Wall Street suits tend to avoid business development companies (BDCs). That’s a mistake. For us income seekers, these “Main Street bankers” can be the best dividend machines in the market.

Forget the “penny yields” most stocks pay. BDCs can dish divvies between 10.6% and 12.6%. Unlike vanilla blue chips, BDCs are mandated by Congress to flip us at least 90% of their taxable income.

In other words, the dividends are a “built in” feature.

Of course we don’t just close our eyes and buy any 12% payer. Some BDCs are dividend machines, others are disasters. Our job: separate the stars from the scrubs and only buy the cash cows.

BDCs are basically banks for Main Street. They lend to small and mid-sized companies that can’t tap the bond market the way Apple or Microsoft can. These borrowers pay a premium for their capital, which BDCs funnel right back to us as payouts.

Most BDC loans float with the Fed. That looks scary with rate cuts coming. But it also brings lower borrowing costs for the BDCs themselves—and relief for the companies they lend to. Healthy borrowers mean stronger dividends.

As I recently wrote about Morgan Stanley Direct Lending Fund (MSDL, 11.1% yield):

Here too, there’s a “bullish disconnect” for us to exploit. When the Fed cuts its policy rate—pacesetter for the rate at which financial institutions lend to each other—BDC loan income typically declines, especially floating-rate loans, an MSDL specialty (99.6% of its portfolio). The Fed is likely to cut in September.

This seems like bad news, but the crowd is missing the real story, as lower rates drive up loan demand, especially when businesses plan to grow (see small-business optimism above). That helps offset lower loan income and gives BDCs more floating-rate loans (whose income will gain when rates rise again).

Floating-rate debt goes both ways. If a company has a lot of floating-rate assets (their portfolio lending) but also a healthy amount of floating-rate debt, a lower portfolio yield might be offset by a lower cost of paying off that debt.

MSDL, by the way, is a (currently) bargain-priced BDC backed by Morgan Stanley (MS) that invests across several dozen industries. (My full breakdown of MSDL can be found here.)

Other BDCs piquing my interest right now?

Trinity Capital (TRIN, 12.6% yield) went public in January 2021 and has been one of the most productive BDCs since then, including a 20% total return in 2025 that puts it among the industry’s best this year.

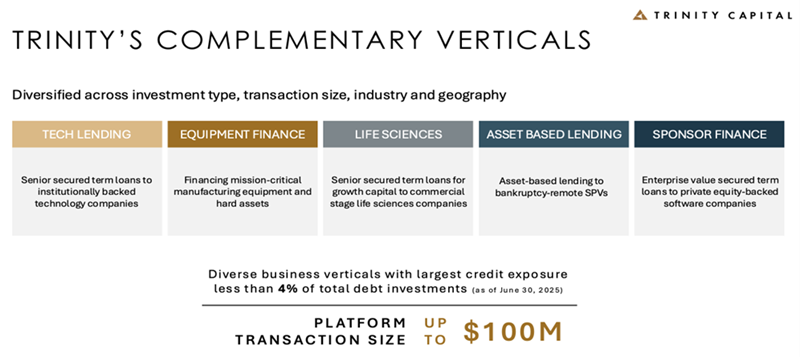

Trinity, which deals almost exclusively in growth-stage companies, operates under a five-pronged model:

Source: Trinity Capital Q2 Investor Presentation

They’re not equal prongs: Debt makes up about 75% of portfolio investments by fair value, while equipment financings command 17%, and equities and warrants account for the rest.

Unlike many highly diversified BDCs, most of Trinity’s investments are on the bleeding edge of something or another. Space technology. Green technology. Healthcare technology. Plain-old technology technology, too, such as artificial intelligence and automation. Portfolio companies include the likes of spaceflight safety firm Slingshot Aerospace, quantum computing company Rigetti and fast-rising non-alcoholic craft brewer Athletic Brewing.

Trinity deals in floating-rate loans—plenty, in fact. But at 80% of outstanding principal, it’s not as exposed as many other BDCs. Moreover, more than half of its portfolio is at floor rates (the minimum interest rate for a variable-rate loan), which could blunt some of the damage of future Fed rate cuts.

Just mind the cost. Trinity is attractive, and investors know it—TRIN’s march higher has shares trading at a 22% premium to its net asset value.

Down here on planet Earth is Oaktree Specialty Lending Corp. (OCSL, 12.0% yield), which trades at a nice 16% discount to NAV.

Its 149 portfolio companies are spread across a variety of industries—top among them software and services, and health care equipment and services—with a heavy cyclical bent.

It primarily deals in senior secured debt, and most of that is of the first lien variety. It also invests via second lien and unsecured debt, as well as equity. More than 90% of the debt portfolio is floating rate—elevated, yes, but there’s at least a little exposure to fixed-rate loans.

Source: Oaktree Specialty Lending Corp. Q3 2025 Earnings Presentation

Oaktree specializes in distressed and opportunistic credit markets, which can be lucrative, but its risk-taking doesn’t always pay off. From a performance standpoint, Oaktree significantly broke from the BDC industry starting in 2024, with the former declining by the high teens and the latter growing by just as much. OCSL was forced to cut its regular dividend by 27% earlier this year, to 40 cents per share. It also issued a 7-cent supplemental distribution in Q1, a 2-cent supplemental in Q2, and no additional dividends in Q3.

While portfolio credit quality showed signs of stabilizing in the most recent quarter, one quarter doesn’t constitute a comeback. Results post any Fed cuts will need to be closely watched to determine whether the dividend can be maintained, even at this lower rate.

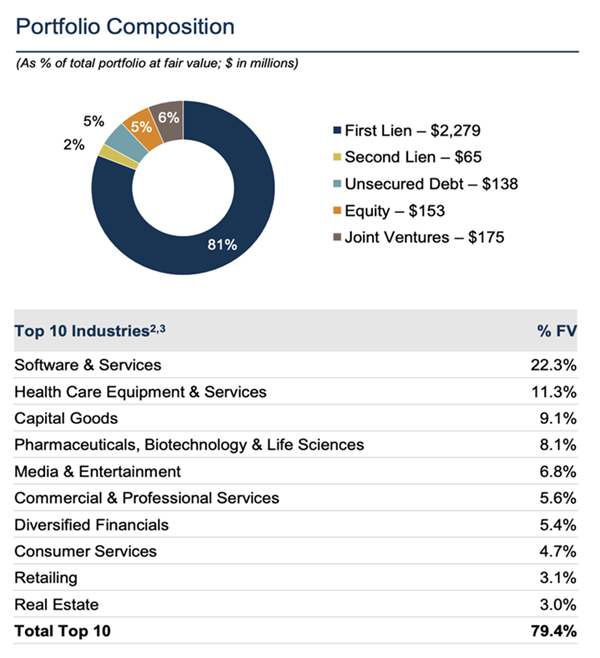

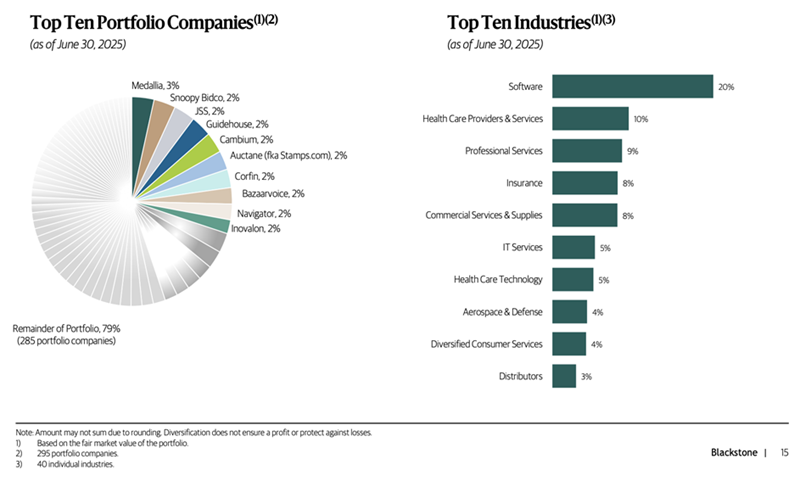

Blackstone Secured Lending Fund (BXSL, 10.6% yield) is one of a number of BDCs that has access to the rich resources of a larger company—in this case, Blackstone (BX) arm Blackstone Credit & Insurance, one of the world’s largest alternative credit platforms. Portfolio companies benefit from the Blackstone connection, too, with BXSL providing expertise and operational support.

BXSL almost exclusively deals in first-lien senior secured debt to upper-middle-market companies; it’s among a mere handful of BDCs with the scale to lead these kinds of deals. (Thanks, Blackstone!) It also has a massive portfolio of 295 investment companies; industry mix leans cyclical, but the focus on upper-middle-market tamps down risk.

Source: Blackstone Secured Lending Fund August 2025 Investor Presentation

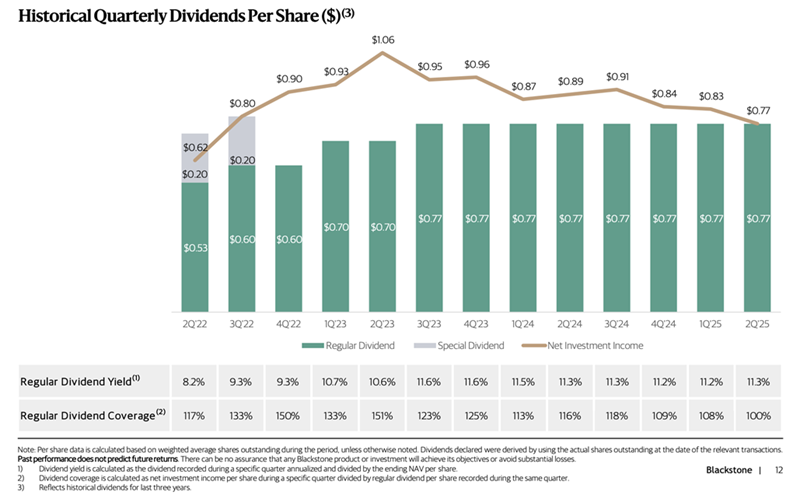

BXSL has outperformed the industry since its October 2021 IPO, but that edge has dulled. Of the most concern is dividend coverage, which has dwindled from “generous” to “barely scraping by.”

Source: Blackstone Secured Lending Fund August 2025 Investor Presentation

More than most, BXSL bears watching in the wake of a Fed cut, as Blackstone might decide the dividend doesn’t make sense at current levels. Shares are pricey given those prospects, too, at a 7% premium.

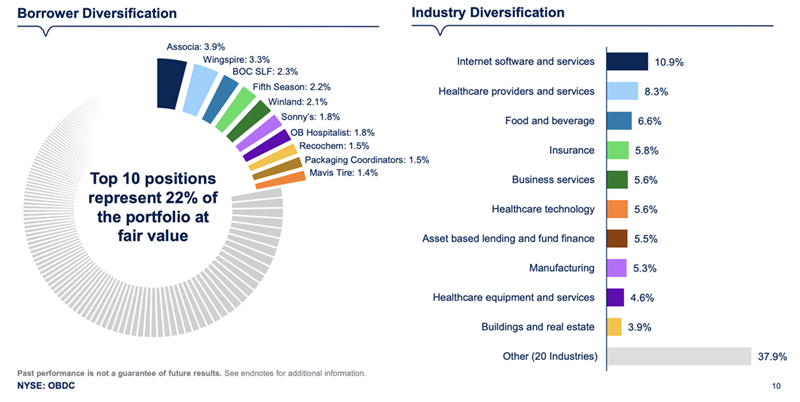

Blue Owl Capital Corp. (OBDC, 11.3% yield), formerly Owl Rock Capital Corporation, originates, executes, and manages debt and equity investments in American middle-market companies, typically with annual EBITDA of between $10 million and $250 million, and/or annual revenue of $50 million to $2.5 billion at the time of investment.

OBDC currently invests in a wide 233 companies, largely via debt (including 81% senior secured loans), 98% of which is floating-rate in nature. The portfolio is extremely defensive, with an emphasis on stability traits: high recurring revenues, high switching costs, recession-resistance.

Source: Blue Owl Capital Corp. August 2025 Investor Presentation

OBDC hasn’t exactly stood out over its roughly six-year history, largely trading in line, if not a little below, the BDC industry. And there was little in its most recent quarter to suggest that this dynamic will change anytime soon. Non-accruals (loans that are delinquent for a prolonged period, usually 90 days) ticked higher. NAV ticked lower. Revenues were only in-line with expectations.

But it’s deploying capital despite a depressed M&A environment, leverage has retreated back to within OBDC’s target range, and its Q3 supplemental dividend improved over Q2. And while it’s not dirt-cheap, it does trade at a 5% discount to NAV.

Avoid the Retirement ‘Death Spiral’: Collect 8% or More for Life

Despite BDCs’ sky-high income potential, most income investors won’t go near them because they’re outside their “safety zone.”

You know the drill. Buy blue chips and bonds. Dollar-cost average in. Slow and steady wins the race.

Here’s the problem: If you’ve saved and invested “by the book,” you’re already behind—and all it might take to realize that is one poorly timed downturn in retirement. That could force you to sell a much bigger chunk of your portfolio to withdraw the income you need to pay the bills, and suddenly, you’re way behind the 8-ball for the rest of your post-career years.

But you can avoid this income “death spiral” by making sure you live on dividends alone.

My 8% “No Withdrawal” Retirement Portfolio can do just that: produce a high level of income (without the big Fed question marks accompanying a few of these BDCs) that allows you to retire on dividend and interest income alone.

That means never having to touch a penny of your nest egg, which means you can use it for a truly rainy day, or eventually pass it on to your heirs.

With the “No Withdrawal” portfolio, even $500,000 in savings—far less than CNBC’s talking heads say you should have piled up—can generate a $40,000 “salary” in retirement.

And if you’ve socked away even more, all the better!

Let me show you the stealth payout plays that Wall Street overlooks—names that yield 8%, 9% or even more that can help us coast forever on dividends alone. Click here and I’ll share more details on these secure funds with very generous dividends!