If there’s anything better than monthly dividends, well, we contrarians don’t want to know about it. Getting paid on the same schedule as our bills (monthly!), makes retirement planning easy.

We still need enough yield, though, to get rid (and stay rid) of our day jobs. Our pile of savings is what it is at this point, so we look to larger dividends to do the heavy lifting for us.

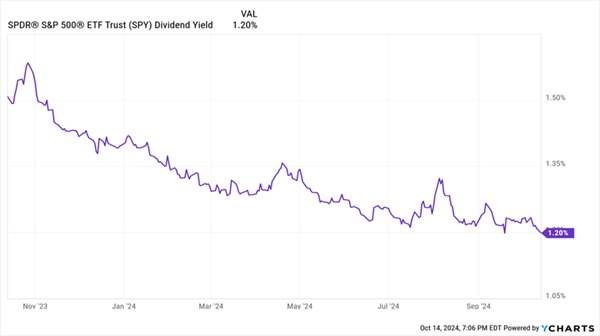

The S&P 500, needless to say, won’t cut it. First, the “SPY” pays quarterly—not often enough! Second, it pays 1.2%—not high enough!

“The Market” Is Paying Just Pennies

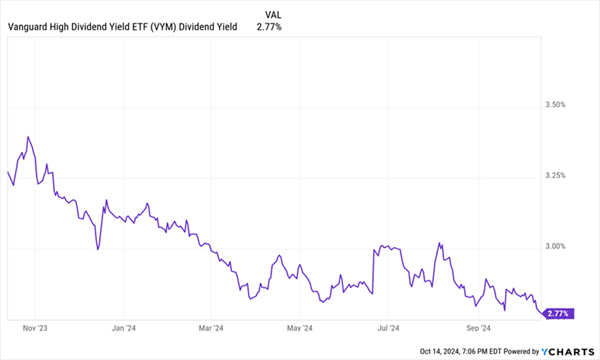

Even yield-focused funds’ yields are pretty lame right now. Two-point-eight percent—what kind of a high dividend fund is this?

Since When is 2.8% a High Dividend?

Let’s move on to five monthly payers dishing 6.2% to 13.7% dividends. On a $500,000 retirement nest egg, that’s $31,000 to $68,500 in annual dividend income.

LTC Properties (LTC)

Dividend Yield: 6.2%

The great thing about monthly dividend stocks is they span most of the market’s most familiar high-yield industries.

I’ll start with a real estate investment trust (REIT): LTC Properties (LTC). LTC, of course, is a nod toward “long-term care”—the heart and soul of its portfolio. This REIT boasts more than 190 properties, with a roughly 55%/45% gross investment split between assisted living properties and skilled nursing facilities.

Long-term care suffered a PR black eye and massive losses during the COVID pandemic, but most REIT operators in the space have turned things around. Operationally, LTC is at least back on its feet; from a stock perspective, however, LTC has a lot more ground to recover.

LTC Is Still Well Off Pre-COVID Levels

LTC is finding meaningful growth elusive, with 2024 and 2025 adjusted funds from operations (AFFO) expected to be largely flat to down from 2023 levels. That’d be easier to swallow if LTC was still deeply discounted, but the market is being realistic about shares, which trade for a fair 13 times AFFO.

As the chart also shows, LTC hasn’t touched its monthly dividend in years, though that’s a mixed bag. No growth? Not good. But LTC also didn’t have to suspend or lower its payout during the pandemic, which sets it apart from many of its REIT peers. And today, that dividend remains very well covered.

Here’s what I’m keeping an eye on: Wedbush analysts recently said that LTC, which currently has a triple-net-lease-only strategy, is considering pursuing a RIDEA structure, which stands for the REIT Investment Diversification and Empowerment Act. Without getting too far into the weeds, this act lets REITs participate in net operating income, and it’s where LTC sees the majority of external growth opportunities in assisted living. Any moves in this direction aren’t expected until 2025, but it’s a potential catalyst that could finally get LTC stock out of the dumps.

AGNC Investment Corp. (AGNC)

Dividend Yield: 13.7%

AGNC Investment Corp. (AGNC) is a REIT, too, though it’s in its own class. Unlike traditional REITs, which deal in physical properties, AGNC deals in “paper” real estate (read: mortgages).

And while an $8 billion market cap is mid-cap territory at best, that makes AGNC a whale in the mortgage REIT (mREIT) pond.

mREITs buy mortgage loans and collect the interest. They make money by borrowing “short” (assuming short-term rates are lower) and lending “long” (if long-term rates are higher, which they usually are).

AGNC deals in residential mortgage-backed securities (MBSs) from government agencies like the Federal National Mortgage Association (Fannie Mae) and the Federal Home Loan Mortgage Corporation (Freddie Mac). And it uses a heaping helping of leverage to monetize its investments—a recipe for disaster during times of rising and high rates, but great news as rates start making their way lower.

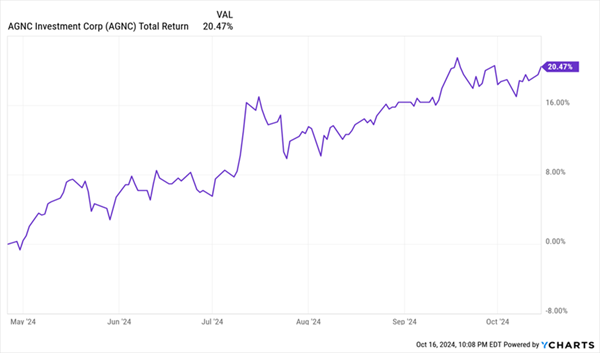

In fact, back in April, I said about AGNC:

“Spreads should tighten if the Fed finally starts easing, which should provide some lift under mREITs in general, and better operators like AGNC in specific.”

As it turned out, AGNC didn’t have to wait for the easing itself—it started rallying as Federal Reserve cuts became more certain. April marked the year-to-date lows in AGNC stock, and shares have delivered a 20%-plus total return since my article.

Fed-Fueled Jubilee for AGNC

AGNC features little credit risk, and as an agency MBS dealer, it’s in prime position to benefit from future Fed rate cuts. I just wish it were cheaper; the stock currently trades at 1.25 times tangible book value.

We would highlight AGNC among the agency REITs. While the valuation isn’t cheap at close to ~1.2x estimated TBV, we think the company’s market positioning as the only large-cap pure-play agency MBS REIT should allow it to continue trading at a premium to book given the current attractive operating environment.

Prospect Capital (PSEC)

Dividend Yield: 13.6%

I’ll move on to another high-yield acronym: business development companies (BDCs).

BDCs, which are structured like REITs (including the dividend mandate), provide financing to small- and midsized businesses, often doing so when banks and other traditional financiers won’t. They’re actually just like private equity in that their portfolios offer exposure to dozens if not hundreds of private companies, but BDCs are publicly traded, so these “rich guy loophole” stocks give us PE-esque exposure for a few bucks a share.

Prospect Capital (PSEC), at more than $2 billion in market cap, is one of the biggest names in the BDC industry.

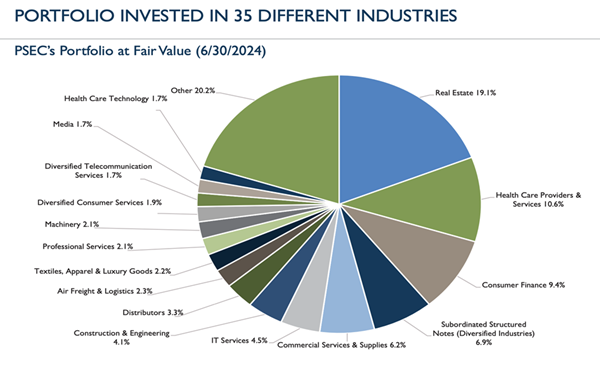

Its portfolio includes 117 investments across 35 industries, and the majority (81%) of those investments are first lien, secured, or underlying secured debt. The bulk of its business is in middle-market lending to companies with EBITDA of up to $150 million, though it also participates in real estate (typically multifamily properties) and subordinated structured notes.

Source: Prospect Capital Q2 Investor Presentation

There’s a lot to like on its face. PSEC offers a massive double-digit dividend with good net investment income (NII) coverage for a while. It boasts a massively diversified portfolio. Non-accrual loans are a thin 0.3%. And it trades at just 60% of its NAV, making it the cheapest stock among any of the BDCs I regularly keep my eye on.

The problem? PSEC isn’t momentarily cheap—it’s perpetually cheap, on account of its dreadful underperformance since 2021. That dividend has been cut multiple times in its past, most recently in 2017, and it hasn’t budged a cent since then. Bloomberg has recently joined us in noticing Prospect’s financial issues.

I’ve repeatedly warned readers about the dangers of betting against a stock like PSEC, because its dirt-cheap valuation is likely to add fuel to any stock gains should it receive a short-term boost of positive sentiment.

But the burden of proof is on Prospect, and that burden is high.

DNP Select Income (DNP)

Distribution Rate: 8.1%

We can also get ridiculously high monthly dividends from closed-end funds (CEFs), which aren’t as well-known as mutual funds and ETFs, but have a few distinct advantages. Most notably, CEFs can use leverage to amplify returns. And their share price can disconnect from the fund’s net asset value (NAV), allowing us to occasionally buy these funds at a discount.

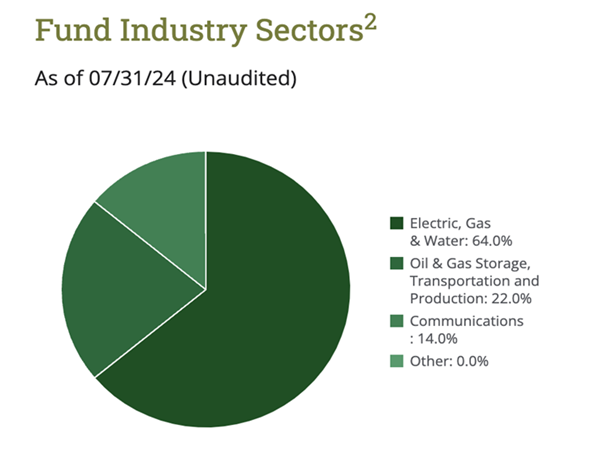

DNP Select Income Fund (DNP) is a utility fund, with a twist. This CEF invests across traditional electric and water utilities such as Sempra Energy (SRE), CenterPoint Energy (CNP) and XCEL Energy (XEL). But it also holds utility-esque companies such as American Tower (AMT), a REIT that owns telecommunications infrastructure and leases it out to the likes of AT&T (T) and Verizon (VZ)—which DNP also owns. It even holds a few MLPs.

A Diversified Utility Fund

Source: Duff & Phelps

Also, DNP doesn’t strictly hold equities—16% of the portfolio is invested in bonds and cash. Meanwhile, it uses moderately high debt leverage of 25% to get more out of management’s selections, which is also how a utility fund is able to yield a fat 8%.

Unfortunately, this Duff & Phelps fund constantly trades at a premium. DNP trades at a five-year average premium of 16% of NAV, and it traded for as much as 31% earlier this year. That said, we’re happy to trade it—like we did this year in Dividend Swing Trader—when the premium gets low enough.

PIMCO Corporate & Opportunity Fund (PTY)

Distribution Rate: 9.9%

The PIMCO Corporate & Income Opportunity Fund (PTY) invests in a variety of debt. Currently, junk bonds are tops at roughly 35% of assets, followed by non-agency mortgage securities (12%), non-U.S. dollar-denominated developed-market bonds (11%) and emerging-market debt (11%). The rest is sprinkled across a few other debt types.

It’s difficult to compare PTY to other bond products because it’s a multisector fund—and while there are a variety of competing funds out there, they’re likely to hold very different investments from one another, not to mention their allocations could change significantly over time.

But let’s compare this PIMCO product to a pair of the largest multisector bond ETFs.

It’s Not Even Close

Yes, this is a shorter-term chart just given CGMS’s lack of trading history, but PTY has delivered over the long run, too. Indeed, it’s a Morningstar five-star-rated CEF, and it sits in the 99th percentile by performance over every meaningful time period.

Alas, while a truly great fund might be worth a premium, we’d have to pay a ransom to buy PTY shares, which currently trade at an eye-popping 24% above its net asset value!

How to Build a High-Yield Monthly Income Stream WITHOUT Overpaying

You wouldn’t buy a car for 24% above MSRP, and COVID-era homebuyers can tell you how painful it is to pay 24% above the asking price. So why would you kneecap yourself by purchasing a fund for 24% above NAV—especially when there are still plenty of reasonably priced monthly payers ripe for the picking?

Case in point? My “8%+ Monthly Payer Portfolio” is chock full of reasonably priced “steady Eddie” stocks that deliver sky-high yields … and beautifully boring businesses that won’t give you nausea over the years … and meaningful price upside, which means we can keep growing our nest eggs well after we’ve hit the retirement button.

This is how we win in retirement.

Many retirement plans build your nest egg, only to turn around and ask you to bleed that same nest egg dry as you age. But the income this portfolio can generate is so rich, it can sustain a retirement on dividends alone.

Here’s the math: If you have a million dollars to work with, an 8% baseline will net you $80,000 a year.

But even if you’re well behind on your retirement savings—let’s say you only have $500,000 to work with—you’ll still generate a roughly $40,000 annual income stream.

That’s $3,330 every month in regular income checks!

Can your current portfolio deliver that level of income? If not, it’s time to make a change. Click here to learn everything you need about these generous monthly dividend payers right now!