Dividend growth stocks deserve a place in your portfolio, no matter how modest the allocation, simply because they often return 100% to 200% or better relatively quickly as their payouts rise.

You’ve probably noticed you rarely see your favorite stock paying more than 2% or 3%, even if the company raises its dividend every year. That’s because its price gets bid up as its payout rises – so you never quite get the bargain 4% yield you’re always waiting for, unless something really bad happens (like 2008).

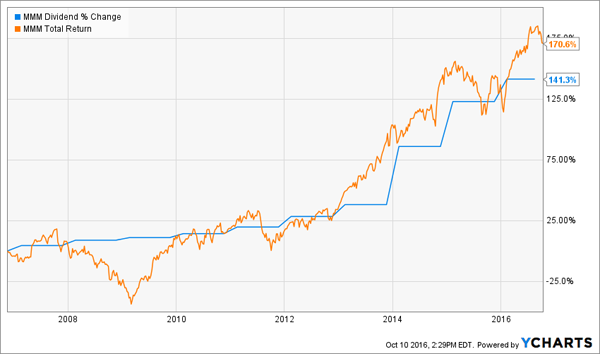

Take industrial firm 3M (MMM), which boosted its dividend by 141% over the past decade for 170% total returns:

3M’s Dividend Growth Drives 170% Returns

Yet aside from the financial crisis, you never had a chance to buy the stock at a yield above 3%. For the rest of the decade, it paid between 2% and 3%:

Steady Non-Crisis Yields

You’d have done well initiating or adding to your 3M position anytime in the last decade, thanks to the dividend growth ahead. In fact, you can use this simple formula to predict your future returns from a given stock:

Total Annual Return = Current Yield + Annual Payout Growth

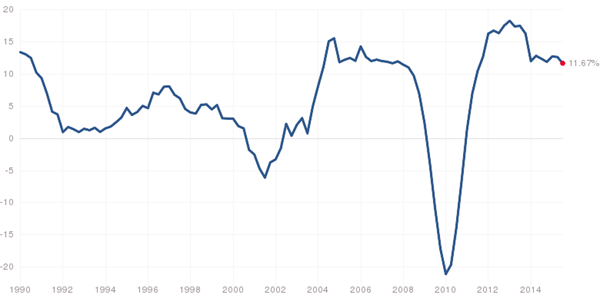

While today’s yield is easy to find, future payout growth requires some forecasting. Fortunately, we’ve had the winds at our backs for a while. Over the last 25 years, there have only been two instances – the last two recessions – when S&P 500 companies weren’t boosting their payouts year-over-year. Since 2004, the increases have mostly exceeded double-digits annually:

S&P 500 Annual Dividend Growth Rate

Unfortunately, the current pace of payout growth is slowing down faster than most investors think – which means we can’t simply buy an index and count on dividend hikes to propel our returns.

Instead, we should focus on under-owned pockets of the market. And there’s one factor that we know makes future hikes probably – excess cash.

Free Cash Flow and Virtuous Cycles

I’d encourage you to ignore widely publicized “valuation” metrics such as the price-to-earnings (P/E) ratio, because it’s too easy to manipulate earnings. Instead, focus on the amount of actual cash a business is generating.

This is represented by free cash flow (FCF), the extra money that management has at its disposal after it’s finished running and reinvesting in its business. FCF is important to you and me because it represents capital that can potentially be returned to you and me.

Price-to-FCF (P/FCF) is a better measure of value than P/E, because it actually represents the multiple you’re paying for a business’ annual excess cash. Reverse the ratio, and you have your potential annual returns if this money was placed directly in your pocket.

Buy a stock with a P/FCF of 10, and you can (in theory) expect 10% annual returns on your investment. Expand that ratio out to 20, and your expected return might fall closer to 5% annually.

This is why I’m down on current dividend aristocrats like McDonald’s (MCD), General Mills (GIS) and Kimberly Clark (KMB). All three have been bid up in the worldwide manhunt for yield, and now trade for about 22-times FCF – the high end of their historical ranges:

Dividend Aristocrats Are Pricey

Can stock buybacks make up for these high price tags? All three companies do repurchase their own shares regularly. They are poster children of the virtuous shareholder cycle we love – where buybacks reduce share counts, making future dividend hikes more impactful on a per share basis.

Problem is, only MCD has reduced its share count meaningfully (-5.9%) over the last year. GIS and KMB have slowed their buybacks (-0.4%), showing their may no longer be enough cash to go around given the high price investors are paying.

7 Under-Owned Dividend Growers

I’d ditch the expensive blue chips for underappreciated midcaps – which usually outperform their larger counterparts anyway. Here are four stocks from my watch list trading at less than 10-times free cash flow. All are growing their payouts quickly AND reducing their share counts meaningfully – a bullish sign of things to come:

SunTrust Banks (STI) trades for just 9.9-times FCF and 98.5% of book value – which means you can buy STI’s assets as a slight discount to fair value and get the banking business for free. Management bought back 2.4% of its float over the past 12 months, and recently boosted its dividend by 8.3%. With a modest 28% payout ratio, there is room for future hikes. Shares pay 2.3% today.

Travelers (TRV) has been thrown out with other insurance stocks, but this firm has sailed through a challenging low rate environment. It’s boosted FCF by 147% over the last five years while raising its payout 63%. Shares trade for 9-times FCF today and yield 2.4%, with a conservative 24% payout ratio.

Refiner Valero Energy (VLO) has never paid this much (4.4%) in its history. It trades for just 7.6-times free cash flow and management agrees that its stock is too cheap, repurchasing 5.5% of float over the last 12 months. Contrary to first-level beliefs, low oil prices have not impacted Valero’s profits negatively because its input costs have declined as well.

Finally, railcar leaser GATX (GATX) is about as cheap a stock as you’ll ever see at 3.3-times FCF. Its earnings cycle up and down with railcar demand, and investors are wary of buying at a top. But the firm’s FCF is hitting all-time highs, and management is using excess cash to repurchase shares (-4.2% last 12 months), pay a healthy yield (3.5%) and boost its payout (+15% year-over-year). If leasing demand stays steady this stock could really roll.

And I have 3 more dividend growers that I like even better than these names. All meet our criteria for big future payout growth as they:

- Trade for cheap multiples to cash flow…

- Have modest current payout ratios…

- Are buying back shares to create virtuous shareholder cycles.

Plus these 3 have great growth prospects – and I expect their top-level gains will drop right into the pockets of shareholders in the form of higher payouts. Click here for my full analysis on these 3 dividend growers with 200% upside.