The key to beating the market – AND keeping your nest egg intact – is diversification. If you don’t put all your eggs in one basket, you can avoid the pitfalls of exposure to one particular company.

For example, people who bought and held Wells Fargo (WFC) after seeing Warren Buffett praise the bank as a safe, reliable pick have been horrified to see the stock plummet on the recent fake account scandals. You could have avoided this by investing in a diversified financials ETF like the Financial Select SPDR Fund (XLF). With that fund, you’d be up 1.5% year-to-date and have a 2.6% yield based on today’s current price.

That’s not bad, but we can do much better.

In fact, we can avoid being exposed just to the financial sector. The problem with sector ETFs like the SPDR funds is that they provide exposure to one particular industry, and the fund’s management company—State Street—is hoping you avoid this risk by buying several SPDR sector funds and rebalancing them as you go along.

This isn’t the greatest strategy, in part because these funds have very low income streams. We can secure higher cash streams immediately if we look at alternative strategies, and we can diversify ourselves across the entire market at the same time.

Not only that, we can do this with a group of four funds that give us risk-adjusted exposure to large-cap stocks, corporate bonds and municipal bonds. This is a powerful strategy because these are uncorrelated assets. When stocks go up, munis don’t necessarily go up with them. More importantly, when the market panics and stocks sell off, municipal bonds don’t necessarily go with them. To illustrate this point, let’s take a look at the beginning of 2016.

When the market panicked, municipal bonds yawned:

Munis Shrug Off Market Fears

The panic sell-off at the beginning of the year didn’t touch municipal bonds. Diversifying between stocks and municipal bonds protects us from a big downturn in one of those asset classes.

So let’s start the portfolio with some munis. These are great investments because they’re tax-free for most Americans, they’re very low risk (defaults are almost unheard of, well below 0.1%), and they pay high yields. And we can get them at a discount with the Invesco Value Muni Income Fund (IIM), which is trading at a 6.4% discount to NAV, the biggest discount for 2016.

IIM is Suddenly Very Cheap

In fact, this fund is trading at a bigger discount than it has averaged since its inception in the mid-90s, so I consider this fund to be on sale. And like any good bargain, it won’t last. That makes this a great opportunity to lock in a 4.7% dividend yield in an ultra-low risk asset class.

We also want to diversify across sectors, regions and companies, so we’re going to buy broad funds that own assets in hundreds of firms. There are hundreds of such funds to choose from, but we’ll limit our risk even further in a couple of ways.

We’ll choose a fund of stocks that only includes dividend aristocrats, because these firms have a solid history of dividend payouts, tend to be large and have solid business models and moats that make them low-risk holdings. Let’s pick the ProShares S&P 500 Aristocrats ETF (NOBL), which is up 8.2% year-to-date versus 6% for the S&P 500.

A Surge in Dividend Payers

That outperformance is a bit troubling for a buyer right now, because it leads to the question of whether we’re buying at a top. That’s why we’ll want to add some downside protection. We can do this by buying a fund that uses a covered-call or buy-write strategy.

If you’re unfamiliar with stock options, the basic idea is that these funds sell insurance on their stock holdings on the open market, which adds income to the fund and protects the fund in the case of a market downturn. The covered-call strategy works best in flat or slightly-down markets, and that’s what we want to protect ourselves against to offset buying NOBL after its recent run-up.

We also want to stay with large-caps because they’re safe, and that means choosing the Nuveen Dow 30SM Dynamic Overwrite Fund (DIAX). Many people don’t even know this fund exists. It only started trading in early 2015, and now only about $1 million worth of shares are traded per day. Yet the fund’s holdings are the biggest companies in the Dow Jones Index and it uses covered calls to protect that fund from a downturn, which is why the fund is nearly flat (down 0.1% year-to-date) for 2016 on a price basis but pays out a 7.1% dividend.

Offsetting Gains with Income

By buying now, we’re getting a good price along with the downside protection of the fund’s option-writing strategy. This should offset some of the risks of buying NOBL right now.

Now for corporate bonds. We’ll target low-grade credit issues in the junk bond market, because these are particularly high yielding and the risks of defaults have been priced into the market for over a year now. Also, we’ll target a fund that is trading at a major discount to its net asset value, so we’re buying these bonds for less than their real market price. We can do this with the BlackRock Debt Strategies fund (DSU).

DSU Delivers Reliable Returns

I’ve written about this fund before, and I stand by my previous argument that this fund’s discount to NAV (currently 11.2%) and strong management team (BlackRock is the biggest private bond buyer in the world) makes this fund a no-brainer. The 6.6% dividend yield helps, too.

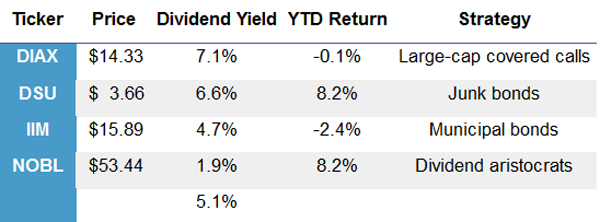

Putting it all together, this is what our portfolio looks like:

From this table above, you can see that we’ve combined assets that have uncorrelated returns. DIAX is basically flat, as it should be. IIM is down a tad after munis have corrected from a strong 2016. A resurgence in corporate bonds and stocks means those funds are up a lot for the year. We’ve exposed ourselves to high quality companies with NOBL and DIAX, more speculative and smaller firms with DSU and municipalities with IIM.

Combined we’re invested in hundreds of entities and we’re getting monthly dividends of over 5% on average. Not bad from both a risk perspective and an income perspective.

This is the power of diversification at work. But let’s not stop here. We can take this strategy and expand it to even more asset classes to create a portfolio that can withstand market downturns and pay us an income stream of 8% or more. I’ve been doing this with my No Withdrawal Portfolio, and so far I’ve seen resilient income and capital gains from this strategy.

The portfolio is full of high quality firms and funds that the market has overlooked, while focusing on those names that can and do pay a high and resilient income stream. Want to learn more? Click here and I’ll show you what the portfolio looks like.