Most investors still don’t understand dividend stocks.

Why?

Because they spend way too much time obsessing over one figure—the dividend yield—and ignore stocks with payouts below some arbitrary number, say 2%, which is about what the SPDR S&P 500 ETF (SPY) pays.

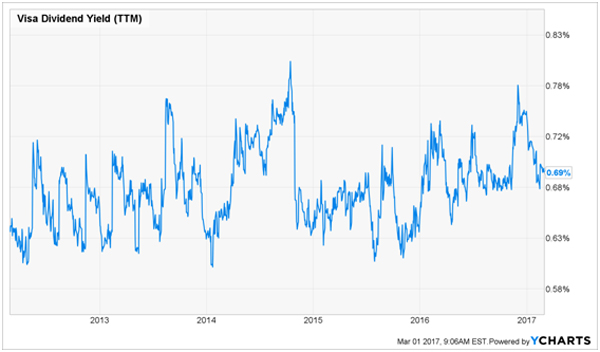

Consider Visa (V), a stock that gets zero love from the dividend crowd, no thanks to its 0.69% trailing-twelve-month yield, which has gone nowhere for five years:

Visa’s Dividend Downer

But if you’ve ignored Visa because of its low yield, you’ve missed out big time—this “boring” chart is actually a sign of powerful growth.

Because what it’s really showing us is that investors have been bidding up V’s share price in lockstep with its payout hikes (because you calculate yield by dividing the annual dividend by the current share price).

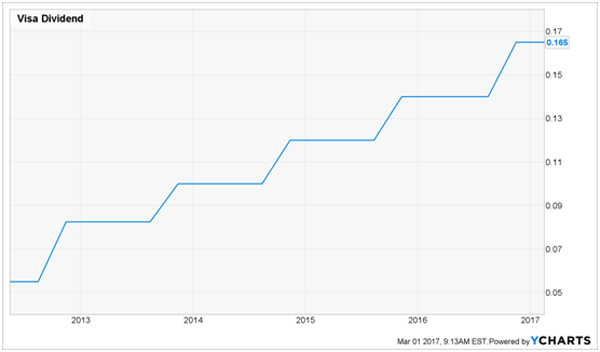

And that dividend growth has been obscene:

The Story Yield Doesn’t Tell

That comes out to a 200% increase over five years! Put it all together, and you can see exactly how those hikes have thrown a relentless lift under the share price, propelling the stock up almost exactly as much as the dividend.

An Unmistakable Pattern

So if you’d bought in five years ago, you’d actually be sitting on a 215% total return (including dividends) on your Visa shares today. And forget about a 0.69% yield—you’d be reaping 2.3%.

Which brings me to the other reason why investors sometimes shun V: its seemingly high forward price-to-earnings (P/E) ratio of 26.7. But the truth is, it’s averaged almost precisely that over the last five years, when the stock went on its stellar run.

The bottom line? You need to look beyond yield and P/E when picking dividend stocks. Adding two other stats will give you a more complete picture:

- The payout ratio—or the percentage of earnings paid out as dividends in the last 12 months—is a measly 23%, so V has plenty of dividend-growth juice left. I consider any figure below 50% a sign of a safe dividend (and higher for real estate investment trusts (REITs), as I’ll explain in a moment.

- Earnings growth: in its fiscal 2017 first quarter, Visa’s earnings per share (EPS) jumped 7.5%, to $0.86 from $0.80 a year ago; the Street expected EPS to fall to $0.78. For all of fiscal 2017, analysts see EPS hitting $3.32, up from $2.84 in fiscal ’16.

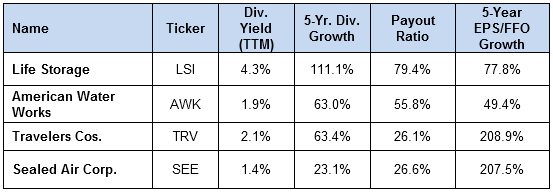

4 More Dividend Growers With Big Hikes Ahead

To find more stocks ready to set us up for big dividend (and share price) growth in the next five years, I’ve scanned the market for names with the same telltale signs as Visa.

As a kicker, I’ve also screened for stocks that hiked their dividends around this time last year—boosting the odds of a big payout increase (and corresponding pop in the share price) as soon as this spring.

Here are four I turned up.

Keep in mind that one (LSI) is a REIT, so I’ve used funds from operations (FFO)—a staple when it comes to measuring REIT performance—rather than EPS for that stock in the last two columns.

Here’s a closer look at our four picks.

The Perfect Business

Life Storage (LSI) operates 650 self-storage facilities in 29 states. This is one of the best businesses there is: once you build these facilities, you really only have to keep the dust off the shelves and hand out keys.

Life’s payout ratio is higher than those of our other stocks, at 79.4%. But that’s manageable for REITs, which generate steady revenue from their various properties; ratios of 85% to 90% of FFO are common in the REIT world.

The trust handed shareholders a 12% dividend hike last March and has plenty of room to do so again: it’s forecasting FFO of $5.50 to $5.60 a share this year—and the midpoint of that range is up 28.4% from last year. That’s a lot of growth for a very reasonable forward price-to-FFO ratio of 16.0.

A Steady Stream of Dividend Growth

American Water Works (AWK) provides water and wastewater services in 47 states and drips out double-digit dividend increases like clockwork: last April, it announced a 10.3% hike, following a 9.7% increase in April 2015 and a similar rise the year before that.

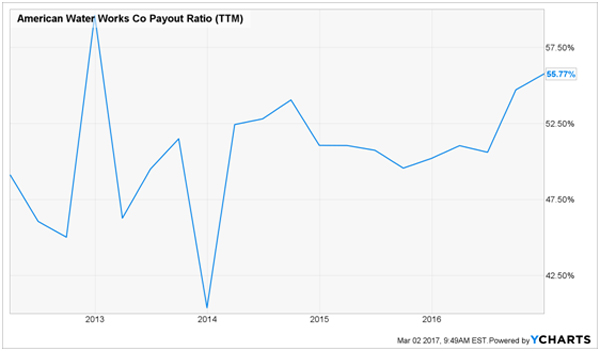

Before I say more, let me address a contradiction you’ve likely noticed: AWK’s payout ratio. At 57%, it’s above my 50% “safe line.”

However, management’s calling for earnings of $2.98 to $3.08 this year, up from $2.82 last year (which was itself a 7.6% rise from the year before). If AWK hits the midpoint of that target, the payout ratio would slip back to 49.5%.

And management’s done a solid job of straddling that 50% mark:

A Safe Payout

Like Visa, you shouldn’t worry about AWK’s forward P/E of 25.6. It’s in line with the five-year average and won’t cap any upside from the stock’s payout growth.

The Breakup Play

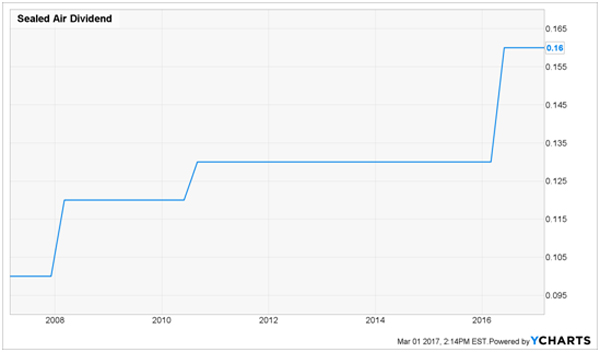

Sealed Air Corp. (SEE) is so boring it makes Life Storage look like Apple (AAPL). The company makes packing materials (including bubble wrap) for food, cosmetics and a range of other products.

SEE has the slowest dividend growth of our five stocks, because all of it came with last March’s hike. Prior to that, the payout hadn’t budged since 2010:

SEE’s Dividend Reignites

The company disappointed the Street when it forecast adjusted EPS of $2.70 for fiscal 2017, well below the $2.95 analysts were expecting. But that’s still up from $2.66 in fiscal 2016.

SEE also plans to sell or spin off of its Diversey Care cleaning-product business, which would simplify the company’s structure—and should spur the stock.

As for the dividend, SEE’s steady earnings and low 25.6% payout ratio give it the flexibility to give investors another raise this month, and the forward P/E of 17.3 is still below the five-year average of 17.7.

Not Too Late to Buy TRV

Travelers Cos. (TRV) is a provider of car, home and business insurance that’s been around since 1853.

I hope you bought this one when I recommended it on November 21. If so, you’re sitting on a 12.3% total return in a little over three months. If not, don’t worry. There’s another catalyst coming: a double-digit dividend increase.

Last April, TRV dropped a 9.8% hike on shareholders, and it’s got plenty of room to do more this April, with earnings arcing higher and its payout ratio at just 25.1%.

Like all insurers, TRV invests the premiums it collects in interest-bearing securities, so it will profit as interest rates rise.

The stock is still reasonably priced at 13.7 times forward earnings. Its dividend hikes and share buybacks (it’s taken 28% of its outstanding shares off the market in the last five years) also hand you some nice downside protection.

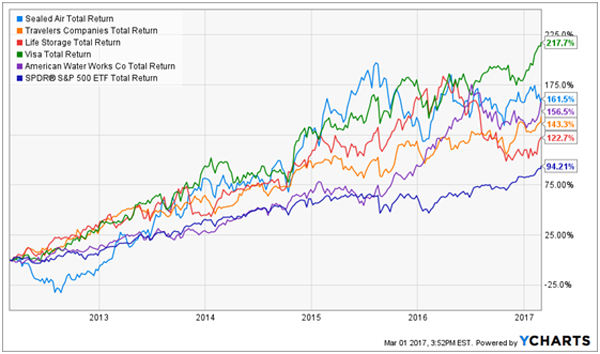

Putting It All Together

When we combine all five of our dividend-growth picks (including Visa) into a diversified portfolio, we see that all have easily beaten the S&P 500 over the past decade on a total-return basis:

Clobbering the Benchmark

I think we’ll see a similar chart five years out—which makes now a terrific time to buy.

6 More Stealth Buys for Double-Digit Gains This Year

These 5 stocks are ripe for buying now … but you can still get the same spectacular growth they offer without sacrificing income today.

In fact, I’ve found a way for you to get at least 7% to 15% price upside in the next 12 months on top of an 8.0% current yield. That’s a 15% to 23% total return by next March, with a big piece of it locked in—in cash!

It comes in the form of the 6 bargain-priced income wonders in my new 8.0% “No-Withdrawal” retirement portfolio. (As you’ve probably guessed, 8.0% is the average yield these 6 rock-solid income plays throw off—but some go as high as 10.1%!)

With the Dow cracking 21,000 and correction fears rampant, these 6 picks are exactly what you need to hold now: because of their fat discounts, they’ll simply trade flat if the market takes a tumble … and we’ll still collect their outsized 8.0% payouts!

I’m ready to take you inside this collection of can’t-miss investments. Simply click here to get my their names, tickers and my complete strategy right away.