Utilities are a particularly enjoyable sector for income investors because they offer sustainable and growing dividends—if you choose the right companies.

This boring and predictable model means utilities tend to attract risk-averse investors who jump out during times of extreme caution—even when there’s really nothing to be cautious about. That’s why the Utilities Select Sector SPDR ETF (XLU) erased much of its 2016 gains in the second half of the year, when the months leading up to the presidential election led to market panic.

Surprising Volatility

What’s even more interesting is that utilities continued to fall even after Donald Trump won and the so-called “Trump rally” began. Utilities only really began to recover in full at the start of 2017, meaning utility investors are sitting on 20% gains from the start of 2016 to today, excluding dividend payouts.

That’s great if you’re in utilities now, but what if you missed the boat? It’s clearly too late to buy into XLU, but that doesn’t mean the utilities sector remains perfectly efficient. It just means we have to be more selective, instead of simply letting the index pick our stocks for us.

So what criteria should we use to buy utility stocks? We want a high dividend yield, dividend growth, sustainable payouts and stocks that have underperformed the index.

Using those criteria, we end up with five names. Here’s a quick introduction to each one.

WEC Energy Group

Midwestern electricity and natural gas supplier WEC Energy Group (WEC) serves 4.4 million customers in Wisconsin, Illinois, Minnesota and Michigan. These states include some big cities (Milwaukee, Chicago), so WEC’s customer base looks secure.

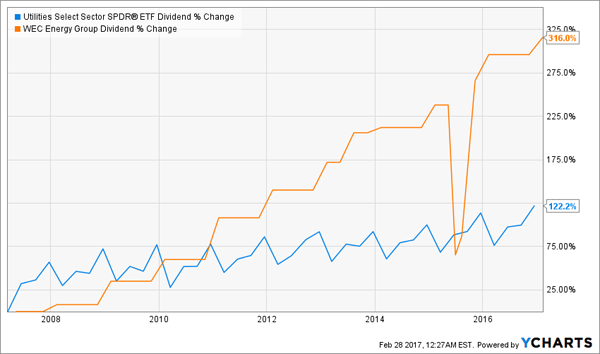

The stock is up 5.4% over the past year, versus XLU’s 11.7% gain, yet it yields slightly more than the index (3.4%) and grew its dividend 316% over the last decade, compared to just 122% for XLU. At that rate, WEC will offer a double-digit yield in a decade, versus just 5.4% for XLU.

Shocking Dividend Growth

Are those payouts sustainable? Absolutely. WEC’s payout ratio (or the percentage of earnings paid out as dividends) is just 66.2%, meaning it can increase its dividend by a third without paying out more than it earns. WEC’s earnings per share (EPS) have also nearly doubled over the last decade and continue to grow. This makes the company’s dividend growth almost guaranteed. Unsurprisingly, management has hiked the payout by 5.1% in the last year.

Great Plains Energy

Great Plains Energy (GXP) is another Midwestern utility, just a bit south of WEC. GXP is headquartered in Missouri and operates in the city, making it a bit smaller than WEC. Its $2.7 billion of annual revenue is growing at a modest pace, but I’m more excited about the 35.7% EPS growth over the last decade—and the company’s 3.7% dividend yield.

What’s even more exciting is GXP’s 8.1% annualized dividend-growth rate. The company has a similar payout ratio as WEC (about 66%), making its payout reliable. Hold this one for a decade and you’ll have an 8% yield.

What’s more, GXP is flat from a year ago, despite utilities’ bull run, making it one of the few high-yielding dividend payers to not rise with the broader market. In an environment where bargains are tough to come by, GXP has become a real gem.

SCANA

SCANA Corp. (SCG) is a South Carolina–based utility that traces its origins back to 1924. It now operates in three states (North Carolina, South Carolina and Georgia) that are positioned for population growth.

Over the last decade, SCANA’s EPS went up 19%, and the dividend has risen 30.7%. The current yield is 3.3%, but that is almost guaranteed to go higher very soon because of a shrewd payout policy from management. SCANA’s dividend has risen just 5.5% in the last year, but the company’s payout ratio is now an absurdly low 40.9%, meaning there is a lot more cash just waiting to be given to shareholders.

Dividend Surge Ahead

Investors are beginning to realize this, which is why SCANA is up 6.3% over the past year. When the dividend hike is announced, expect its price to go up even more.

Dominion Resources

Dominion Resources (D) is an S&P 500 company with a bigger customer base than any other name on our list. It’s a Virginia-based utility with facilities across the east coast, from North Carolina to Massachusetts, as well as some operations in Indiana, Illinois and Wisconsin.

Considering Dominion’s size, it’s shocking that this stock has gone unnoticed for so long. But this happens sometimes; it even happened to Apple (AAPL) in early 2016! Still, Dominion is the top performer of my picks—up 10% in the last year, just a hair below XLU’s return. Yet Dominion has a higher dividend yield (3.6%) and a comparable long-term dividend-growth rate (112.7% versus XLU’s 122%). And Dominion is in the sweet spot for dividend coverage: 60.6%, similar to WEC and GXP.

Buying Dominion gets you conservative income growth and massive geographic diversification, thanks to the company’s sheer size. Purchase this stock today and watch the yield on your initial buy grow to 7.6% in a decade.

NorthWestern

My final pick is NorthWestern (NWE), which, unsurprisingly, operates in the northwest, including Montana, Nebraska and South Dakota. These are sparsely populated areas, so it’s not surprising that NWE is a small company, with just 1,300 employees and a $2.8-billion market cap.

But that small size may be why it’s been criminally overlooked.

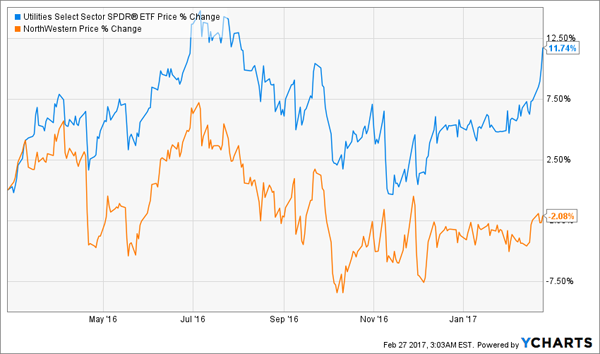

The stock is actually down 2.1% over the last year, versus double-digit gains for utilities generally. There’s no justification for this selloff. NWE’s payout ratio is 58%, and its dividend grew by a whopping 20% in the last year. Considering the low payout ratio even after the dividend hike, there is little justification for this stock staying negative over the past year:

NWE Has Become a Bargain

With the utility rally unlikely to stop anytime soon, NWE is well positioned to benefit as investors scan less obvious corners of the market for value. I want to beat them to it.

As you can see, finding bargain utility stocks with hefty yields and strong payout growth isn’t easy in today’s overbought market.

But the picture changes dramatically when you go dive into overlooked corners of the market like preferred shares, real estate investment trusts (REITs) and closed-end funds. Here, yields upward of 6.0%—and discounts of 15% or more—are common.

You can start with the 6 screaming bargains in our “No-Withdrawal” retirement portfolio. Combined, they throw off a safe 8.0% payout! That’s enough to generate $40,000 in income from every $500,000 you invest.

Here’s what you get in this one-of-a-kind portfolio:

- A 9.9% payer trading at a 10% discount with heavy insider buying in the past month. This one pays dividends monthly!

- An 8.4% yielder that has little correlation with the stock market, giving you valuable “crash insurance.”

- A REIT that also pays 8.4% but has raised its payout for 17 straight quarters.

This is just the start. Simply click here and I’ll give you the names of these 6 off-the-radar income plays and our complete strategy now.