Worried about President Trump? The Fed? China’s economy?

All of the above?

If so, here’s some simple advice – ignore it all, and invest only in “sure things.” You see, no matter what American voters, Janet Yellen, or Xi Jinping decide to do later this year, there’s one sure economic bet in the U.S…

The country will be a lot older in the future than it is right now – thanks to 10,000 Baby Boomers turning 65 every day. Remember how this generation drove the U.S. economy since their infancy in the 1950s?

- Post-WWII makers of baby products recorded record profits thanks to their wares flying off the shelves.

- Boomers fueled unprecedented economic growth in the 1980s as they powered the American workforce.

- And the suburbs expanded like crazy thanks to their home buying. Only one-quarter of Americans called the ‘burbs home beforehand, versus one-half by 2000.

This time around, the healthcare industry will benefit. The 65+ population will double and 85+ will triple in the coming years. And the longer we live, the more likely it is that we’ll need care. By 2024, national healthcare expenditures are projected to climb to $5.43 trillion, or about 20% of GDP.

Here are three firms set to capitalize on these trends, and dish increasing demographic-driven dividends to their shareholders. These stocks are good long-term buys no matter what happens between now and this November. All have 200% upside or better in the decade ahead.

CVS Health (CVS) runs America’s largest drugstore chain, a pharmacy-benefit-management business and 1,100 in-store medical clinics. E-commerce websites such as Amazon.com (AMZN) may be eating into traditional retail sales, but they’re not a threat when it comes to prescription drug fulfillment.

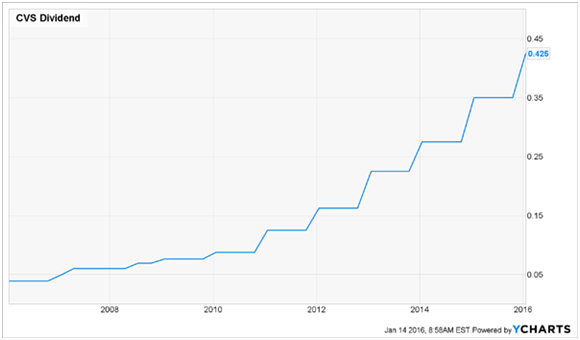

Business is booming at CVS, and the company generously shares its profits with shareholders. It’s raised its dividend by 9.9% annually, on average, over the past decade.

Accelerating Dividend Growth at CVS

Since 2007, CVS has also reduced its outstanding share count by 30%. These stock buybacks have created a virtuous cycle for shareholders, as fewer and fewer shares translate into accelerating earnings-per-share (EPS) and dividend growth.

By the end of this year, all of Target’s (TGT) 1,660 pharmacies will become CVS-branded facilities. Consumer advocates already worry that this acquisition, which consolidates competition, will lead to higher prices. It probably will – which is good news for CVS shareholders.

The stock yields 1.7% today. A modest 30% payout ratio provides some upside for continued dividend increases. Analysts are projecting double-digit earnings growth through 2019, making the stock’s price-to-earnings (P/E) ratio of 22 look quite reasonable.

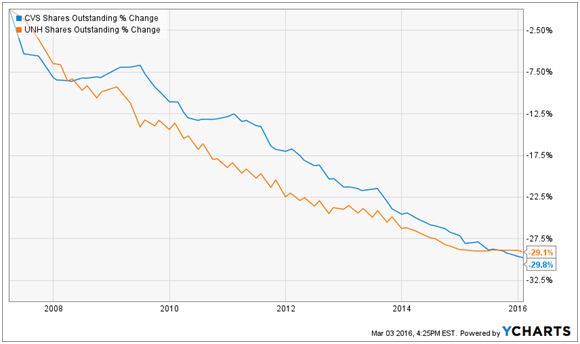

United Health (UNH), the largest health insurance carrier in the U.S., also treats its shareholders well. It’s tripled its dividend over the past decade, while buying back nearly as many shares as CVS since 2007:

CVS & UNH Buy Back 30% of Their Respective Companies

At a glance, UNH looks richly priced at 21-times earnings. But it trades at just 15-times free cash flow (FCF), a more accurate valuation measure because it reflects the actual cash profits a business pulls in. UNH’s dividend is a near-mirror image of CVS – a modest 1.6% with a conservative 31% payout ratio.

Earnings growth should help power higher payouts and more share repurchases. Analysts are also projecting double-digit earnings growth for UNH through 2019 – it’s a steal at 15-times FCF if that plays out.

Finally, leading healthcare landlord Ventas (VTR) owns 1,282 healthcare properties across the U.S. and Canada. This includes 786 senior housing communities, and 371 medical office buildings.

Ventas’ stock recently went on sale thanks to a bad 2016 outlook from competitor HCP (HCP). Investors dumped the entire sector, even though HCP’s results were isolated and due to nothing more than poor management. In fact, as you can see, Ventas has consistently outperformed HCP over the past decade:

Ventas Delivers All Decade Long

Ventas’ stock has pulled back 5% in total over the past 12 months. Prior to the HCP worries, investors fretted about the Fed raising rates. Then, China.

The Fed’s not an issue – Ventas returned 32% in two years during the last major rate hike cycle. And China’s not a meaningful driver, either – the Shanghai Composite Index inflated and popped twice while Ventas investors were collecting smooth 260% cumulative returns over the past 10 years.

Over the past five years, Ventas has grown its fund from operations (FFO) at a compounded rate of 10.9% annually. FFO is the REIT (real estate investment trust) equivalent of earnings, as it accounts properly for depreciation. Ventas’s FFO growth has powered 5-year dividend growth of 27%.

Ventas pays a 4.8% yield today. It’s not a bad buy here, but I prefer three smaller firms in its space with dividends that are 38-86% higher. They aren’t as well known as Ventas, and thanks to their relative obscurity, their stocks are cheaper.

This means their yields are higher, too. They pay 6.6%, 7%, and 8.9% to be specific.

Plus, these firms are raising their dividends every year – even faster than Ventas – and in one case, every single quarter. Which means, in just a few years, you’ll be earning a growing 10% yield on your initial investment.

The best time to buy these stocks is right now, before Wall Street uncovers these hidden gems and sends analysts their way. Click here, and I’ll give you the name and ticker for each one, along with my full analysis of each pick.