It’s something I hear from readers all the time: “Brett, the 7%+ dividends you recommend in the Contrarian Income Report service are well and good, but are dividends that high really safe to invest in? I’m worried about a dividend cut.”

The answer?

They are absolutely safe—so go ahead and enjoy the outsized cash payouts delivered by our Contrarian Income Report selections, which I’ve carefully chosen and safety-checked to let you retire on a $500k nest egg (and maybe even less).

And for stocks outside of our portfolio, you just need to take a few quick steps to stay off the rocks.

I’ll show you 3 time-tested dividend-safety tips today. Plus I’ll name 4 deadly dividend payers you need to sell now (or avoid if you don’t already own them) as we move through this article.

So let’s get going, starting with…

Dividend-Safety Tip No. 1: Mind the (Correct) Payout Ratio

The payout ratio is the first stop many folks make when checking out a dividend stock, and it should be a slam dunk: it’s simply the percentage of net income a company has paid out as dividends in the last 12 months.

So if that percentage is below, say, 50%, you’re good, right?

Well, not exactly. Because way too many people are looking at the wrong payout ratio!

That’s because the net income half of the ratio is an accounting creation that can be manipulated and often has little relation to the actual cash the firm is making. To get the real story, we need to look at the free cash flow (FCF) payout ratio.

FCF is a snapshot of how much cash a company is generating once it’s paid the cost of maintaining and growing its business. You calculate it by subtracting capital expenditures from cash flow from operating activities (you can find both figures under the “Financials” tab on Yahoo Finance).

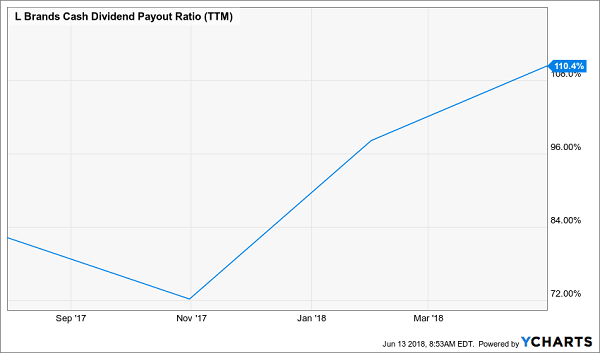

Which brings me to the first dividend that’s undoubtedly on the chopping block right now: the sky-high 6.6% payout at L Brands (LB), owner of Victoria’s Secret.

If you own LB, you’re already sitting on a 32% loss in the past year, while the rest of the market has gained 15%. That’s tough enough to take, but it gets worse: the lingerie peddler’s payout is on borrowed time—and when it goes, it’s going to catch the herd completely off guard, pummeling the stock again.

That’s because all those folks following the net income–based payout have no idea! Sure, LB pays out 73% of profits as dividends. That’s high, but not necessarily a sign of a looming cut on its own.

But the FCF payout ratio tells a far different story:

Key Indicator Flips From Yellow to Red

Over the last few months, LB has gone from paying a high-but-manageable portion of FCF as dividends to paying out more in dividends than it earns in FCF. It’s a subtle shift that 99% of the herd has sleepwalked right by … and a blaring sign that if you hold this stock, you need to sell yesterday.

Dividend-Safety Tip No. 2: Backstop Your Payouts With Rising FCF

Even if you’ve found a stock with a reasonable FCF payout ratio, you’ll want to make sure the underlying free cash flow is stable—or better yet rising—so the payout ratio doesn’t float up into the danger zone, like LB’s has.

Because the truth is, just a few quarters of soft FCF can tip the balance fast—and tighten the vice on the dividend before you even realize it.

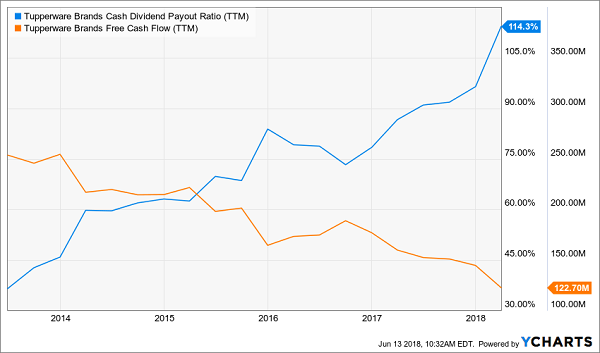

Case in point: Tupperware Brands (TUP), which, like LB, had a high but still relatively manageable payout ratio—73% as of the end of the third quarter of 2016. Too bad FCF has fallen through the floor since, putting the dividend in big trouble:

Noose Tightens on TUP’s Payout

So don’t be fooled by TUP’s 6.2% dividend yield. With slumping sales and FCF, this payout’s headed straight for the waste bin.

Dividend-Safety Tip No. 3: Be Careful With Stock Screeners

You can save yourself a lot of work by going with a dividend-safety screen like DIVCON, one of my go-to tools for dividend-stock research.

DIVCON uses a five-tier rating system that provides a snapshot of dividend health for individual companies. It’s offered as a free resource by ETF shop Reality Shares. (You can access DIVCON’s scores for free right here.)

The test combines and weights seven factors (including cash flow, earnings growth and dividend history) to provide a snapshot of a company’s dividend health.

DIVCON 5 is the best bucket. It means the dividend is in good shape, and there’s a very good chance it’ll be increased in the next year.

DIVCON 1 is the danger zone. It means the dividend is more likely to be cut than raised in the next 12 months. Current “DIVCON 1s” include two additional dangerous dividends I’ve been warning you about for a while and am doing so again today: 10.5%-paying Prospect Capital (PSEC), which I last covered in May, and CenturyLink (CTL), whose thin-ice 12.0% payout I sounded the alarm on (again) in early June.

But before you dive into a screening tool like DIVCON, keep in mind that for real estate investment trusts (REITs), net income and FCF aren’t the best measures of performance (and dividend safety).

For that, you need to look at funds from operations (FFO), a metric some screeners simply aren’t set up to deal with, causing them to flag REIT dividends as risky when they’re actually safe (or vice versa). And some screeners, like DIVCON, may offer little—if any—REIT coverage at all.

That just means you have to check REIT dividend safety “the old-fashioned way,” by doing a quick dive into the last four quarterly earnings reports and paying particular attention to FFO.

Here’s a Growing 4.9% Payout You Could Easily Miss

Consider Summit Hotel Properties (INN), payer of a 4.9% dividend and a REIT I tapped for its high yield and fast dividend growth in a May 8 article.

Going by the net income– and FCF-based payout ratios you’ll find on a screener like Ycharts, you’d think its dividend is headed for a haircut—after all, it appears to be paying a dividend while generating negative FCF!

2 Misleading Dividend-Safety Indicators

Source: Ycharts.com

But if you take a quick look back through Summit’s last four quarterly earnings reports, you’ll find a far different story: it posted adjusted FFO of $1.32 a share in all, while paying out just $0.69 in dividends.

The resulting 52% payout ratio is among the lowest you’ll find in the REIT space—and a rock-solid indicator that this payout is safe and set to grow.

My Favorite 7.7% Dividend Payer Is Cheap—But Not for Long

My top REIT pick for 2018 boasts a higher dividend than Summit Hotel Properties—I’m talking about an eye-popping 7.7% cash payout.

What’s more, this outsized dividend is as safe as they come—and poised to grow as interest rates head higher, as I’ll explain in a moment.

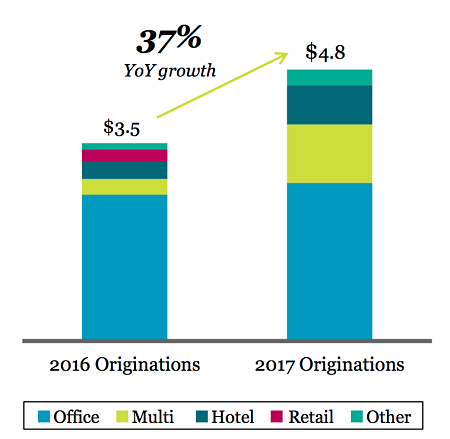

This company is a well-connected commercial real-estate lender that does all the work for us—building a secure, diversified loan portfolio featuring offices, retail space, hotels and multi-family units.

Management then collects the monthly rent checks, deposits them and sends most of the profits our way as dividends!

This REIT’s mammoth 7.7% payout is easily covered by FFO, and its loan growth is soaring, setting us up for massive dividend hikes, too!

Big Loan Growth Today, Big Payout Growth Tomorrow

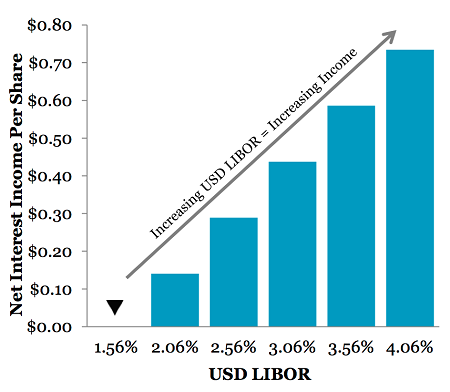

Plus if you’re worried about rising rates, this is the stock for you: management has smartly eliminated interest-rate risk by using floating-rate loans. In fact, it’s actually set up to make more money as interest rates move higher!

More Income as Rates Rise

And as its income—and dividend—march higher, they’ll haul the share price right up along with them.

That’s why I’ve made this unsung REIT a cornerstone of my “8% No-Withdrawal” portfolio, a collection of 6 investments from every corner of the market that I’ve assembled to do two things:

- Deliver a safe 8% average dividend, enough to pay you $40,000 in income—enough for many folks to retire—on a $500k nest egg.

- Safeguard your retirement stash, letting you fund your golden years on dividends alone without drawing down your nest egg! This insures your retirement against a market meltdown and lets you leave a lasting legacy for your kids (and grandkids).

I’m ready to share the names of all 6 stocks and funds inside this dynamic portfolio with you now. Click here to get the name, ticker symbol and full details on my top REIT pick and all 6 of these my top high-yield buys.