Most investors with $500,000 in their portfolios think they don’t have enough money to retire on.

They do – they just need to do two things with their “buy and hope” portfolios to turn them into $3,333 monthly income streams:

- Sell everything – including the 2%, 3% and even 4% payers that simply don’t yield enough to matter. And,

- Buy my 8 favorite monthly dividend payers.

The result? $3,333 in monthly income every month (from an average 8% annual yield, paid every 30 days). With upside on your initial $500,000 to boot!

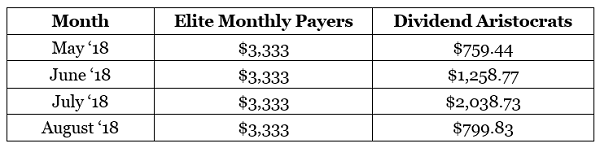

Traditional dividend stocks simply can’t keep up. Let’s take a 4-pack of popular dividend aristocrats to map how much they’ll pay investors through summer. They simply can’t keep up with my monthly machines:

Consistent Monthly Payouts

“But… but… you’re forgetting dividend growth!” I can hear the aristocrat fanboys stammering now.

I’m not forgetting growth. First, I accounted for likely dividend hikes for two of these aristocrats.

Secondly, and more importantly – when executed correctly, this strategy actually captures more upside than “America’s best blue chips.” I know this because since inception, my Contrarian Income Report readers have enjoyed current yields of 6%, 7% and even 8% or higher.

With most of these payouts being paid every single month.

And this strategy isn’t capped at $500,000. If you’ve saved a million (or even two), you can just buy more of my elite eight monthly payers and boost your passive income to $6,666 or even $13,332 per month.

Though if you’re a billionaire, sorry, you are out of luck. These Goldilocks payers won’t be able to absorb all of your cash. With total market caps around $1 billion or $2 billion, these vehicles are too small for institutional money.

Which is perfect for humble contrarians like you and me. This ceiling has created inefficiencies that we can take advantage of. After all, in a completely efficient market, we’d have to make a choice between dividends and upside. Here, though, we get both.

A Sample Monthly-Paying 4-Pack for Yields Up to 12.3%

Main Street Capital (MAIN) is a business development company (BDC) that pays its 5.8% yearly yield in monthly installments. It provides capital to lower-middle-market companies, and also provides debt to middle-market companies. And as I discussed earlier this year, it has been one of the best BDCs on Wall Street for years.

Main Street Capital (MAIN) Clobbers the Competition

Back in January, I told investors that they were better off waiting for a discount in MAIN. That’s because:

The company announced Jan. 3 that Vince Foster will be stepping down as CEO to executive chairman while COO and President Dwayne L. Hyzak takes over the chief’s role – a transition that’s expected to take place in Q4 2018. The news sent the stock down by more than 4% in a week, which doesn’t sound drastic, but is one of the company’s worst such quick moves in the past couple years.

While Hyzak clearly knows Main Street through and through, and Foster still will be providing some input from his executive chairman position, the BDC very well could end up missing Foster in the daily operation of the company.

That, plus a share price that stood at 166% of net asset value, made MAIN too richly priced for my blood. Investors did get a small dip in February along with the rest of the market, but that’s gone, and MAIN is back to trading at a similar premium.

Those sales on Main Street Capital never seem to last for long!

Prospect Capital Corporation (PSEC) is a fellow business development company. It pays more than twice Main’s payout at 12.3%. Problem is, its yield is so high because this stock is “cheap for good reason.”

This BDC is structured to give out most of its income to shareholders, but that’s exactly why it’s frequently in dividend trouble. The company most recently announced a 28% payout cut in August 2017, and it’s been in “recovery mode” ever since.

BDCs have very few “business moats” – cutting checks isn’t rocket science. For years Prospect has been average at best, and competition is taking its toll. The firm just reported its results for the quarter ended March 31, and net interest income declined 4% year-over-year to $70.4 million, while net assets trickled down from $9.43 per share to $9.23.

Moving along, BlackRock Municipal Income Fund (BFK) is the rare municipal bond fund that pays a generous 5.5%. (Contrast it with the iShares National Muni Bond ETF (MUB), which is the largest such fund at nearly $9 billion in assets, paying a paltry yield of just 2.4%.)

BFK isn’t an exchange-traded fund, of course – it’s a closed-end fund, which allows it to use the kind of leverage necessary to squeeze that kind of yield out of munis. But BFK’s high yield isn’t solely an effect of high leverage.

BlackRock Municipal focuses on the far end of the maturity spectrum. At the moment, roughly 55% of the fund is invested in bonds with remaining maturities of 15 to 30 years, with more than 20% of the total falling in the quarter-century-plus area. While the long maturities might be a cause for worry, BFK balances that out with excellent credit quality. The fund is about two-thirds-weighted in bonds with an A rating or higher, and another 20% is BBB – still investment-grade.

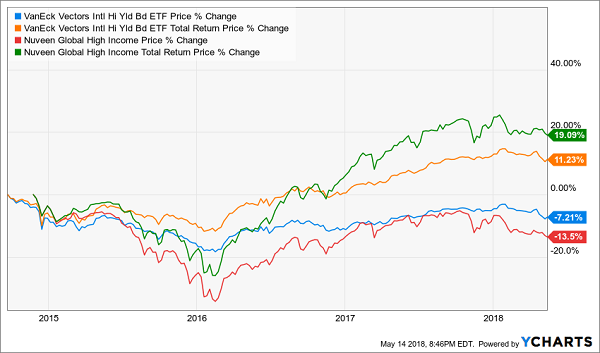

Finally let’s wrap our monthly coverage with the VanEck Vectors International High Yield Bond ETF (IHY), paying 5.6%.

It’s another way to get both high yield and diversification in your bond portfolio is to seek out high-yield junk abroad. Global bonds, Van Eck says, “have had low or negative correlation to other bond asset classes” – in other words, they’ll help you zig when most bonds are zagging.

And funds like the VanEck Vectors International High Yield Bond ETF (IHY) help you tap that diversification for a relatively low annual fee of 0.4% while bringing in more than 5% in annual income.

The IHY invests in a portfolio of 540 bonds spread across a couple dozen countries, including large weightings in U.K. (11%) and Brazilian (10%) debt. Two-thirds of the portfolio is in the highest junk rating (BB), while most of the rest is in B-rated bonds. The maturity is on the short end, too, with more than 80% of the fund invested in debt maturing in one to seven years.

However, the IHY has a problem that many low-cost ETFs share: It’s inferior to closed-end funds. The Nuveen Global High Income (JGH), for instance, while hardly a dynamo, has clobbered the modest returns of the IHY over the past five years. And it also pays monthly.

Fortunately we’re not constrained to IHY’s “lightly funded” payouts. Here are 8 better monthly dividend payers that are best buys today.

The Best Monthly Payers to Buy Today: Floating Rate Bond Funds & More

My favorite monthly payer today is a rate-proof bond fund that yields 5.1% annually. It tends to deliver total returns between 10% and 15% yearly when the Fed is raising interest rates (as it is right now).

It’s one of 12 monthly payers in my “8% Monthly Payer Portfolio”. With just $500,000 invested, it’ll hand you a rock-solid $40,000-a-year income stream. That’s an 8% dividend yield … and it’s easily enough for most folks to retire on.

The best part is you won’t have to go back to “lumpy” quarterly payouts to do it! Of the 19 income studs in this unique portfolio, 12 pay dividends monthly, so you can look forward to the steady drip of $3,333 in income, month in and month out—give or take a couple hundred bucks – on every $500K in capital you’re able to invest.

I’d love to share my 8 favorite monthly payers with you today, along with the name, ticker, and buy price for this floating rate bargain. Click here to get a full copy of my research on Monthly Dividend Superstars: 8% Annual Yields with 10% Price Upside, Too