Fidelity Investments has a laundry list of highly rated mutual funds – so let’s delve into a quartet of funds that are top-tier choices for retirement investors. The recipe for retirement success includes safety, durability, income and cost-efficiency, among others – these four funds have these qualities in spades!

Fidelity Investments is the No. 2 player in the mutual fund world, boasting $1.7 trillion in total assets across its expansive lineup of offerings. Just like Vanguard – which also boasts a number of excellent retirement funds – most of Fidelity’s assets are long-term in nature.

Why is that important? Because it shows that while some of Fidelity’s funds can be used to make short-term plays, most of its mutual funds are buy-and-hold investments – in other words, exactly what you’re looking for if you’re planning out a retirement portfolio.

What really makes Fidelity stand out as an elite choice in the mutual fund world is its willingness to adapt. Fidelity was built upon the shoulders of active managers like Peter Lynch and Will Danoff, providing superior performance from the best brains in the business. But Fidelity hasn’t shied away from the growing trend toward index funds, either, and provides investors with some of the lowest-cost options available.

While I like several Fidelity funds for different investment purposes, I have my eye on four Fidelity mutual funds that hit the perfect notes for retirement. Also, several of these funds are available in corporate 401(k) plans.

Fidelity 500 Index Fund (FUSVX)

Type: Large-cap stock (index)

Expenses (FUSEX Investor Shares, Minimum Investment of $2,500): 0.09%

Expenses (FUSVX Premium Shares, Minimum Investment of $10,000): 0.045%

Yield: 2%

Selecting a large-cap stock fund from Fidelity is no easy task. That’s because Fidelity offers two of the most celebrated actively managed large-cap funds in the business: Fidelity Magellan (FMAGX), which Peter Lynch famously led to 29% annual returns during his tenure from 1997 and 1990, and Fidelity Contrafund (FCNTX), where William Danoff has targeted underappreciated value and growth stocks alike since 1990.

You won’t go wrong with either actively managed fund. But it’s difficult to argue with Fidelity 500 Index Fund (FUSVX), whose Premium shares not only offer the returns of the S&P 500 – a difficult benchmark that most managers fail to beat consistently – but do so at expenses so light, the fund might as well be free. FUSVX shares charge just 0.045%, or $4.50 per year for every $10,000 you invest. That just undercuts Vanguard 500 Index Fund (VFIAX) Admiral shares, which charge 0.05%.

What you get with FUSEX and FUSVX is pretty straightforward: An investment in the S&P 500’s component companies, which means a group of 500 blue-chip stocks, including Apple (AAPL), Microsoft (MSFT) and Exxon Mobil (XOM).

But don’t make this mistake of thinking that the S&P 500 is a perfectly balanced index that gives you exposure to every U.S. sector evenly. For instance, information technology makes up 21% of the fund, while financials are nearly 15%. But real estate, materials and telecom stocks each make up less than 3% of Fidelity 500’s weight.

Fidelity 500 Starting to Beat Fidelity’s Legendary Funds

Obviously, you can never beat the market with FUSVX, but a fund that offers simply market performance is a good place to start building your portfolios’ core.

Fidelity Select Technology Portfolio (FSPTX)

Type: Technology sector (actively managed)

Expenses (Minimum Investment of $2,500): 0.78%

Yield: 0.05%

Technology stocks … for retirement?

While it seems counterintuitive, understand this: Many long-held ideas about portfolio composition as investors head toward retirement were created at a time when people simply didn’t live as long as they do now. In 1960, the average life expectancy for an American was just under 70 years – now, it’s just under 79!

That means not only do you need to rethink things like equity/debt ratios as you age, but what the stock portion of that equation looks like.

More simply put, you need some growth in your retirement portfolio.

And where better to get that than technology? Technology is becoming an increasing component of most aspects of our lives. This isn’t a new phenomenon, nor does it show any sign of slowing. The only thing that changes is what technology companies are leading the charge, and that’s where adept active management comes in handy.

Fidelity Select Technology Portfolio (FSPTX) – whose 270-plus holdings include the likes of Apple and Alphabet (GOOGL) – has been under the guidance of Charlie Chai since 2007, and despite the lack of income, FSPTX’s total return has outperformed that of the S&P 500 – and handily, I might add. Since Jan. 4, 2007, Chai’s Select Technology has returned roughly 170%, vs. “just” a double (including dividends) for the S&P 500.

Fidelity Select Technology Portfolio (FSPTX) Is a First-Rate Sector Fund

It’s rare that I recommend a fund that provides so little income, but FSPTX has proven its worth for too long to ignore it.

Fidelity Focused High Income Fund (FHIFX)

Type: High-yield bond (actively managed)

Expenses (Minimum Investment of $2,500): 0.85%

Yield: 4.2%

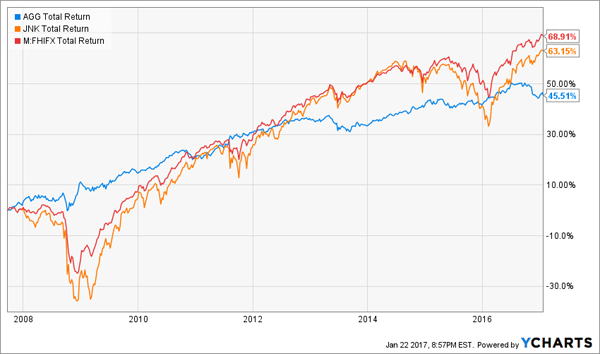

Fidelity Focused High Income Fund (FHIFX) is one of the best offerings in Fidelity’s fixed-income lineup, but despite the “Focused” moniker, it has one of the broadest strategies … at least in theory.

That is, while FHIFX is a high-yield bond fund, it normally invests in “income producing debt securities, preferred stocks, and convertible debt securities,” and it can potentially invest in “non-income producing securities, including defaulted securities and common stocks.”

But for right now, FHIFX is staying mostly true to its name, with an 88% allocation to corporate bonds, 7% in bank debt and 5% in cash.

Now, while FHIFX invests in “junk” debt, the risk here isn’t nearly as high as the name would suggest. For one, the fund invests across 243 different bonds across 158 issuers. Second, that debt is evenly spread over a number of sectors and industries, with energy the largest component at 12%, but telecom, banks and thrifts, tech, financial services and utilities all enjoying high-single-digit weightings.

And lastly, FHIFX does invest in junk, but the lion’s share of the portfolio (82%) is in the highest-rated junk range (82% in BB), and less than 1% of its bonds are CCC or below. In other words, these are junk bonds … but decently rated junk bonds.

Fidelity Focused High Income Fund (FHIFX) Delivers High Total Returns

Manager Matthew J. Conti has been on board since 2004, and the fund boasts strong performance numbers not just against other high-yield debt funds, but against broader U.S. bond offerings, too.

Fidelity Four-in-One Index Fund (FFNOX)

Type: Asset allocation (actively managed)

Expenses (Minimum Investment of $2,500): 0.11%

Yield: 2.1%

The Fidelity Four-in-One Index Fund (FFNOX) offers investors a diversified portfolio within a single mutual fund … and it does so in a pretty odd way. That is, it’s an actively managed fund that holds index funds.

Managers Andrew J. Dierdorf and Christopher L. Sharpe adjust FFNOX’s allocations among four different Fidelity funds – the Institutional Premium Class shares of Fidelity 500 Index Fund (FXAIX), Fidelity Extended Market Index Fund (FSMAX), Fidelity International Index Fund (FSPSX) and Fidelity U.S. Bond Index Fund (FXNAX) – as needed during different market environments.

Currently, the fund is almost half-weighted in Fidelity 500, with 25% in International Equity, 12% in Extended Market and the rest in U.S. Bond.

Fidelity Four-in-One Index Fund (FFNOX): 10% Annual Returns Since 2012

While FFNOX has underperformed the S&P 500 over the past five years, remember: This is a mix of not just large-cap stocks, but also mid-cap stocks, international stocks and U.S. debt, and thus it reflects the combined returns of all those sectors.

When you consider that, and FFNOX’s dirt-cheap 0.11% expense ratio, FFNOX looks extremely attractive as an all-in-one fund.

Live Off Dividends Forever With This “Ultimate” Retirement Portfolio

If you want to retire comfortably, you need big dividends. The steady drumbeat of income is what helps pays the bills and keeps you afloat when you’ve stopped collecting a paycheck.

But if you want to get through retirement without ever touching your nest egg, you need more than just giant dividends – you need dividend growth to beat back inflation, and you need capital appreciation to keep building your nest egg. The “triple threat” stocks in my “8% No Withdrawal” retirement portfolio will deliver exactly that!

How many times have you seen a pundit shill for OK-yielding blue chips like Coca-Cola or Kellogg? They’re not bad companies, but they leave you with just 3% to 4% in dividends, paltry payout hikes and little in the way of growth potential.

You and I both know that math doesn’t add up. Those 3% to 4% returns on a nest egg of half a million dollars will only generate $20,000 in annual income from dividends at the high end!

You’ve worked your tail off for decades. So you deserve more out of your retirement.

My “No Withdrawal” portfolio ensures that you won’t have to settle during the most important years of your life. I’ve put together an all-star portfolio that allows you to collect an 8% yield, while growing your nest egg – an important aspect of retirement investing that most other strategies leave out.

I’ve spent most of the past few months digging into the high-dividend world, and I’ve had to weed out several yield traps that looked great on their surface, but potentially disastrous at a closer look. The result is an “ultimate” dividend portfolio that provides you with …

- No-doubt 6%, 7% even 8% yields – and in a couple of cases, double-digit dividends!

- The potential for 7% to 15% in annual capital gains

- Robust dividend growth that will keep up with (and beat) inflation

This all-star cluster of stocks features the very best of several high-income assets, from preferred stocks to REITs to closed-end funds and more, that combine for a yield of more than 8%.

This portfolio will let you live off dividend income alone without ever touching your nest egg. That means never having to worry about how you’ll pay your monthly bills, and never having to worry about wrecking your retirement account if disaster strikes.

Don’t scrape by on meager blue-chip returns and Social Security checks. You’ve worked too hard to settle when it matters most. Instead, invest intelligently and collect big, dependable dividend checks that will let you see the world and live in comfort for the rest of your post-career life.

Let me show you the path to the retirement you deserve. Click here and I’ll provide you with THREE special reports that show you how to build this “No Withdrawal” portfolio. You’ll get the names, tickers, buy prices and full analysis of their wealth-building potential – and it’s absolutely FREE!