It’s a question I get from investors all the time: “Should I take my dividends in cash or reinvest them through a dividend reinvestment plan (DRIP)?”

My answer: unless you want your cash sitting in your account earning zero, your best bet is to reinvest any dividend money you don’t need to pay your bills.

But we don’t want to practice “buy and hope” investing, either, whether we do it through obsolete DRIPs or the old-fashioned way.

When I say “buy and hope,” I mean putting your cash into household names like the so-called Dividend Aristocrats and “hoping” for higher stock prices when you cash out in retirement.

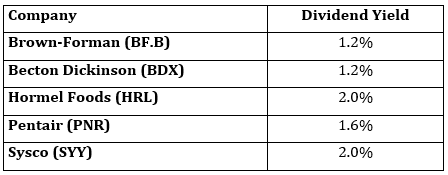

You’ve probably heard of the 53 stocks on the Aristocrats list, which have raised their payouts for at least 25 straight years. Trouble is, despite their lofty name, these companies hand us a pathetic current dividend of 2.2%, on average.

And many pay a lot less:

5 Dividend Paupers

So if you invest mainly in these stocks (as many people do), you won’t have to worry about reinvesting your dividends. You’ll need every penny of dividend income just to keep the lights on!

That’s because even with a $1-million portfolio, you’re only getting $22,000 in dividend income a year here, on average. That’s not far above poverty-level income for a two-person household.

Pretty sad after a lifetime of saving and investing.

Luckily, there’s a way we can rake in way more dividend cash. I’m talking a steady $75,000 a year in income on a million bucks. And if you’re not a millionaire, don’t worry: a $550k nest egg will bring in $41,200 annually, enough for many folks to retire on.

That’s 59% more income than our million-dollar Aristocrat portfolio, from a nest egg that’s a little over half the size!

How to Bank an Extra $41,200 in Cash Every Year

I know what you’re thinking: “Brett, that amounts to a 7.5% yield. There’s no way a payout like that can be safe.”

You can be forgiven for thinking that, because you hear it everywhere (heck, even my financially savvy personal trainer didn’t believe payouts like this were possible).

But the truth is, there are plenty of safe payers throwing off at least that much, like the 19 stocks and funds I recommend in my Contrarian Income Report service (which I’ll show you when you click here).

Right now, these 19 sturdy investments yield 7.5%, on average. And every month I personally run each one through a rigorous dividend-safety check, starting with 3 things that are absolutely critical:

- Rising free cash flow (FCF)—unlike net income, which is an accounting measure that can be manipulated, FCF is a snapshot of how much cash a company is making once it’s paid the cost of maintaining and growing its business;

- A payout ratio of 50% or less. The payout ratio is the percentage of FCF that went out the door as dividends in the last 12 months. Real estate investment trusts (REITs) use a different measure called funds from operations (FFO) and can handle higher payout ratios, sometimes up to 90%;

- A healthy balance sheet, with ample cash on hand and reasonable debt.

Making DRIPs Obsolete

The best part is, these 19 investments are perfect for dividend reinvestment because each one gives us a dead-giveaway signal of when it’s time to buy, sit tight—or sell and look elsewhere for upside to go with our 7.5%+ income stream.

That makes DRIPs obsolete!

Because why would we mindlessly roll our dividend cash into a particular stock every quarter when, at a glance, we can pinpoint exactly where to strike for the biggest upside?

To show you what I mean, consider closed-end funds (CEFs), an overlooked corner of the market where dividends of 7.5% and up are common. We hold 11 CEFs in our Contrarian Income Report portfolio, mainly larger issues with market caps of $1 billion or higher.

(By the way, my colleague Michael Foster focuses 100% on CEFs in his CEF Insider service, where he keys in on funds with sub-$1-billion market caps trading at ridiculous discounts due to their obscurity. That sets you up for fast 20%+ upside and dividends up to 9.4%. You can check out a recent interview I did with Michael here.)

We don’t have to get into the weeds, but CEFs give off a crystal-clear signal that a big price rise is coming. You’ll find it in the discount to NAV, which is the percentage by which the fund’s market price trails the market value of all the assets in its portfolio.

This number is easy to spot and available on pretty well any fund screener.

This makes our plan simple: wait for the discount to sink below its normal level and make your move. Then keep rolling your dividend cash into that fund until its discount reverts to “normal.”

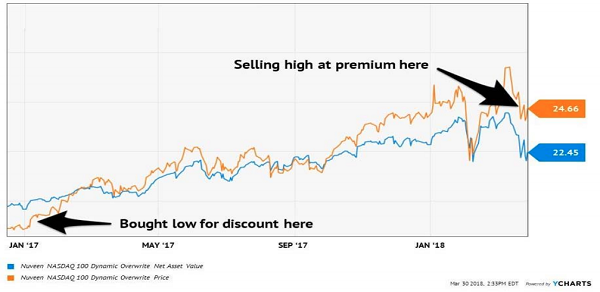

That’s exactly what we did with the Nuveen NASDAQ 100 Dynamic Overwrite Fund (QQQX) back in January 2017—and the results were breathtaking.

How We Bagged a 42% Total Return (With a 7.5% Yield) in 15 Months

QQQX is run by portfolio manager Keith Hembre, who cherry picks the best stocks on the NASDAQ, juices their high yields with a safe options strategy, then dishes distributions out to shareholders.

It’s hard to imagine now, after the huge run tech stocks have put in over the past couple years, but back in January 2017, QQQX was trading at a 6% discount to NAV and paid a 7.5% dividend.

That triggered our initial move into the fund. And over the next 15 months, we bagged two dividend increases and watched as QQQX’s discount swung to a massive premium—so much so that by the end of that period, the herd was ready to ante up $1.13 for every buck of assets in QQQX’s portfolio!

Discount Window Slams Shut…

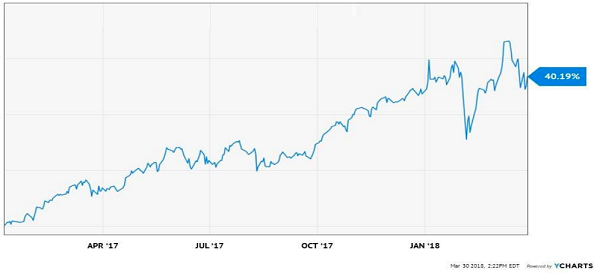

That huge swing from a discount to a premium catapulted us to a fat 42% gain (including dividends). But the fund’s outrageous premium meant its upside was pretty well maxed out by the time we took our money off the table on April 6, 2018.

… and Delivers a Fast 42% Gain

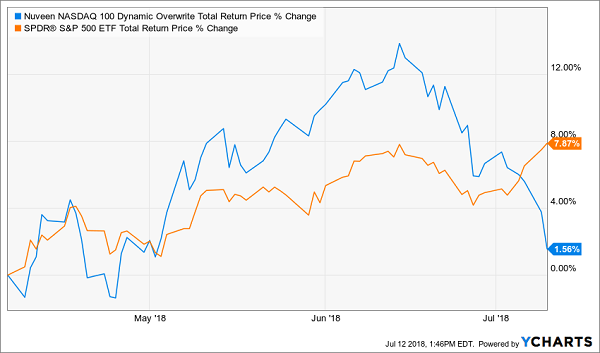

And what’s happened since?

QQQX has moved up slightly—a 1% gain. But that’s way behind the market, which has cruised to a 7.5% rise.

Premium Gives Us the Perfect Exit

Forget QQQX: Grab These 8% Monthly Dividends Instead

Luckily, the herd has cooled a bit on QQQX, but it still trades at a 5% premium to NAV. And why the heck would we overpay when the ridiculously inefficient CEF market is throwing us bargain after bargain as I write this?

And there’s one more thing I have to tell you: many of these cheap CEFs pay dividends monthly instead of quarterly.

So if you hold them in your retirement portfolio, their massive dividend payouts will roll in on exactly the same schedule as your monthly bills!

Convenience isn’t the only reason to love monthly payers, though. Because they also let you reinvest your payouts faster, amplifying your gains (and income stream) as you do.

I’m talking about an automatic “set-it-and-forget-it” CASH machine here!

The best news? You can kick-start your monthly income stream without doing a single moment of legwork … because I’ve done it all for you.

Beat the Trade War and Rising Rates With These 8% Payers

Allow me to introduce my new “8% Monthly Dividend Portfolio.” It’s a tightly built collection of REITs, CEFs and dividend-growth stocks I’ve personally assembled to protect and grow your portfolio, no matter what happens with the Federal Reserve or in DC.

And yes, as the name suggests, this portfolio also hands you a tidy 8% in dividend income, year in and year out.

So that $550k nest egg I told you about above will bring in $44,000 a year (and the yield on your initial buy will climb as each of the stout investments in my “8% Monthly Dividend Portfolio” hike their dividends).

And because these income studs pay dividends monthly, you can look forward to a steady $3,667 in income, month in and month out—give or take a couple hundred bucks.

I’d love to share the names of all my favorite monthly payers with you now. Simply click here and I’ll give you my full research on these monthly dividend all-stars—names ticker symbols, buy-under prices, the works. Don’t miss out!