If you’re a retiree, or a near-retiree, you’ve probably been told you should dump—or at least reduce—your stock holdings and focus on fixed-income investments.

It sounds like a smart move, right? After all, CDs, Treasuries and the like protect your principal, while one big downturn can wipe out your stock-market gains.

But going lean on stocks leaves you open to two big risks: that you’ll outlive your savings and miss out on the long-term gains only the stock market can offer.

Consider these numbers from the Society of Actuaries: if you’re a 65-year-old man, you have a 41% chance of living to 85 and 20% odds of hitting 90. If you’re a woman of the same age, your chances jump to 53% that you’ll make 85 and 32% for 90.

But here’s the part most retirees overlook: if you’re married, the odds one of you will still be around at 85 take a big leap—to 72%.

That’s the lifespan side of the equation. Here’s the investment side: according to Oppenheimer, the S&P 500 notched an average annual return of 7.2% over any 20-year holding period from 1950 to 2010 (measured in rolling monthly periods). Try getting that kind of performance out of a Treasury or a CD.

You can slash your risk further by picking stocks with high yields, reasonable payout ratios (or the percentage of earnings paid out as dividends) and—a Warren Buffett favorite—economic moats, or advantages that are tough for competitors to match.

Here are two that fit the bill.

Take a Swim in 3M’s Moat

At first blush, 3M Co. (MMM) doesn’t look like a retirement stock. It’s an industrial firm, and most investors know that industrials are among the first—along with resource and consumer-discretionary stocks—to dive when the economy dips.

That’s true, but 3M has loads of advantages that make pole-vaulting over its moat a tall order. They include $1.4 billion of patents, technology and top-notch brands, like Scotch-Brite, Scotchguard and Thinsulate.

The company also poured $1.76 billion, or 5.8% of its sales, into R&D in 2015 and can use its huge size to wring better prices out of its suppliers.

To those strengths, I’d add a product portfolio that’s as diverse as they come: a quick glance at 3M’s website reveals that it sells 19,180 items in the US alone, spread over 12 categories ranging from automotive to healthcare.

Finally, 3M knows how to keep a lid on costs: even though the anemic global economy and high-flying greenback held back its Q4 sales and profits, it managed to eke out a 0.6% expansion of its operating margin, excluding restructuring charges.

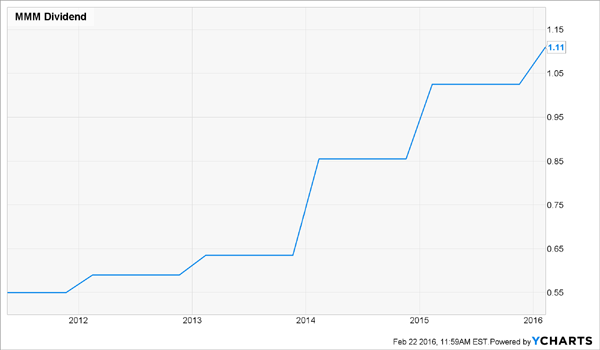

And in one crucial way, this is your grandparents’ 3M: dividends. The company has paid a dividend for 98 straight years and has hiked its payout for the last 57, easily nailing down a spot on the S&P Dividend Aristocrats list, whose members have boosted their payouts for at least 25 consecutive years.

There’s room for more hikes, too, thanks to 3M’s modest 53% payout ratio. The shares yield an above-average 2.8%.

Right now, 3M trades at 17.4 times its expected 2016 earnings. That’s higher than both its five-year average forward P/E of 15.9 and the S&P 500, at 15.8. But with its heavy R&D spend, take-it-to-the-bank dividend hikes and buybacks (3M slashed its share count by 15% over the past five years, and its board just signed off on a new $10-billion repurchase plan), it’s a price worth paying.

JNJ: A Prescription for a Happy Retirement

I called out Johnson & Johnson (JNJ) as one of my top stocks to buy now and hold forever a little more than a month ago. If you followed that advice, you’d be sitting on a nice 7.6% gain already.

But if you missed out, don’t worry. The stock has plenty of room to run, especially if your time frame is long—say, the 20 years between your 65th and 85th birthday.

One thing that makes JNJ a retirement standout is its low volatility. It boasts a beta rating of 0.62, meaning it has historically been 38% less volatile than the S&P 500 as a whole. That means it doesn’t usually shoot as high as the average stock when the market’s on fire, but it won’t plunge as far when the market craters, either.

You can see that in action over the past year:

That’s partly a function of the company’s broad business. Like 3M, its products are everywhere and include medicine-cabinet staples like Neutrogena skin cream, Visine eye drops and Tylenol pain relievers.

But its offerings go much further. Aside from consumer goods (19% of 2015 revenue), Johnson & Johnson makes pharmaceuticals (45%) and medical devices (36%).

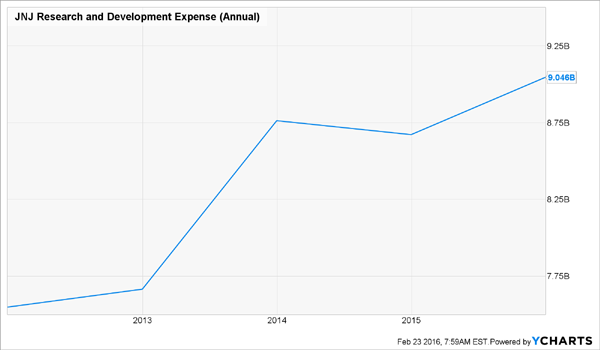

Like 3M, JNJ puts a huge emphasis on R&D, to the tune of $9.05 billion, or 12% of sales, in 2015. That’s translating directly into fast-selling new drugs: since 2009, it has released 14 with sales of $1 billion or more, and RBC Capital Markets is calling for 10 new $1-billion-plus sellers in the next three years alone.

On the dividend front, JNJ easily earns a spot among the Dividend Aristocrats, with 53 straight years of payout hikes. The shares yield 2.9%, well ahead of the average S&P 500 stock, and the company pays out 54.8% of its earnings as dividends, so you can look forward to that payout rising throughout your golden years.

Meantime, JNJ trades at just 15.4 times its forecast 2016 earnings, a great deal considering its strong pipeline, rock-solid dividend and huge potential to gain as more baby boomers pass retirement age.

Johnson & Johnson is a great way to play the bull market in aging Americans, but it’s not the best way. That honor goes to three other stocks that are throwing off yields more than twice as big. I’m talking about payouts of 7.9%, 8.5% and 9.4%.

And when I say “bull market in aging Americans,” I’m not kidding around. This is hands-down the biggest demographic shift in US history—and the perfect way for you to grab the high, safe income you need to fund your own retirement.

Consider:

- There are 77 million baby boomers in the US who just started retiring.

- Roughly 10,000 of them will turn 65 every day for the next 17 years.

- We’re living longer than ever but will require more care as we get older.

- Healthcare spending in the US will increase to $5.3 trillion by 2024.

The best part? Most investors haven’t heard of my three top picks. That means you can not only collect yields north of 8%, but you’re positioned to grab 15-20% upside in the next 12 months as other investors pile into these reliable dividend-payers.

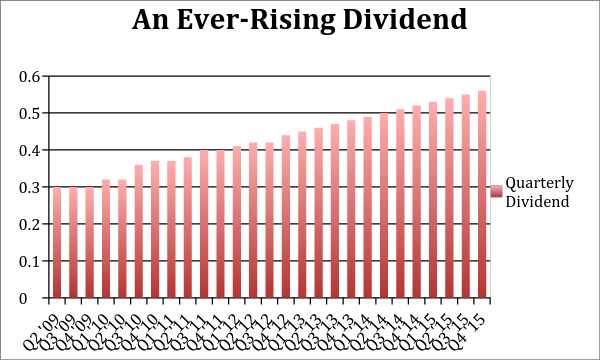

And all three are growing their dividends at a rapid clip. Check out the dividend growth in my favorite firm, which raises its payout every single quarter:

That’s why I’m urging my subscribers to lock in these juicy dividends today, while they’re still cheap. Click here to get the names of all three of these dream investments and discover how we’re playing this megatrend now.