Legendary investor Peter Lynch was fond of saying that corporate insiders may sell their company’s shares for a variety of reasons. But there’s only one reason they buy – and that’s because they think the price is going up.

Anyone at the director-level or above in Corporate America is considered an “insider” – and it’s perfectly legal for them to buy their own company’s stock. That’s a good sign in general, and especially for the stocks that we’re interested in. It means the executive buyer is bullish on dividend growth, and as we’ve discussed before, payout growth is what ultimately sends stock prices higher.

Executive teams from two of our Contrarian Income Report companies are, right now, using personal money to buy up their own cheap stocks and big dividends. That’s a big sign of confidence, and I’ll share the specifics in a minute. But first, let’s talk about a few more big payouts being bought by corporate insiders.

Seven 7% Dividends With Serious Insider Buying

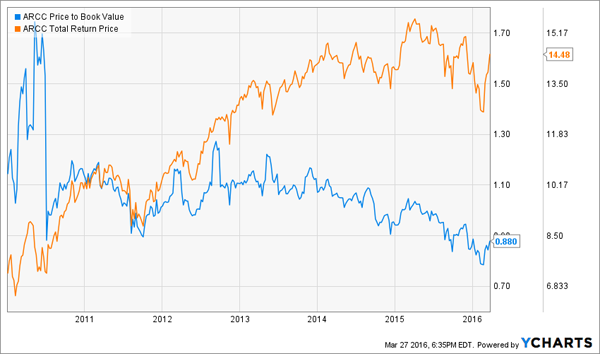

Five insiders at Ares Capital (ARCC) have accumulated more than 150,000 shares for personal accounts over the last 3 months. These executives like their stock at 88 cents on the dollar. ARCC trades for just 88% of book value today, a bargain level it hasn’t yet seen this decade.

ARCC Has a History of Rallying Off Cheap Book Values

ARCC usually trades for around 100% of book value. Being a business development company (BDC), that’s typically a fair floor price for the stock – thanks to quarterly audits of its books by a third-party (a requirement for all BDCs). And as you can see from the chart above, pullbacks in price-to-book have been good buying opportunities recently.

Prospect Capital (PSEC) is popular with its own management team as well. They’ve purchased more than 7 million shares over the last three months, as this BDC trades for just 74% of book value. Granted it often trades below book, because Prospect’s management team isn’t regarded as being as shareholder-friendly as ARCC’s and other competitors. But even with the perpetual discount, PSEC is rarely this cheap.

Regular readers know that I’m not big on BDCs as buy-and-hold stocks. Granted, they have huge dividends (ARCC pays 10.5%, PSEC pays 14%). But their profits rely on financial wizardry that can be foiled when credit markets tighten or interest rates rise. Still, they’re interesting speculations today with insiders buying and cheap relative valuations.

Mortgage REIT insiders are getting greedy, too. They’re buying up their own shares trading at big discounts to book value – inspired by recent acquisitions in the space.

Earlier this month, Armour Residential REIT (ARR) made an acquisition offer for Javelin Mortgage Investment (JMI). Javelin was trading for just 63% of book value prior to the offer, and Armour offered to pay 87% – which is a 40% premium to current share prices.

High-level managers at American Capital Agency (AGNC), Chimera Investment (CIM) and Invesco Mortgage Capital (IVR) see similar value in their own share prices, which trade for 82%, 88%, and 69% of book respectively:

These mREITs Haven’t Been This Cheap This Decade

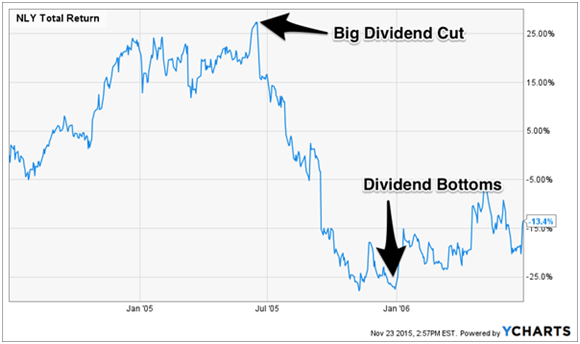

Like their BDC counterparts, “mREITs” are fair speculations here. But the potential of higher rates is a concern of mine. During the last rising rate cycle from June 2004 through June 2006, even “gold standard” mREIT Annaly Capital (NLY) lost 13.4%.

Annaly Suffers Last Hike Cycle

Right now the “smart money” is pricing in a 73% chance of a rate hike by December (via Fed Fund futures prices). Granted, the most likely scenario is a single quarter-point hike (40% implied probability). Still, the fixed-rate securities that mREITs hold will decline in price each time rates climb – even if it’s just a quarter-point at a time.

Big Insider Buying In Healthcare

Rate hikes won’t be a problem for healthcare executives, who are enjoying tremendous demographic dividends. There are 10,000 Baby Boomers turning 65 every day. They’re the reason the 65+ population will double and 85+ will triple in the years ahead.

Given these tailwinds, you’d expect these insiders would struggle to find their own shares at bargain prices. But the sector is on sale this month, thanks to a cautious outlook from HCP (HCP) that sent its stock – and those of its competitors – sharply lower.

HCP may have trouble executing its business operations, but its management team knows a good deal when they see one. Since the stock’s post-earnings plunge, execs have bought more than 37,000 shares. Each purchase is already profitable, with an average gain north of 10%. HCP yields 7.3% today.

Shares of Sabra Health Care REIT (SBRA) lost more than 25% in a one-month span, thanks to worries about China (completely unrelated to Sabra) and HCP. Insiders smartly moved in, swooping up 230,000 shares over the last three months.

The stock yields 8.6% today. It’s a decent play today, but in my opinion the healthcare market has too many opportunities for us to entrust our capital with mediocre operators like HCP and Sabra, both of whom have a history of earnings disappointments.

In lieu of these two, I prefer three smaller (and much better run) healthcare firms with heavy insider buying. They’re stock prices are also dirt-cheap thanks to the recent China and HCP worries, trading for around 10-times cash flow.

They’re managed by executives that have demonstrated time and again they know how to create business value – and pass on the lion’s share of their profits to shareholders. That’s why these firms are raising their dividends every year – and in one case, every single quarter.

Their stocks pay healthy yields of 6.7%, 7%, and 8.9% today already. With dividend growth, you’ll be earning a growing 10%+ yield on your initial investment in just a few years.

And the best time to buy these stocks is right now, before Wall Street uncovers these hidden gems and sends their analysts stumbling into coverage. Click here, and I’ll give you the name and ticker for each one, along with my full analysis of each pick.