Small-cap stocks are the cardiac kids of the market. They can bring high risk, and with that high risk can come high reward. For the first half of the 2020s, the reward hasn’t been there—but that’s beginning to change this year. And today, we’re going to discuss five small caps paying between 6.5% and 15.3% in dividends.

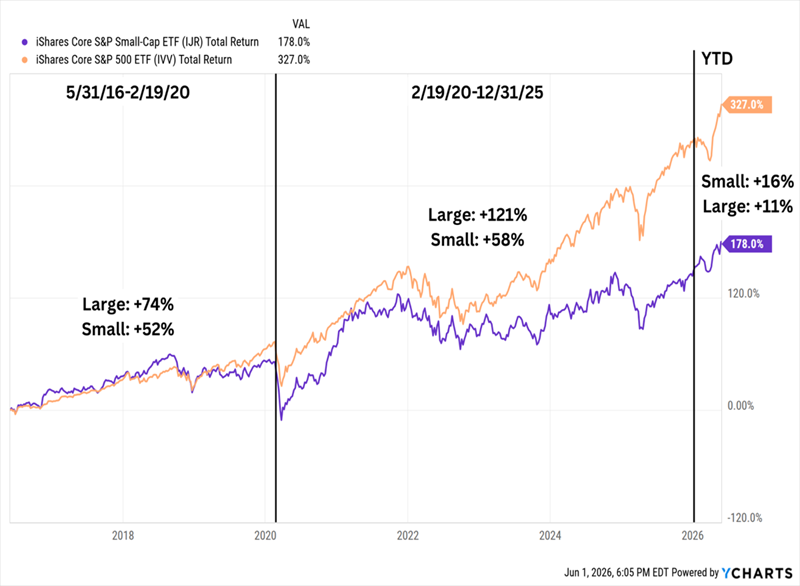

Small caps have lagged over the last 10-year period. Large caps outperformed them handily from 2016 to 2020, and then again from 2020 to 2025. But you can see in the chart below that we now have a turn—small caps have outperformed large caps year-to-date by a margin of 16% to 11%.

It’s Not a Big Data Sample, But Small Caps Could Be Turning the Tide

You’d never guess it, by the way, if you were tuned into CNBC or reading the mainstream financial headlines—because nobody else is talking about small caps.

But we contrarians prioritize high income along with value. We want to buy stocks when they’re cheap, so they can appreciate while they pay us. And when we look at the broader market’s forward P/Es, we see that the S&P SmallCap 600 boasts a price-to-earnings ratio of 15.9—cheaper than both the MidCap 400 and the S&P 500.

Broad-Market Forward P/Es:

- S&P 500: 21.0

- S&P MidCap 400: 16.4

- S&P SmallCap 600: 15.9

Their loss. Our gain.

If we keep our eye on high yields and relative values in the small-cap space, we can set ourselves up for total-return success even if the broader market doesn’t cooperate. Right now, I’ve got a few of them on my radar—a five-pack of small caps paying us a super-sized 10.4% on average.

Newell Brands (NWL)

Dividend Yield: 8.1%

The name Newell Brands (NWL) likely won’t ring a bell, but we’ve all heard of at least some of the home-goods giant’s brands: Rubbermaid containers. Crockpot and Sunbeam kitchen appliances. Mr. Coffee coffeemakers. Calphalon cookware. Yankee Candle. Elmer’s glue, Sharpie markers and Paper Mate pens. Newell even goes outside the home with Coleman camping gear and Bubba water bottles.

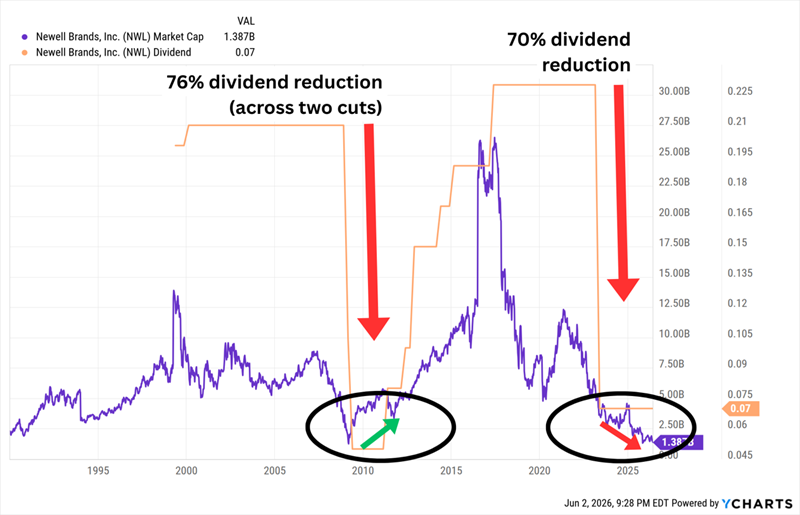

It has never been a massive operation, but what was a $25 billion company less than a decade ago has shriveled to about $1.5 billion—well in small-cap territory and NWL’s lowest valuation since the Great Financial Crisis.

What hasn’t gone wrong for Newell? A number of brand acquisitions turned into busts. The decline of physical retail hurt brands like Yankee Candle. Periods of weak consumer demand never seemed to be met with a resurgence in interest for its various products when the economy improved.

Newell’s financials have eroded. Revenues haven’t improved since 2021. The company has posted net losses in each of the past three years, and in five of the past 10. Net debt of more than $5 billion has remained persistently high. In 2023, NWL slashed its dividend by 70%—not much less than what it was forced to cut back during the depths of the GFC.

And Unlike Last Time, Shares (Nor the Dividend) Have Begun to Recover

The view from 10,000 feet is terrible, and NWL’s price matches the view: Shares trade at less than 6 times this year’s earnings estimates.

The question is whether there’s anything else other than a fire-sale valuation, and the answer is: possibly.

After years of hemorrhaging on both the top and bottom lines, Newell is expected to finally grow both in 2026, albeit very modestly. And Wall Street thinks the company is poised to make a much more substantial improvement to profits (+15%) in 2027. It made progress toward those goals in Q1, thanks to a better-than-expected net loss, higher revenues and thicker margins.

It’s not much given Newell’s lengthy track record of poor operational performance, plus the broader economic picture still isn’t favorable. But we might want to revisit NWL if it starts stacking similarly successful reports.

Betterware de México (BWMX)

Dividend Yield: 6.5%

Newell isn’t the only small-cap home goods story worth eyeing. Betterware de México (BWMX) covers similar territory—kitchen, storage, cleaning—but with a very different financial track record.

Betterware is a direct-to-consumer selling company that offers home organization, beauty and personal care products not just in Mexico, but here in the U.S. It offers fragrances, skin care products and toiletries, as well as laundry and cleaning supplies. And there’s some overlap with Newell in that it offers kitchen and food preservation supplies.

It has predominantly done this under the Betterware and Jafra brands—so much so that the company also refers to itself as “BeFra.” However, it has just folded in a very familiar third name: Tupperware. Just a couple days ago, BWMX closed on its purchase of the Tupperware brand’s operating assets in Latin America.

Betterware, like Newell, spiked in 2021-22 before rapidly retreating, but it has done so on virtually opposite results. Revenues have grown every year since 2020, when it became the first Mexican company to directly list on the Nasdaq. The bottom line hasn’t been as consistent, but BWMX has been solidly in the black every year since coming public.

So whereas Newell has remained in a tailspin, BWMX has been in a broader uptrend since 2023, and has delivered a 140%-plus total return in the past year.

Despite this meteoric rise, shares trade at only 8 times this year’s earnings estimates.

But there are two things to watch out for here:

- Like many international companies, BWMX has a “pay what you can” distribution that can vary from one year to the next. We also get extra variance from one quarter to the next because of the exchange rate between the dollar and the Mexican peso.

- As I mentioned above, Betterware is a direct-to-consumer company. That’s a polite way of saying that it’s a multi-level marketing (MLM) operation. Buyer beware.

Oaktree Specialty Lending (OCSL)

Dividend Yield: 11.2%

Many of the biggest payers in small-cap land are going to come from specialty niches, such as business development companies (BDCs)—finance firms that provide debt or equity capital to smaller businesses when traditional banks don’t want to step in.

Take Oaktree Specialty Lending (OCSL), for instance.

Oaktree is a private debt BDC with a portfolio of 163 companies under its wings. It predominantly deals in senior secured debt, much of that first lien, and most of its debt investments are floating-rate in nature—helpful when Fed rates are rising, but not great when they’re in decline.

OCSL specializes in distressed and opportunistic credit markets, which can be lucrative, but its risk-taking hasn’t always paid off. More problematic of late, though, has been its industry mix. Oaktree’s 20%-plus exposure to software and services would’ve been considered a positive in previous years, but disruption from AI has burned many BDCs with tight ties to the industry.

The company’s fiscal Q2 net asset value (NAV) was 6% less than it was a year ago and about 4% less than the prior quarter—partially to blame were markdowns in the software portfolio, whose fair value dropped by a few percentage points. OCSL’s stock has more than reflected these issues, off 16% over the past year (and 7% year-to-date). So while we were paying 87 cents on the dollar a year ago, we’re only paying 78 cents today.

That, and the 11% yield, would make Oaktree a screaming deal if we had any clue for just how long we’d actually be getting that 11% yield.

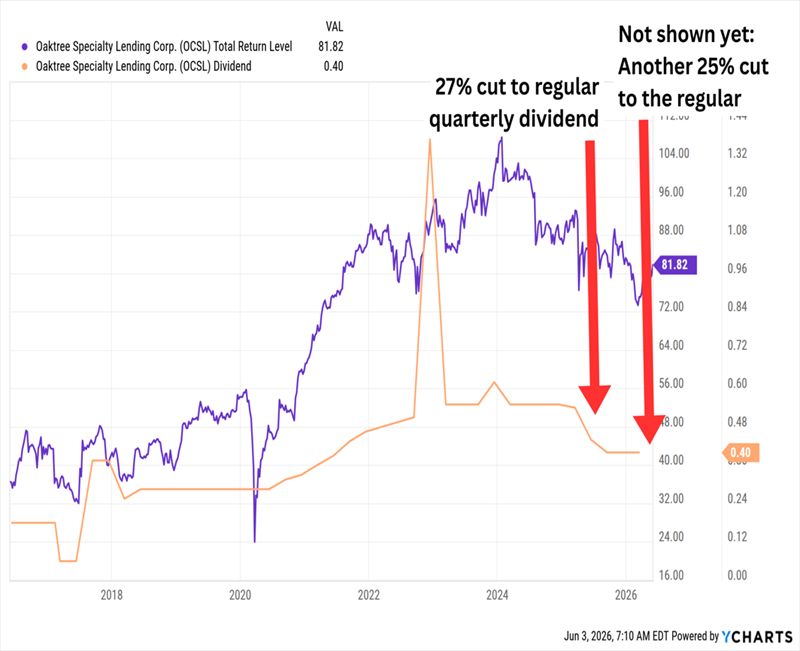

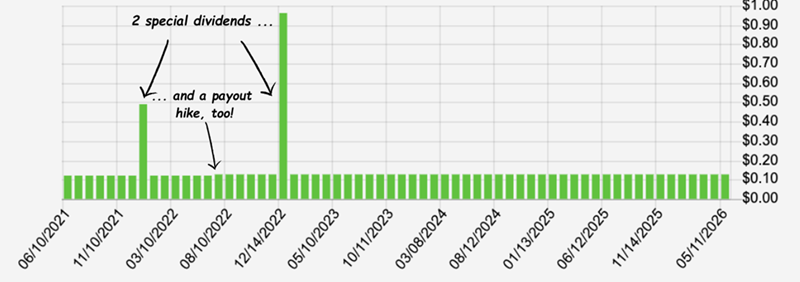

OCSL Has Now Made 2 Dividend Cuts in a Little More than a Year

BDCs, like real estate investment trusts (REITs), are required to pay out at least 90% of their taxable income as dividends. Rather than promise above and beyond that and risk overstretching, many BDCs will sometimes pay a constrained (but still generous) regular dividend that they’ll supplement with special dividends as net investment income allows.

Oaktree doesn’t often pay specials, and the past couple of times it has done so, it has come in tandem with a large cut to the regular dividend, helping soften the income blow. When it cut from 55 cents to 40 cents in February 2025, it added a 7-cent special that withered to 2 cents the next quarter and evaporated by the fall. OCSL announced in May that it would clip its regular distribution again, to 30 cents, but offered an additional 4 cents in supplementals.

OCSL isn’t shy about sharing the wealth when times are good—it’s there in the chart, too, including raises to the regular dividend and a couple of nice supplementals. But until non-accruals shrink and NAV finds a floor, that fat yield is a consolation prize, not a reason to buy.

Arko Petroleum (APC)

Dividend Yield: 10.4%

Arko Petroleum (APC) is a freshly minted stock that got its start earlier this year, and rarely will you see such a high payout from an IPO outside of the REIT/BDC set.

In February, ARKO Corp. (ARKO), one of the nation’s largest operators of convenience stores and wholesalers of fuel, spun off the primary operating entity of its wholesale, fleet fueling and GPM Petroleum fuel supplying businesses.

That new publicly traded company, Arko Petroleum, has come out swinging, paying a pro-rata 26 cents per share in April, then announcing in May that it expected to pay 50 cents for its full dividend during the second quarter. That comes out to a wild 10%-plus yield at current prices.

And while it’s not dirt-cheap, it’s still relatively inexpensive. Wall Street is looking for roughly 30% earnings growth this year and another 11% next year. Yet shares trade at just 14 and 13 times those estimates, respectively.

There’s real short-term danger here, of course. APC went public just before the Iran war, so it started trading amid a reasonable gas-price environment, only to quickly face extreme volatility in the energy markets. The company says that while customer behavior is changing—people are making more frequent but smaller-ticket visits—it hasn’t yet seen any demand destruction. But that could be coming if the Strait of Hormuz remains closed throughout the summer.

Still, Arko Petroleum is managing things well so far. Results from its first full quarter as a publicly traded company were well ahead of the Street consensus, and the company plans to add another 20 NTI Fleet Fueling stores, which is expected to boost its margins. It also has an interesting ace up its sleeve. APC receives 1.25% prompt-pay incentives from its fuel supply partners—when gas prices rise, so too do these incentives, which the company says “largely [eliminates] our exposure to commodity price movements.” That wouldn’t fully offset the harm if consumers avoid the pump this summer, but it’s a helpful buffer.

PennyMac Mortgage Investment Trust (PMT)

Dividend Yield: 15.3%

We can’t talk about high-yielding small caps without talking about mortgage REITs (mREITs).

Mortgage REITs borrow money at short-term rates to purchase mortgages (and other assets) that pay income tied to long-term rates, then profit off the difference.

They want short-term rates to be lower than long-term rates (and they usually are), and their ideal situation is for short-term rates to be declining while long-term rates hold steady or move lower. The mREITs’ existing mortgages, which were issued when rates were higher, will yield more than newly issued ones, and thus be worth more.

PennyMac Mortgage Investment Trust (PMT) primarily invests in residential mortgage-related assets. Its business is split into three categories:

- Credit Sensitive Strategies: credit risk transfer (CRT) agreements, subordinate mortgage-backed securities (MBSs), credit-linked MBSs

- Interest Rate Sensitive Strategies: Mortgage servicing rights (MSRs), agency MBSs, senior non-agency MBSs, collateralized mortgage obligations (CMOs)

- Aggregation and Securitization: Purchasing, pooling and reselling newly originated prime-credit-quality loans

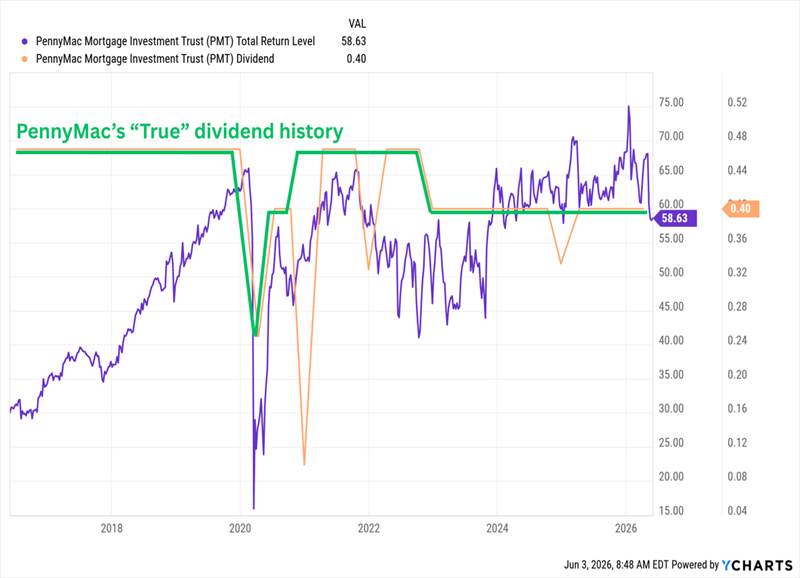

Because mREITs tend to be much more sensitive to external factors (namely interest rates) than physical-property REITs, their dividends tend to skew a bit more mercurial. Rate cuts are common, though so are increases if the environment allows. PMT itself has cut twice—a COVID-era cut that was reversed, as well as a smaller reduction in 2022 that it hasn’t yet walked back.

PMT’s Chart Makes Its Dividend History Look Worse Than It Is

Because mREIT dividends often compensate for poor price performance, we really want to pick our shots. Right now, for instance, PennyMac has been shellacked, off 15% year-to-date even with its monster dividend included. That has PMT shares trading at less than 9 times 2026 earnings expectations and 7 times 2027 estimates, and at just 70% of book value.

But PennyMac isn’t down for nothing. Its Interest Rate Sensitive Strategies arm has been struggling, and management expects that to continue. That led to a wide Q1 miss and lowered guidance.

Here’s the number that keeps me cautious: PMT’s portfolio is generating run-rate potential of 31 cents per share per quarter. It’s paying out 40 cents. That’s not a yield—that’s a countdown. Unless the other segments step up fast, another cut is a real possibility.

This Growing 11% Dividend Is One of Our Top Buys Right Now

Dividends are supposed to help us absorb volatility—but when sky-high yields are every bit as shaky as the stock, all we’re buying is a false sense of security.

That’s what makes my favorite 11%-paying fund a must-buy for serious income investors.

Check out the dividend history: The only changes in this fund’s monthly payout are for the better—the regular distribution has growth over time, and its shareholders have even pocketed the occasional special dividend!

This 11% Payday Is the Real Deal

We can also sleep soundly at night knowing that this fund is helmed by one of the best managers in the bond business—literally. Morningstar previously named him Fixed Income Manager of the Year. And he’s literally a hall-of-famer, honored by the Fixed Income Analysts Society Hall of Fame.

And because this fund is actively managed, it can drop in and hoover up sudden bond discounts that index funds simply aren’t built to identify and snare.

This “battleship” fund is a must-buy for all income investors, and I want to share my complete research on it right now. Click here and I’ll introduce you to this powerful 11% payer and give you a free Special Report revealing its name and ticker.