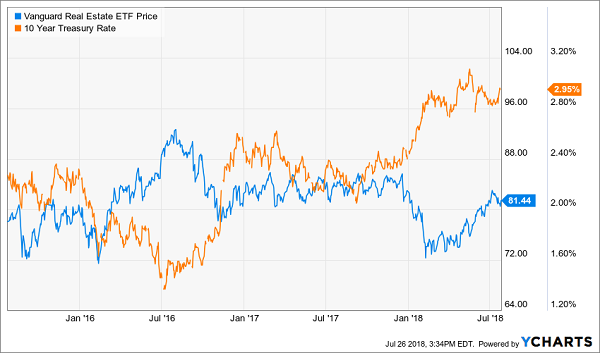

Have real estate investment trusts (REITs) finally “decoupled” from rising interest rates? In other words, has the popular (but untrue) “rates up, REITs down” reasoning been busted (again)?

For those of us who have been waiting for the stock market’s landlords to carve out a bottom before buying anything new, we may be back in business:

REITs Finally Rising with Rates?

Regular readers know that the best REITs do just fine as rates rise. That’s been the case historically, and they’ll rally again this time around.

Why? Because elite landlords simply keep raising their rents. These higher cash flows translate to higher dividends, and higher stock prices, regardless of what the Fed is up to.

Let’s consider the case of Ventas (VTR), which kept on hiking its payout as Uncle Sam’s 10-year IOU rallied from 2003 to 2006. Its investors were rewarded with total returns (including dividends) of 174% as the 10-year rate rose above 5%:

Ventas Outran the Long Bond

Also as you can see above, it didn’t take Ventas much time to start scaling the rate-induced wall of worry. We’re starting to see the same scenario unfold with the top REITs today.

But what exactly are “the best” REITs? Certainly not retail, where even reliable anchor tenants like grocers are seeing their business models threatened.

Heck, even Ventas is having a rough go of things today. Its dividend growth has slowed considerably in recent years.

We’re better off looking elsewhere. So let’s consider the early leaders – the sectors sparking this budding REIT rally. If it proves to have legs, these are the stocks likely to continue paving the way.

Let’s highlight four REITs most investors – even serious income hounds – have never heard of. Here’s where we’ll find a couple of hidden high yield gems to consider.

CatchMark Timber Trust (CTT)

Dividend Yield: 4.3%

This first REIT can be found in the great outdoors. CatchMark Timber Trust (CTT), at about $615 million in market capitalization, is one of the smallest players in the timberland real estate space. But there’s nothing small about its properties: some 514,100 acres of commercial timberland across eight states, split between 75% pine and 25% hardwood – destined to eventually become wood products, pulp and paper.

It’s not a scintillating business, but it does create steady, predictable cash flows. As for growth: CatchMark is trying to achieve that through acquisitions. The company has made 24 M&A transactions totaling $509 million since its 2013 initial public offering, accounting for about half its acreage.

But the deal I’m most excited about is a May announcement that a joint venture including CTT would spend a total of $1.39 billion to gobble up 1.1 million acres of timberland in east Texas. That timberland currently supplies International Paper (IP) and Koch Industries-owned Georgia-Pacific.

This is a game-changing move that is ballooning CatchMark’s acreage. It’s also expected to immediately be 2% to 3% accretive to cash available for distribution (CAD), which could nudge CatchMark into a (long overdue) dividend increase. This is an encouraging setup in a little-traveled industry.

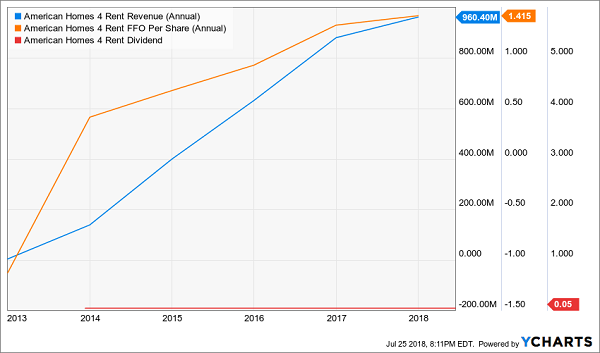

American Homes 4 Rent (AMH)

Dividend Yield: 0.9%

You can tell by the yield alone that American Homes 4 Rent (AMH) is not ready to deliver retirement income yet. But I think in decades, not months, and I think AMH should be on your long-term watch list as a “future star of tomorrow.”

REIT investors are familiar with residential plays such as AvalonBay Communities (AVB) and Preferred Apartment Communities (APTS), and I’ve even introduced investors the more niche play of “manufactured home” REITs such as Sun Communities (SUI).

But American Homes 4 Rent is a little different. AH4R is one of the top names in single-family home rental, boasting 51,840 single-family homes in 22 states. Its target home typically is built after 1990, is at least 3BR/3BB and is located in areas with above-average median household incomes and near attractive school systems.

Business has been humming since the company’s 2013 IPO, with revenues and funds from operation (FFO) climbing each and every year. Also, AH4R said in June that building rental properties is generating an extra 50 basis points by building single-family homes rather than purchasing existing inventory. Higher occupancy, and the ability to consistently raise rents, makes for an attractive business case.

I say that American Homes 4 Rent is a “future star of tomorrow” because from a dividend perspective, it’s certainly not ready today. The company yields less than 1%, and that’s not because share-price gains are outpacing its rate of dividend growth – there is no dividend growth. The payout has been stuck at its same level since the REIT came public.

For now, AMH is a hard pass. If it changes its stance on dividends, let’s reconsider.

AH4R Is Growing Its Wealth, But It’s Not Sharing It

Vici Properties (VICI)

Dividend Yield: 5.1%

Casino REITs aren’t exactly an unknown. I’ve covered plays such as Gaming and Leisure Properties (GLPI) – a high-yield regional casino operator – before.

But Vici Properties (VICI) adds a small twist to the entertainment theme.

Vici, which was spun off from Caesars Entertainment Operating Company in 2017, owns 20 “market-leading” gaming properties, leased out to Caesars Entertainment Corporation (CZR). The properties operate under the Caesars, Horseshoe, Harrah’s and Bally’s brands – including the famous Caesars Palace – and includes 14,500 rooms and more than 150 restaurants, bars and nightclubs.

The kicker is diversification. For one, some of the properties are so-called “racinos” that include horse racing in addition to traditional gambling. Also, the company has a good geographical spread that includes not just Las Vegas (35% of portfolio revenues), but New Jersey, Indiana, Louisiana and Missouri, among other states. On top of all that, Vici isn’t just gaming: It has a little revenue diversification in the form of four championship golf courses, including top-100 ranked Cascata in Boulder City, Nevada.

The company has scant financial history to go off of – it’s simply too young. But it has an attractive portfolio that may enjoy not just a strong current environment for casino operators, but also a potential boom in regional interest as states begin to approve sports betting.

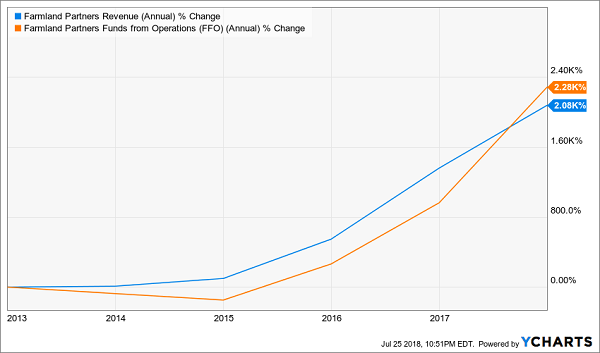

Farmland Partners (FPI)

Dividend Yield: 7.8%

One of Wall Street’s most exciting stories right now is taking place down on the farm.

Farmland Partners (FPI) owns or has under contract more than 166,000 acres of farmland across 17 states, farmed by more than 125 tenants and yielding more than 30 types of major commercial crops. Management is made up of several officers with actual farm operations knowhow.

The business has enjoyed rising rents, and a boom in food commodity prices should only help FPI’s case.

But Farmland Partners also is the subject of a massive scandal that isn’t getting much press – which could spell opportunity. Specifically, a Seeking Alpha contributor that goes by the name of Rota Fortunae wrote a wildly bearish article about FPI claiming that the REIT was “uninvestible” because it was “artificially increasing revenues by making loans to related-party tenants who round-trip the cash back to FPI as rent; 310% of 2017 earnings could be made-up.”

Is Farmland Partners’ Success Too Good to Be True?

The result was a drop of as much as 40%, sending FPI’s yield through the roof.

A High-Risk, High-Reward Opportunity?

Rota Fortunae’s article wasn’t the final word on FPI – not by a long shot. Days later, Farmland Partners released a laundry list of defenses against several points made by Rota, and said the article was “false and materially misleading in numerous respects.” A week after that, FPI filed a lawsuit against Rota, seeking damages for what it calls a “short and distort” scheme.

Shares have rebounded somewhat since then, but there’s still a massive discount in FPI – and a historically high yield to boot! However, investors face a pivotal question of how much (if any) truth was in Rota’s commentary.

7 Rate-Proof, Recession-Proof REITs for 8.5% Yields (And Upside!)

It’s possible that Farmland Partners is a once-in-a-lifetime discount – a solid company with a now-enormous yield that has been slandered and will rebound with a vengeance.

Are you willing to bet your retirement on it? I’m not.

You can’t rely on solid-but-so-so yields and a couple of high-yield gambles to fund your retirement. You need to average 8% across the board with bulletproof holdings.

That’s no problem for my 8% No Withdrawal Portfolio! All seven REITs in the portfolio check both boxes for “dividend growth” and “high current yield” – a must-have for rising-rate environments.

As a group, they pay an impressive 8.5% average yield today. That’s outstanding in a 3% world.

Combine 5% to 10%+ dividend growth with these high-single-digit current yields, and we have a formula for safe 15% to 20%+ annual gains from REITs. With a significant portion of that coming as cash dividends.

And thanks to the new tax plan, there’s never been a better time to buy REITs and live off their dividends.

(REIT investors will benefit from the tax breaks that “pass through” businesses will receive in the new code. Investors will be allowed deduct 20% of their REIT dividend income, which means the 37% tax bill will drop to 29.6%.)

But it’s important to choose your REITs wisely.

Don’t buy low-yielding static payer. Don’t buy a retail REIT, either (with that entire industry is in a death spiral, future rent checks will be dicey for years to come).

Instead, focus on recession-proof firms, such as those that rent hospitals, business lodging and warehouses filled with Amazon packages. Landlords that own properties that will be in high demand no matter what happens to interest rates or the economy from here, in other words.

I’d love to share my seven favorite recession-and-rate-proof REITs with you – including specific stock names, tickers and buy prices. Click here and I’ll send my full 8% No Withdrawal Portfolio research you to right now.