read about preferreds are tempted to buy “low cost” ETFs like the PowerShares Preferred Portfolio (PGX) and the iShares S&P U.S. Preferred Stock Index Fund (PFF). These funds pay 5.6% each and, in theory, they diversify your credit risk.

Problem is, they actually expose you to unnecessary credit risk. The only way you lose with this vehicle is by giving your money to a driver who crashes your car. But the S&P 500 and NASDAQ are large enough that there’s usually a company financially crashing into a brick wall at any moment in time.

Over time, these brick walls act as a much larger drag on performance than fees. You’re better off finding the best driver, and paying him or her well.

Two years ago, I introduced my Contrarian Income Report subscribers to my favorite preferred chauffer, the Flaherty & Crumrine Dynamic Preferred and Income Fund (DFP). After fees, it’s crushed its ETF counterparts two to three times over:

Our “Expensive” Driver Cruises Past These ETF Lemons

Remember, the stated yields you see quoted are always net of fees. So don’t make the common mistake of subtracting management expenses from the yield you see quoted – that’s already been accounted for.

When you consider net yields along with total return potential, you’ll see that the best bond managers are well worth paying for.

This Friday: The Last Safe 10% Yield

“Back in the day” it used to be easy for my subscribers and I to make a killing in closed-end funds (CEFs). We had a simple, profitable two-step formula:

- We’d buy a double-digit yield at a big discount, and then

- We’d bank the payout AND upside for safe 40%+ returns!

Yes, we’ve had fun contrarian times since the spring of 2016. That April, we actually purchased “Bond God” Jeffrey Gundlach’s DoubleLine Income Solutions Fund (DSL) for a fat 11% yield at a 7% discount to its net asset value (NAV). Our savvy purchase went on to crush the broader market, delivering 40.5% returns in just 16 months:

Gundlach’s DSL Became Quite Popular

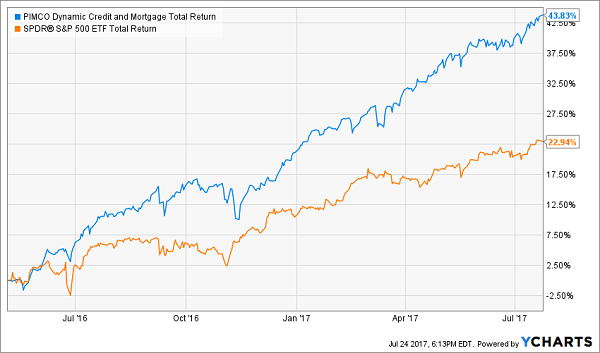

The following month we did it again. We found a 10% payer – issued by the ever-popular PIMCO no less – selling for a 10% discount. And we enjoyed 43.8% total gains from PIMCO’s Dymanic Credit and Mortgage Fund (PCI) in the 15 months to follow:

PIMCO’s Stepchild Fund Gains Favor

Of course these were easy pickings in hindsight. It’s hard to believe now, but the funds were quite out-of-favor at the time. DSL was dogged by its recent underperformance, while PCI carried the baggage of an investment strategy highlighted (and maligned) in The Big Short.

In the last eighteen months, as I mentioned, CEFs have trended back in vogue. Their discounts have narrowed and yields have compressed. But there’s one double-digit yield left, and it’s fittingly the offspring of a recent Bond God favorite.

This Friday, I’ll be sharing my full research on this “last safe 10% yield” to my No Withdrawal Portfolio. If you want to retire on dividends alone, my research will show you ten safe buys paying an average of 7.5%.

Which means a million dollars invested in these stocks and funds will be safe, diversified – and pay you $75,000 annually without you having to sell a share.

And here’s the kicker: your capital also enjoys 10% upside or better, thanks to the strategy I mentioned earlier.

Are you a current subscriber? If not, why not? We have a 60-day risk-free trial that will let you cancel and get your modest $39 investment back (no questions asked). AND I’ll let you keep all of my research for free.

Which means your downside is zero, and your upside is a secure, prosperous retirement funded by safe 7% to 8%+ dividends. Click here to get started and I’ll explain more about my no withdrawal approach – plus I’ll share the names, tickers and buy prices of my three favorite closed-end funds for 8.6%+ yields.