The stock market is overdue for a correction (to say the least). And when the rising tide pulls back, certain dividend dogs will be exposed.

It’s all well and good to chase 5% and 6% dividends as “bond proxies” when the market continually grinds higher. It’s another story when stocks begin to wobble – and an entire year’s worth of yield is jeopardized in a down week!

Of course some dividend stocks will hold up just fine. But we’re going to pick on three that are likely to be exposed when the bullish music stops.

Gladstone Investment (GAIN)

Dividend Yield: 6.8%

Back in July, I highlighted Gladstone Investment Corporation (GAIN) as a business development company stud amidst a pair of BDC duds.

Gladstone provides debt and equity financing to manufacturing, consumer products and business services/distribution companies. Portfolio holdings include the likes of Ponca City, Oklahoma’s Head Country Bar-B-Q (a barbecue sauce maker), Ripon, California’s Jackrabbit (a nut harvesting equipment manufacturer) and Winston-Salem, North Carolina display specialist ImageWorks.

And at the time, I highlighted a few things to like, such as a generous monthly dividend and a 5% discount to net asset value.

So, what has GAIN been up to in the meantime?

Well, it produced a decent enough fiscal Q2 report at the end of September, improving its net interest income by a penny per share to 18 cents – total investment income actually declined sequentially, but the company cut back on expenses by about 10%. The company also upgraded its monthly payout from 6.4 cents per share to 6.5 cents.

But the stock has really taken off since September, jumping 22% against a 4% decline for the VanEck Vectors BDC Income ETF (BIZD). There’s nothing wrong with that – but the result is a suddenly overbought status in which GAIN is trading at an 11% premium to NAV. This still is a quality name, then, but a market pullback could knock off some of Gladstone Investment’s recently acquired froth.

Gladstone Investment (GAIN) Is Sitting in the Nosebleeds

Buckle (BKE)

Dividend Yield: 5%

When it comes to dangerous dividends, Guess? (GES) and Abercrombie & Fitch (ANF) are popular whipping boys. But Buckle is up 26% in the past three months – even including a recent pullback – and could be set up for more losses should the market pull back.

While retail has been hammered over the past few years amid the increasing encroachment of digital vampire squid Amazon (AMZN), the industry received something of a respite over the past few months amid tax-law optimism and a stellar holiday shopping season.

Buckle, however, didn’t look so hot.

The retailer announced a 4% year-over-year decline in revenues for November, on a 3.6% decline in same-store sales. It followed that up with a 4.8% dip in net sales for December, on a 4.1% stumble in comps. And when the company reports fourth-quarter earnings here in about a month, analysts expect merely flat sales and a 3% decline in profits. That doesn’t sound like a fruitful holiday to me.

BKE shares aren’t expensive, per se, at 12 times forward estimates, but why should they be? The company should finish off 2017 with a 16% drop in earnings, followed by another 4% dip next year. Expect Buckle to keep shedding its gains from the past few months, especially if its Q4 report comes out ugly compared to the rest of the fashion retail field.

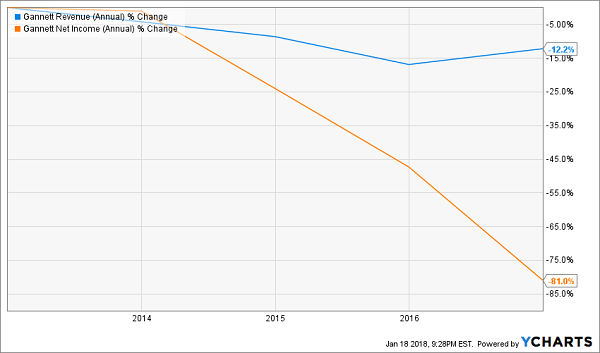

Gannett (GCI)

Dividend Yield: 5.4%

For a long time, Gannett (GCI) was a somewhat sneaky media play. That’s because while most people knew it for its USA Today and other print brands, the company also sported digital and attractive broadcast businesses.

No more. The company in 2015 spun off the publishing business, which retained the Gannett name, and the growth divisions remained in the newly dubbed Tegna (TGNA). That merely exacerbated what already was a steadily diminishing income situation – from $277 million in 2012 to $211 million in 2014 to $53 million last year.

The company did make a stab at further consolidating the publishing business, offering in 2016 to buy Tronc (TRNC) – the former Tribune Publishing, which owns the Chicago Tribune and Los Angeles Times – but dropped the bid after an unsuccessful six-month courtship.

Shares have run up 25% in the past few months to boot, bringing the company’s forward price-to-earnings ratio to about 14. That’s hardly Rubenesque, but it doesn’t look great when you consider that’s based on analysts’ predictions for an 8% profit decline next year.

Gannett’s (GCI) Results Are Like Its Papers: Shrinking

Besides, the optimism likely has to do with the same thing driving many other domestic stocks – a reduced corporate rate, which benefits Gannett in an outsize way given its American-centric business and high 30%-32% effective rate. It helps the bottom line, but it doesn’t solve publishing’s terminal decline.

Meanwhile, that dividend isn’t exactly pristine. At 16 cents quarterly, it represents 98% of the company’s profits in the first three quarters of 2017. Yes, the dividend looks more sustainable on the cash-flow front, but that’s another figure that keeps diminishing over time.

You can do better than an above-average but not spectacular dividend in a dying industry.

3 Ways to Safely Bank 8% Dividends

Most of the stocks you read about in the mainstream media that pay 5% or better are train wrecks. They have big stated yields for the wrong reason – namely, because their prices have been axed in half or worse over the past year!

For example, retailer Macy’s (M) pays 7%+ on paper. But its business model is toast. Next quarter’s payment may happen, but that’s a risky game I’m not willing to play.

Instead, I’d rather look in corners of the income world that aren’t combed over as regularly. There are three in particular that I like today. You won’t hear about them on CNBC, or read about them in the Wall Street Journal, because they don’t buy advertising like Fidelity and other firms.

Their relative obscurity is great news for us 8% dividend seekers.

Play #1: Closed-End Funds

If you feel trapped “grinding out” dividend income with classic 3% payers (like dividend aristocrats), you can double or even triple your payouts immediately by moving to closed-end funds, or CEFs. In fact, you can often make the switch without actually switching investments.

I’ll discuss my favorite CEFs in a minute.

Play #2: Preferred Shares

Not familiar with preferred shares? You’re not alone – most investors only consider “common” shares of stock when they look for income.

But preferreds are a great way to earn 7% and even 8% yields from the same blue chips that only pay 2% or 3% on their “common shares.”

I’ll explain preferreds – and my favorite tickers to buy – after we finish our high yield hat trick.

Play #3: Recession-Proof REITs

The IRS lets real estate investment trusts, or REITs, avoid paying income taxes if they pay out most of their earnings to shareholders. As a result these firms tend to collect rent checks, pay their bills and send most of the rest to us as a dividend. It’s a sweet deal.

Not all REITs are buys today, however – landlords with exposure to retail space should be avoided.

That’s easy enough to do. I prefer to focus on REITs that operate in recession-proof industries only. I want to receive my rent check powered dividends no matter what happens in the broader economy.

Now let’s discuss how you can get a hold of my complete “8% No Withdrawal Portfolio” research today, along with stock names, tickers and buy prices. Click here and I’ll share the specifics – and all of my research – with you right now.