Have you always wanted to buy a safe stock like Coca-Cola (KO) and get rich from it like Warren Buffett?

It’s doable. But most investors “live in the past” and fixate on dividend track records rather than a payout’s forward prospects. And looking ahead is the key to yearly gains of 10%, 15% or even 20% or more with dividend aristocrats.

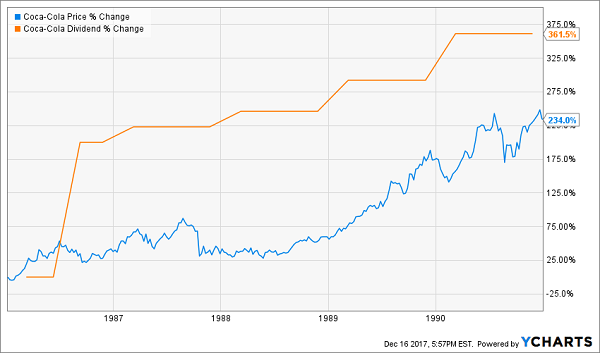

Let’s look at Coke, which achieved its dividend royalty status in 1987 (its 25th straight year with a dividend hike). The firm hit its coronation with a head of steam, rewarding investors with a 362% payout hike in just five years (from 1986 to 1991). Its stock price raced to keep up with its dividend, rising 234% over the same time period:

Great Dividend Growth, Great Returns

It didn’t really matter if you bought shares before or after the company was officially a dividend aristocrat. The driving factor for profits was the dividend’s velocity – it was moving higher quickly, so its stock price followed.

Fast forward to the last five years, and we see that Coke’s youthful exuberance has slowed considerably. The firm still hikes its payout every year, but it’s a slower climb – totaling 45% over the past five years. Which means its stock price merely plods along too (+25% in five years):

Average Dividend Growth, Average Returns

Why is Coke’s dividend slowing down? Simple – just look at the top line.

Shrinking Business is Bad for Payouts

It sounds obvious, but income investors often wade so deep into the dividend weeds that they ignore obvious cues – such as shrinking sales.

Let’s add Coke’s top line into the last chart, and we’ll see that the fact that the payout is growing at all is an act of financial wizardry:

Shrinking Sales Slow the Dividend

Coke’s top line has shrunk by 22% over the last five years. Which makes its dividend growth quite the feat!

Contrast this with the 1986 to 1991 period, when the company was younger and still growing. It boosted its sales by 30% over that time period.

Of course it’s possible to grow payouts faster than profits and sales. In fact, this is what often happens with dividend payers. But even the most gifted managers can only squeeze so much in payouts from a shrinking pie. It’s better to focus on businesses with the winds at their backs.

And That Can Include Spry Aristocrats, Too

In a minute, we’ll discuss five Dividend Aristocrats that have years and even decades of profitable runway ahead.

Coke’s future business prospects don’t pass my taste test. Consumers are turning away from its core product of sugary beverages. The company knows this, and is expanding into other segments such as health and energy beverages – but it’s forced to pay up for hot products.

(Which is why I’m actually worried that Coke could be the next GE. It’s following a similar problematic path – a pricey acquisition binge to patch its leaky sales bucket.)

We’re better off focusing on companies that are generating sales and profit growth organically. From there, we choose the firms that are financially fit enough to dish an increasing amount of their profits back to their shareholders every year.

That’s how you buy the best dividend aristocrats, those that will keep their titles for years and even decades ahead. Here’s a five-pack with well-positioned businesses for 2018, 2028 and 2038 and beyond.

Medtronic (MDT)

Dividend Yield: 2.2%

Medtronic (MDT) is a medical device company that has its hands in numerous areas. About 35% of its revenues come from its cardiac and vascular group, a third from minimally invasive therapies, a quarter from restorative therapies and the remaining 6% from its diabetes group.

At the ground level, that means Medtronic makes devices such as insulin pumps, aortic stents, heart valves, electrosurgical instruments, tracheostomy tubes and surgical imaging systems.

The view from 10,000 feet is incredible. Healthcare costs have been rocketing unchecked seemingly forever, and the aging of the baby boomers is only helping to drive up demand for these life-lengthening products. These trends aren’t stopping anytime soon, with healthcare costs expected to climb 5.5% annually between 2017 and 2026, when they’re expected to reach $5.7 trillion.

The company’s most recent quarterly report exemplifies Medtronic’s continued growth, including a 10% top-line boost from its cardiac and vascular products. Net sales overall were a little slow, growing 1.2% to $7.4 billion, but they did beat estimates. More importantly, analysts expect the bottom line to grow in the high single digits for at least the next five years.

MDT also is generously expanding its dividend, which has grown by 64% since 2014. The company’s projected profit growth, as well as a payout ratio of about 39% of this year’s expected profits, means Medtronic should have plenty of ability to improve its dividend in the years and even decades ahead.

Becton, Dickinson and Company (BDX)

Dividend Yield: 1.3%

Becton, Dickinson (BDX) is another medical device company that, like Medtronic, spans numerous healthcare needs. Becton’s product lineup covers areas ranging from anesthesia delivery, diabetes care and cervical cancer screening to infection protection, molecular diagnostics and specimen collection.

It’s also one of the few companies that can actually claim to have swallowed up a fellow Dividend Aristocrat.

Near the end of 2017, Becton, Dickinson completed the acquisition of C.R. Bard, itself a medical-tech company that specialized in vascular, surgical and oncology products, among others. The deal is expected to “generate low-single digit accretion to adjusted earnings per share in fiscal year 2018, and high-single digit accretion in fiscal year 2019.”

As a result, Wall Street is high on Becton, Dickinson’s prospects for the years ahead. Analysts project average annual earnings growth of 14% for the next half-decade, including a 16% bump in 2018.

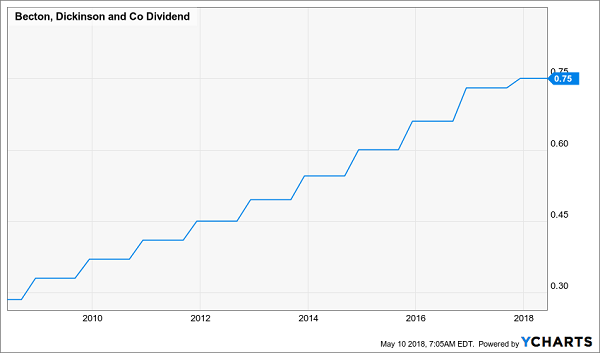

Meanwhile, BDX should extend its 46-year dividend growth streak sometime later this year. Since 2014, the payout has plumped up by a healthy 38%, and there’s ample room to continue considering a meager 27% payout ratio based on 2018’s projected profits.

Becton, Dickinson (BDX): A Healthy Health Care Dividend Raiser

Praxair (PX)

Dividend Yield: 2.1%

Praxair (PX) is proof of the concept that “boring is beautiful.”

This is an industrial gases company that produces carbon dioxide, argon and oxygen, among other common gases, not to mention other specialty gases, mixtures and even handling equipment. In fact, Praxair even goes a step further by providing whole management-and-delivery systems, doing everything from cleaning to leak detection to inspection.

The beauty of Praxair is that industrial gases tend to be critical to operations but also a small portion of costs. Meanwhile, the company deals in contracts that are up to 20 years in length, meaning that it has some extremely established customers it can rely on to keep driving cash flow.

At the moment, Praxair is working on asset sales to facilitate its planned merger with German chemical giant Linde Group AG. The marriage should create $1.2 billion in annual cost and capex synergies and efficiencies.

PX is a newcomer to the Aristocrats, joining Roper Technologies (ROP) and A.O. Smith (AOS) in 2018 after notching its 25th consecutive year of dividend hikes. Expect it to keep up its membership well into the future, with analysts expecting double-digit annual profit growth for the next five years at a minimum.

3M (MMM)

Dividend Yield: 1.9%

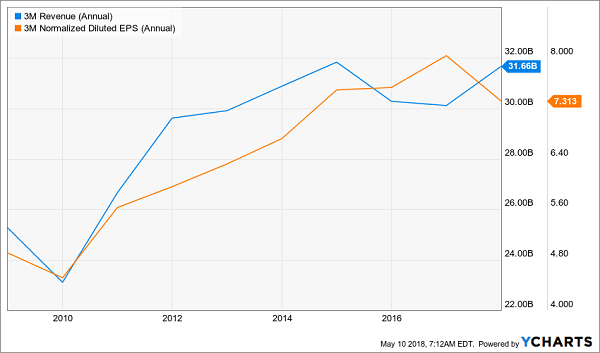

Yes, I’m well-aware that 3M (MMM) doesn’t exactly look like its sterling self right now. After all, the name behind Post-it Notes, Scotch Tape, Thinsulate and Nexcare healthcare products is coming off a rough first-quarter earnings report in which it guided both its full-year organic growth rate and profits lower.

But take heart.

3M shares are now off nearly 14% in 2018 – one of the largest pullbacks in MMM in years. That gives investors the chance to jump into one of the most successful industrial companies on the planet for … well, at just less than times forward earnings, not exactly a bargain, but a more reasonable price than investors have been offered for some time.

3M (MMM) Hits a Bump in the Road – Not a Mountain

3M, after all, offers more than 55,000 products that cover everything from adhesives to dental implements to fire protection to car care. 3M generally benefits from a growing global economy, and its outstanding product diversification means that if one area slumps, there are dozens of other categories there to pick up the slack.

Despite the Q1 warning, analysts still are expecting 9%-plus annual profit growth on average for the next five years. Meanwhile, MMM just celebrated its 60th consecutive dividend increase – a 16% improvement that keeps 3M among the ranks of the longest-serving Dividend Aristocrats.

Ecolab (ECL)

Dividend Yield: 1.1%

Ecolab (ECL) is one of the “quiet” Dividend Aristocrats, serving boring but vital functions while mostly keeping out of the public eye. But while most consumers haven’t heard of Ecolab, they’ve certainly benefited from its products.

ECL is responsible for keeping the power on, keeping the water flowing and keeping everything you come in contact with clean.

Ecolab’s Nalco Water division provides water treatment technologies for large-scale industries such as refining and petrochemicals. This helps companies save money by conserving water and energy, plus keeps them in line with ever-changing environmental regulations, but also helping them save money by conserving water and energy. Ecolab also dabbles in everything from kitchen equipment repair to dishwashing solutions to pool and spa maintenance, for customers ranging from businesses to schools to government organizations.

Ecolab generates more than $1 billion in free cash flow every year, and the company is modeling as much as 16% earnings growth next year, while analysts are looking for a 15% pop. In fact, they’re pretty bullish on the company’s prospects even further into the future, with Wall Street’s pros looking for 13% annual bottom-line growth from now through 2023.

That, as well as a conservative 30% payout ratio, should keep the dividend hikes going well past Ecolab’s 26-year increase streak.

How to Retire on 8% Dividends Paid EVERY MONTH

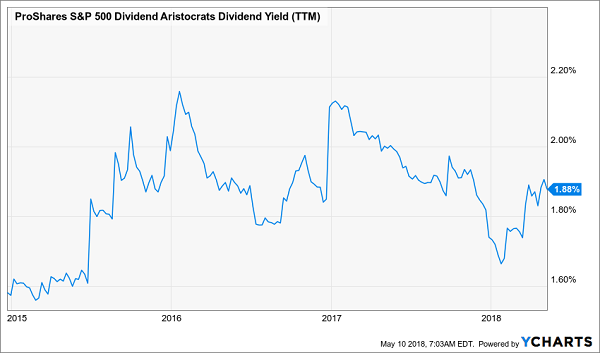

Dividend Aristocrats like 3M and Ecolab are impressive dividend growers, but a portfolio too reliant on Aristocrats will leave your retirement portfolio in haggard shape. In fact, with an average yield of less than 2%, the Aristocrats deliver less income than the 10-year T-note!

However, I have a portfolio of dividend winners that not only will pay you 4 times more, but will pay you 3 times more often.

When you retire, chances are you’ll be relying heavily on dividend income to get you through your regular expenses: the house, the car, power … you name it. But while most publicly traded companies tend to pay dividends out quarterly, your bills sure aren’t quarterly. They come every single month, rain or shine.

That’s why monthly dividend stocks make so much sense for long-term retirement planners. A reliable stream of income that doesn’t vary from month to month allows you to budget with precision. And with the right plan, you can collect $3,000-plus in dividends every single month – and do it with a smaller nest egg than even the suits at Merrill Lynch say you need to retire well.

My “8% Monthly Payer Portfolio” checks off every box investors need from retirement:

- Monthly income to use against your monthly bills.

- Dividends large enough to allow you to live off investment income entirely. That means no selling your stocks and shrinking your nest egg, which ultimately shrinks your regular dividend paycheck.

- Better returns on any dividends you choose to reinvest. If you don’t need the income from your portfolio right away, you don’t have to wait every three months to put dividends to work – you can sink them back into new investments just about every 30 days!

These monthly dividend payers include a few picks that have remained mostly under the radar despite their high payouts and general quality. For instance, this portfolio includes an 8.7% payer trading at a bizarre 5.3% discount to NAV, and a steady Eddy high-yielder that barely blinks when stocks plummet.

Because these big dividends compound quicker, they’ll turbocharge your net worth and allow you to enjoy the retirement you’ve worked so dearly to reach. Don’t delay! Click here and I’ll send you my exclusive report, Monthly Dividend Superstars: 8% Yields with 10% Upside, for absolutely FREE.