Each June, the National Association of Real Estate Investment Trusts (NAREIT) hosts a conference that brings all of the key players in the sector together. For REIT investors, it’s the equivalent of the Super Bowl and it offers a window into who’s poised to perform well in the second half of the year and beyond.

This year, the focus in real estate remains about mergers and acquisitions, as small- and mid-range companies are combining to better compete with the larger players. Even the REITs that plan to go it alone for the time being are raising capital by selling non-core assets, with private equity and foreign capital bidding up prices.

Lodging and industrial continue to see strong tenant demand, while the outlook for retail remains volatile. Even so, individual pockets of strength can be found where you least expect it and here are three NAREIT winners that may have flown under the radar.

Front Yard Residential (RESI) rents out 12,000 affordable single-family homes in markets such as Atlanta, Memphis and Houston and believes that it can acquire another 3,000 properties without raising additional capital.

Improving Margins at Bargain Price

The company confirmed at NAREIT that it is in the process of improving its borrowing costs. At the beginning of the year 74% of its borrowings were floating rate and subject to rise along with the rest of the market. That figure is now down to 45%, which is the kind of leverage that management can use to exceed profit expectations.

Front Yard’s 5.6% dividend yield is attractive, but doesn’t stand out from the pack. What does pique my interest however, is that the stock is priced at a 40% discount to net asset value (NAV). NAV often helps to serve as a floor for a company’s valuation, especially when the business appears to be stable and potentially growing.

Sabra Health Care (SBRA) operates senior and assisted living centers and confirmed at NAREIT that M&A will continue to be important to its future strategy. The company undertook a multi-billion dollar merger in 2017 and has since been pruning assets to assist in combining the businesses. In the second quarter, management also retired all of the preferred stock outstanding for $144 million.

Breathing Life into Merger

Sabra may be wheeling and dealing with its real estate portfolio, but has a stable balance sheet and sports a solid 8.1% dividend yield. The healthcare side of the REIT business tends to offer more stable returns and has attractive demographic trends with the Baby Boomers aging. The company has guided to adjusted funds from operations (AFFO) of $2.27 to $2.35 a share in 2018, which is sufficient to cover the quarterly dividend of $0.45.

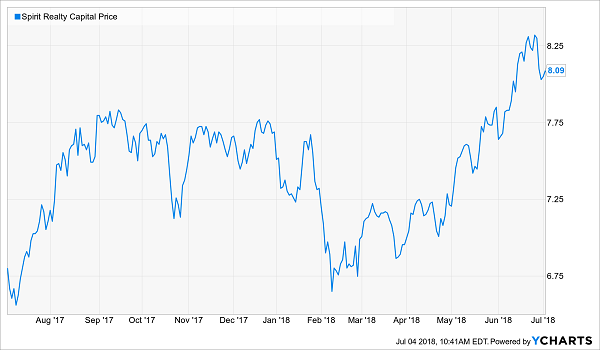

Spirit Realty Capital (SRC) is a net-lease operator, which means that its retail, office and industrial tenants pay for updates and maintenance. It’s been a volatile year for the stock, which has gained 10% and still offers an attractive 8.9% dividend yield.

Follow the Buyback Trend

NAREIT was notable for the company, as it recently spun off the locations of its largest customer Shopko and some asset-backed securities into Spirit MTA (SMTA). The deal involved 40% of Spirit’s properties, but only accounted for 10% to 15% of FFO.

The spin also raised significant cash that management is likely to use in an already active share buyback program. Now that the company has removed underperforming assets from its books and should see a profit boost, the rest of the market may also see value in the stock.

These three REITs may have shined in the big game this year, but they currently pay static dividends.

If, however, you’re nearing retirement, or have already retired and are living off income from your investments, I strongly encourage you to check out the top 7 REITs from Brett Owens, Contrarian Outlook’s Chief Investment Strategist. All seven are key recommendations in his 8% No Withdrawal Portfolio and check both boxes for “dividend growth” and “high current yield”.

As a group, they pay an impressive 8.5% average yield today, which is downright outstanding in a 3% world.

Combine 5% to 10%+ dividend growth with these high-single-digit current yields, and we have a formula for safe 15% to 20%+ annual gains from REITs, with a significant portion of that coming as cash dividends.

And thanks to the new tax plan, there’s never been a better time to buy REITs and live off their dividends.

(REIT investors will benefit from the tax breaks that “pass through” businesses will receive in the new code. Investors will be allowed deduct 20% of their REIT dividend income, which means the 37% tax bill will drop to 29.6%.)

But it’s important to choose your REITs wisely.

Don’t buy a low-yielding static payer. Don’t buy a retail REIT, either (with that entire industry in a death spiral, future rent checks will be dicey for years to come).

Instead, focus on recession-proof firms, such as those that rent hospitals, business lodging and warehouses filled with Amazon packages. Landlords that own properties that will be in high demand no matter what happens to interest rates or the economy from here, in other words.

We’d love to share Brett’s seven favorite recession-and-rate-proof REITs with you – including specific stock names, tickers and buy prices. Click here and I’ll send my full 8% No Withdrawal Portfolio research you to right now.