I heard the same question from readers all through 2022: when will we back up the truck and start buying again?

Your dividend strategist sympathizes. We “pivoted” early, starting back in late 2021, selling early and often in my Contrarian Income Report and Hidden Yields dividend-investing services.

Heck, we coined the term “pivot” long before the press did! And while Wall Street has been betting on a rebound all year, the truth is, they’ve been wrong, wrong and wrong again.

Now 2023 is here and we’re sitting on a big pile of cash. Of course, cash doesn’t pay dividends. But our mattresses are still outperforming 90% of investors out there!

Our Time for Big Dividends—at Big Discounts—Is Coming

Take heart, dear contrarian, because I believe we’re almost through this mess.

Big bear markets often break quickly and dramatically to the upside, just as they did in 2009, 2019 and April 2020. Our next moment is coming soon. The first quarter of 2023 is my current bet for the next big buying opportunity.

And when it comes, closed-end funds (CEFs) will be at the top of our shopping list. That’s because these often-overlooked funds can pay us three ways:

- High dividends: Many CEFs yield north of 7%, and CEF payouts well into double digits are common. What’s more, the majority of CEFs pay monthly.

- Portfolio gains: Even though they can seem a bit esoteric, there’s nothing mysterious about CEFs: they hold the same stocks, bonds, REITs and other investments you know well. And you’ll enjoy price gains from those investments when you hold them through a CEF, just like you would if you bought “direct.”

- The closing “discount window”: There’s one key difference with CEFs, though, and it works to your advantage: their market prices are often discounted to the value of their portfolios, a metric called the discount to net asset value (NAV). When these discounts get unusually wide—as they were in 2022—we can buy and ride along as they “snap shut,” catapulting the fund’s price higher! (See more on discounts to NAV in point #3 below.)

The bottom line here is that now is a good time to get our CEF shopping list ready. And I’ll tell you when it’s “go time” in Contrarian Income Report, which is focused on high-yield investments like CEFs.

I’ll show you how to grab a no-risk trial subscription to CIR below. Meantime, let’s dive into my 5-step “checklist” for buying CEFs, so we’re ready when the time comes.

CEF “Checkbox” # 1: Total, not Price, Returns Are the Key Performance Indicator

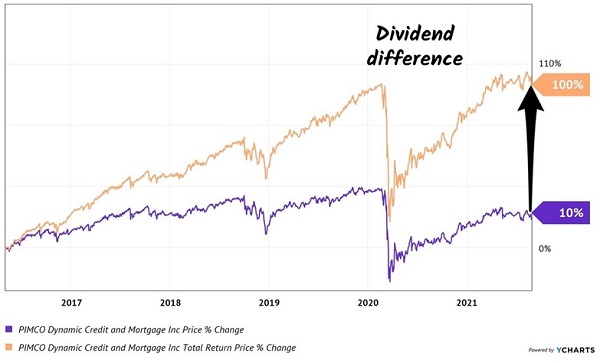

Because CEFs are high-yield investments, the price chart alone won’t tell you the whole profit story, and it could even mislead you into thinking a fund is a poor performer when that’s the furthest thing from the truth.

A look at a former CIR holding, the PIMCO Dynamic Income Fund (PDI), which merged with the PIMCO Dynamic Credit & Mortgage Fund (PCI) a while back (the combo doubled our CIR members’ money over a nearly six-year holding period).

PCI: Watch the Orange Line, Ignore the Purple One

A non-payout chart of PCI—the purple line—would miss this dividend double—orange line. The takeaway? Be careful about price-only charts when evaluating CEFs. Brokerage statements typically report price-only returns, too.

CEF “Checkbox” #2: Strong Past Performance (and Management)

The best way to zero in on a fund that can withstand anything 2023 throws at us is to look for those that have held up through thick and thin in the past. And be sure to look beyond the fund and consider its management firm, too.

For example, PIMCO CEFs almost never trade at discounts, for one reason: the firm has a history of strong performance in all markets. And that reputation makes it a magnet for top talent. (This also means that on the rare occasions when these funds do dip into discount territory, they’re always worth a look.)

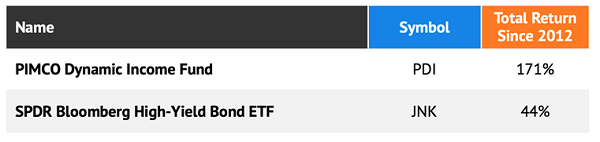

Consider PCI and PDI, which have had the benefit of the brightest bond minds on the planet calling the shots, from retired “Bond King” Bill Gross to current superstar Dan Ivascyn.

They have consistently beaten the bond benchmark SPDR Bloomberg Barclays High-Yield Bond ETF (JNK). Since inception, the merged PDI has pummeled JNK, delivering total returns of 171% versus 44%!

CEF “Checkbox” #3: A Discount—and a Plan to Close It

One aspect of the CEF structure lends itself perfectly to contrary-minded investing: a fixed pool of shares.

Mutual funds issue more shares whenever they want, fixed each day at NAV. But CEFs have a fixed share count, with their funds trading like stocks. As a result, from time to time a fund will fall out of favor. When it does, it finds its shares trading at the discount to NAV I mentioned earlier.

This is basically “free money” because these underlying assets are constantly marked to market (unlike mutual funds). If a fund trades at a 10% discount, management could theoretically liquidate the fund and pay everyone $1.10 on the dollar. Or it can buy back its own shares to close the discount window (and boost the share price).

A discount is a great start, but do make sure that management has a plan to close that window! Sometimes, the discount exists for a reason, so we dig deeper.

CEF “Checkbox” #4: Ensure Fees Are Backed By Performance (See Checkbox #2)

Most investors are conditioned to a fault by their experience with mutual funds and ETFs to search out the lowest fees. This makes sense for investment vehicles that are roughly going to perform in line with the broader market. Lowering your costs minimizes drag.

Usually, but not always. CEFs are different. On the whole, there are more dogs than gems. It’s a necessity to find a great manager with a solid track record. Great managers tend to be expensive, of course—but they’re well worth it.

Two other things to bear in mind with fees: one, they’re taken straight out of NAV, so you are never charged for them. And two, if your fund’s discount to NAV is greater than its fees, you’re essentially “hiring” management for free anyway! This is another totally ignored benefit of CEFs.

CEF “Checkbox” #5: Insider Ownership

We always like to see management teams with their own personal cash invested in their funds. After all, if their interests are the same as ours (to enhance our dividends and gains, in other words), they’re likely to work that much harder to ensure these things happen.

Insider ownership isn’t always easy to spot with CEFs, but it is part of my research at CIR. For example, Bradford Stone, one of the managers at the Flaherty & Crumrine Dynamic Preferred and Income Fund (DFP), holds 26,667 shares worth around $549,340 today. DFP was also good to us at CIR, delivering a 57% return in a little under seven years—a solid return for a bond fund—and it was entirely in dividend cash.

Get Instant Notice When We’re Set to Buy—and the 8%+ Payouts We’ll Be Targeting

As I said above, I’ll let my Contrarian Income Report subscribers know when the time comes to buy—and exactly which stocks (including CEFs!) we’ll be picking up.

You can make sure you’re in line to take full advantage when you take out a 60-day trial membership to Contrarian Income Report.

That’s not all: you’ll also get full details on my high-yield investing strategy—including my proven plan to help you retire on dividends alone. Plus you’ll get an exclusive Special Report revealing the stocks and funds I see as perfect buys right now to make my “no-withdrawal” retirement plan work.

Don’t miss this unique opportunity. Click here to learn all about this powerful “no-withdrawal” retirement strategy and start your 60-day trial to Contrarian Income Report now.